Signet Jewelers is a shining example why credit agencies cannot be trusted

Back in April, we highlighted how the credit rating agencies were unfairly bearish on this massive jeweler with a powerful illusion of choice.

S&P specifically gave the company a roughly 25% chance of going bankrupt in the next five years—a number that should be reserved for the riskiest companies.

Now, in December, we’re returning to the stock to see why S&P has had to walk back their opinion.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Continuing our ‘best of 2021’ series for the Investor Essentials Daily, today we’ll be reviewing one of our best credit calls of the year.

Every Wednesday, we highlight a company with a distorted credit picture, causing dislocations between its real credit health and its grades from the rating agencies.

On April 28th, we took a look at jewelry retail giant Signet Jewelers (SIG), highlighting that its credit picture was much healthier than S&P’s ratings suggested.

S&P gave Signet a highly speculative B+ rating, implying a nearly 25% chance of bankruptcy within the next five years.

Using our Credit Cash Flow Prime analysis, we highlighted that Signet’s real credit picture was much stronger, warranting a crossover credit rating with just a 2% chance of bankruptcy.

Since then, investors, and even S&P, seem to be catching on. Signet’s prices, which ranged a few basis points above or below par in April, are now comfortably trading at a premium, most recently in the $101-$102 range. This appreciation has meant the 2024 bond yield has fallen from more than 4.5% in April to below 4%.

S&P was forced to react, and in July, it upgraded Signet slightly from B+ to BB-, meaning its implied bankruptcy risk fell to just over 10%.

While we still think Signet is safer than what the rating agencies suggest, this shows that using Uniform Accounting can help investors see signals before the market has time to react.

Even Signet’s stock was sent higher as the market grew more comfortable with its credit health. The stock has more than tripled the S&P since late April, returning 37% versus 11%.

Below, you’ll find why we were confident Signet was a stronger business than the rating agencies thought.

While the pandemic has accelerated a few long-standing trends such as the shift to e-commerce, it also reversed a slowly evolving spending pattern.

Younger generations have traditionally focused on experiences over physical things, lowering spending on traditional luxury items. Of course, over the course of 2020, consumers were left with few options for experiences.

With the risk that purchased experiences will fall through due to restrictions and rescheduling, these traditional products came back in force during the pandemic.

Another social dynamic shaken by quarantining has been the strength of close friendships and partners.

The relationships and strong friendships that have survived amidst pandemic-related challenges have emerged stronger from the crucible of sharing living conditions and each other’s company.

People are finding themselves spending more time with their partner in this remote environment than they normally would if they were going into the office every day.

Additionally, as major cities and activities have been limited during the pandemic, familial ties have deepened as couples spend more time at home with their loved ones.

Both of these trends mean that jewelry retailers like Jared’s, Kays, and Zales are likely to see strong tailwinds that could bump up demand compared to as the world exits the pandemic.

Furthermore, jewelry is a luxury item people like to see in person before purchasing, thanks to the large price tag and individual appeal. This is why the jewelry business may not be as disrupted by online threats as other industries.

These potential tailwinds for demand can boost jewelers to post better cash flow metrics than what credit rating agencies are expecting.

Signet Jewelers (SIG) controls all three of the aforementioned jewelry brands, and it is positioned well for these demand trends.

However, rating agencies are still skittish when rating the company’s debt. Specifically, S&P gives Signet Jewelers a highly speculative B+ rating, with the implied assumption of a 25%+ risk of default over the next five years.

For context, this implies a 1-in-4 chance the company goes bankrupt over the next 5 years.

Even if equity investors do not want to take the risk of betting on a recovery in Signet Jewelers, the company is much safer than S&P suggests.

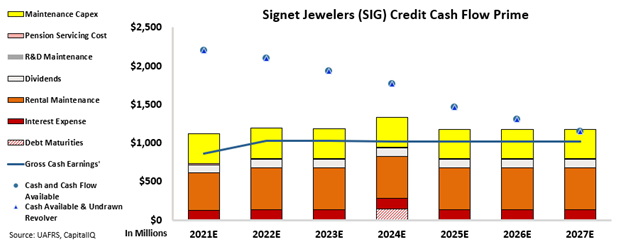

Our Credit Cash Flow Prime (CCFP) analysis is able to get to the heart of the firm’s true credit risk.

In the below chart, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

As depicted, Signet Jewelers has massive cash liquidity and therefore should have no issues handling its obligations going forward. Its cash on hand and cash flows should be sufficient to weather any storm over the next five years.

Even when the company does have debt maturities, its cash balance suggests it can navigate any potential challenges ahead.

Rather than a highly speculative name, Signet Jewelers is actually in a strong position. This is why S&P’s B+ high yield rating, with a 25%+ risk of default expectation, does not make sense.

Using the CCFP analysis, Valens rates Signet Jewelers as an investment grade XO (BBB-) rating. This rating corresponds with a default rate below 2% within the next five years, a more realistic projection once a holistic understanding of the company’s risk is taken into account.

Ultimately, Uniform Accounting and the Credit Cash Flow Prime analysis highlights how Signet Jewelers’s credit risk profile is much safer than what rating agencies believe.

SUMMARY and Signet Jewelers Limited Tearsheet

As the Uniform Accounting tearsheet for Signet Jewelers Limited (SIG:USA) highlights, the Uniform P/E trades at 79.8x, which is above the global corporate average of 24.0x and its historical average valuations of 31.3x.

High P/Es require high EPS growth to sustain them. In the case of Signet, the company has recently shown a 15% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Signet’s Wall Street analyst-driven forecast is a 75% EPS decline in 2022 and 4% EPS growth in 2023.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Signet’s $81 stock price. These are often referred to as market embedded expectations.

Signet is being valued as if Uniform earnings were to grow 2% per year over the next three years. What Wall Street analysts expect for Signet’s earnings growth is below what the current stock market valuation requires in 2022, but above that requirement in 2023.

Furthermore, the company’s earning power is in line with the corporate averages and cash flows and cash on hand are twice its total obligations—including debt maturities, capex maintenance, and dividend. Also, intrinsic credit risk is 50bps above the risk free rate. Together, this signals a low credit and dividend risk.

To conclude, Signet’s Uniform earnings growth is in line with its peer averages. However, the company is trading above average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research