America’s favorite sandwich is ready for more

The peanut butter & jelly sandwich has been a staple of American cuisine for over one hundred years. It is so ingrained as a quick snack anyone can make, it’s easy to forget. However, smart investors should be thinking about the implications of the quarantine for PB&J demand.

Using GAAP accounting, it appears today’s company struggles to stay profitable. Uniform Accounting tells a different story.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

In the past hundred years, it has become substantially easier for anyone to cook. Thanks to cookbooks, a proliferation of quality ingredients, and advances in kitchen technology, the boundaries between professional chef and amateur have broken down.

The easiest meal to make doesn’t rely on any of these three things. It is a simple combination of three ingredients.

Contrary to popular belief, George Washington Carver did not invent peanut butter. In 1895, Dr. John Harvey Kellogg of Kellogg’s cereal fame patented modern peanut butter.

In 1896, a Good Housekeeping article encouraged those at home to combine peanut butter and bread and other ingredients like piment, cheese, celery, and more.

It wasn’t until 1901 when a Boston cooking magazine called for combining the peanut paste and currant or jelly. The rest is history.

Since then, companies like Smucker’s (SJM) have made their business supplying the peanut butter and jelly for countless PB&J sandwiches.

We have often talked about how the At-Home Revolution has benefitted takeout and grocery delivery companies. With fewer people able to eat out for dinner, the losers have been traditional sit-down restaurants relying on customers to come in for a meal.

Throughout the pandemic, parents and children alike have been forced to eat more meals at home, and nothing is as easy to make as peanut butter and jelly.

Not only this, but more pets are being brought into homes as well. Smucker’s also benefits the company’s own famous pet food brands such as Meow Mix and Kibbles ‘n’ Bits.

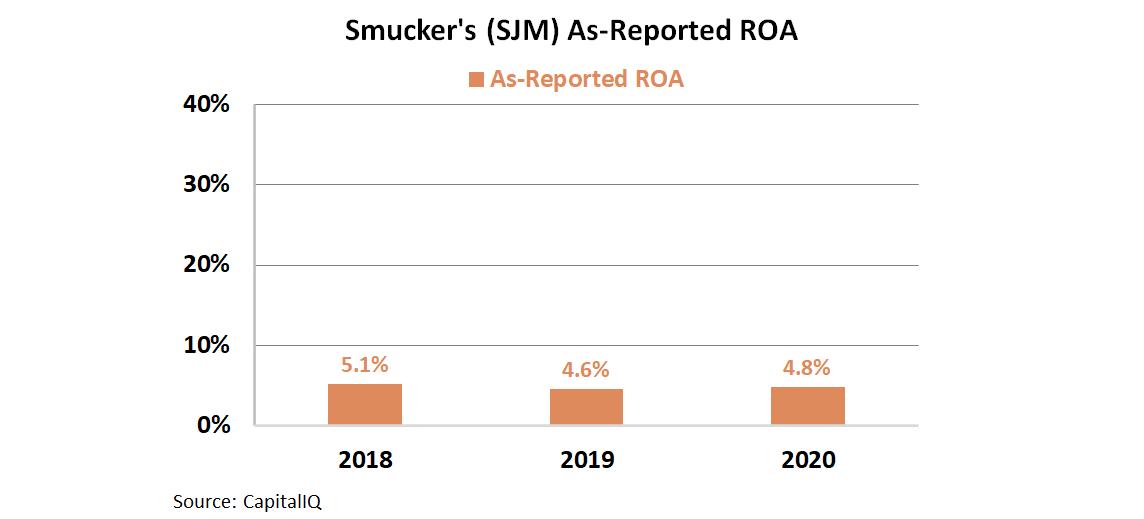

Smucker’s has been benefiting from both of these trends over the past year. However, if an investor were to look at the as-reported metrics they would never know it.

Over the past three years, it appears Smucker’s has seen profitability stagnate at around 5%, just around the company’s cost-of-capital. It would seem selling such a commoditized product does nothing for returns.

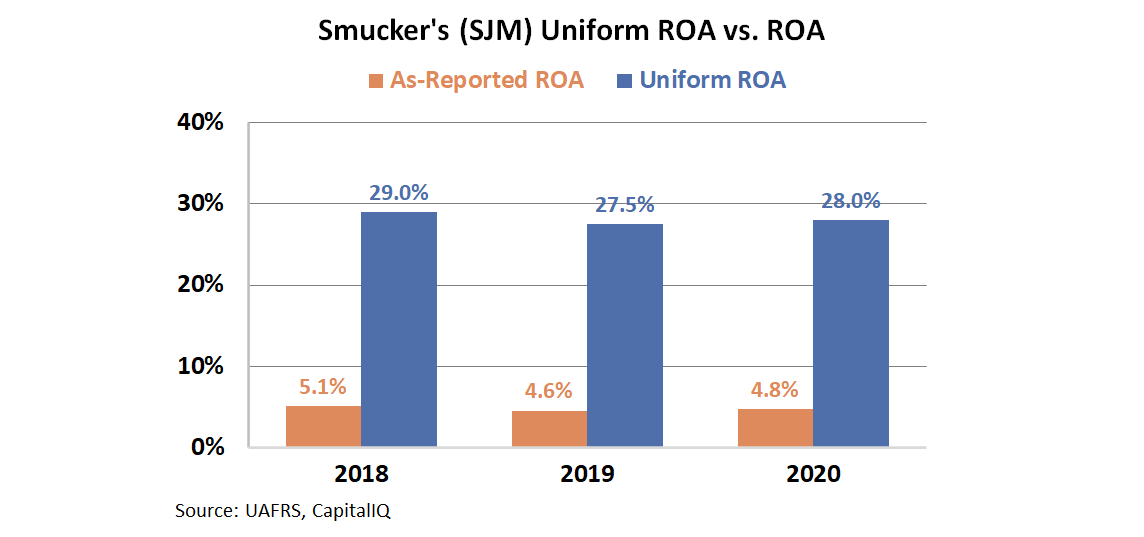

In reality, these metrics fail to reflect the real earnings power of Smucker’s. Distortions in GAAP accounting around goodwill, amortization, and other line items have suppressed the firm’s profitability.

When looking through a Uniform Accounting lens, we can see the true earnings power of the firm.

Rather than returns at the cost-of-capital, Smucker’s makes real economic profit, with returns above 27% over the past three years.

Investors without Uniform Accounting would be writing off Smucker’s as a simple food producer without any pricing power.

In reality, Smucker’s is able to leverage its brand name and efficient cost structure to the benefit of investors. However, those stuck using GAAP metrics would never be aware of the firm’s real profitability.

SUMMARY and The J. M. Smucker Company Tearsheet

As the Uniform Accounting tearsheet for The J. M. Smucker Company (SJM:USA) highlights, the Uniform P/E trades at 15.8x, which is below the global corporate average of 25.2x but around its own historical average of 16.4x.

Low P/Es require low EPS growth to sustain them. In the case of Smucker’s, the company has recently shown a 16% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Smucker’s Wall Street analyst-driven forecast is a 10% EPS growth in 2021 followed by an immaterial EPS shrinkage in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Smucker’s $126 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 3% per year over the next three years. What Wall Street analysts expect for Smucker’s earnings growth is above what the current stock market valuation requires in 2021 and 2022.

Furthermore, the company’s earning power is 5x the long-run corporate average. Also, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a high dividend and credit risk.

To conclude, Smucker’s Uniform earnings growth is in line with its peer averages, but the company is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research