The stock price implies that this company sells pickaxes (instead of mining for gold): TRUE margins (half of as-reported) say they’re losing anyway.

The market’s stock price implies that this company can keep selling pickaxes instead of mining for gold. TRUE uniform UAFRS-based margin analysis shows that the firm is still losing anyway. Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company

Investor Essentials Daily:

Tuesday Tearsheet & Embedded Expectations

Powered by Valens Research

When talking about businesses we love, there is one trope that often comes up, thanks to Levi Strauss.

“Be the guy who sells pickaxes, not the guy who is trying to mine the gold.”

In 1853, Strauss moved to San Francisco, arriving in the middle of the California gold rush. Instead of rushing to the hills to try to find gold, he opened up a dry goods store, supplying the gold miners.

Gold mining is a tough business. Not only did you have to worry about the low probability that you’d ever find a meaningful amount of gold, you also had to worry about surviving finding gold, or someone else pushing you out. The hills of California were a lawless place.

But supplying gold miners in the middle of a gold rush is a phenomenal business. No matter who is successful, everyone needs the suppliers to prospect. That was the business Strauss was in, and business was phenomenal.

Think of it… can you make even one gold miner in existence since the gold rush? Meanwhile, who doesn’t know Levi’s still today.

Some of our favorite companies and stocks have historically followed the same business model in their respective industries. Many over the years have been “sellers of pick axes” to various industries. A handful of the names that are currently on our Conviction Long Idea List fit that criteria.

Finding a pickaxe seller, doesn’t guarantee you a winning investment though. To find a good pickaxe seller, you need to find a company that isn’t just selling pickaxes, it needs to be selling pickaxes to a growing industry.

Because when you find a supplier that is supplying a shrinking industry, the same truism works, only in reverse. In a declining industry, you can find winners and losers, as you have lower cost competitors or higher quality competitors that can keep their demand.

A supplier to a shrinking industry will lose no matter what though, because the overall pie of demand will fall. The company may see demand shrink less because of how good they are, but it will still shrink.

That’s the situation Schlumberger (SLB) has found themselves in the past 5 years.

Schlumberger is viewed as a world class oil & gas services company and supplier to the industry. But in the face of the oil crisis from 2015 on, the stock has fallen from a peak of almost $120 in mid 2014 to $41 now.

With a 66% decline, it would be reasonable to assume the market has correctly priced in Schlumberger’s struggles as a pickaxe provider to a declining industry.

But, when we use Uniform Accounting analytics to understand the company’s real performance, and what the market is pricing in, we see that’s not the case.

The market is currently pricing Schlumberger for a sustained recovery in their business… yet they might struggle to deliver on this without a real inflection in the industry.

And management is showing more concern about their outlook, pointing to reasons to think the market might be disappointed.

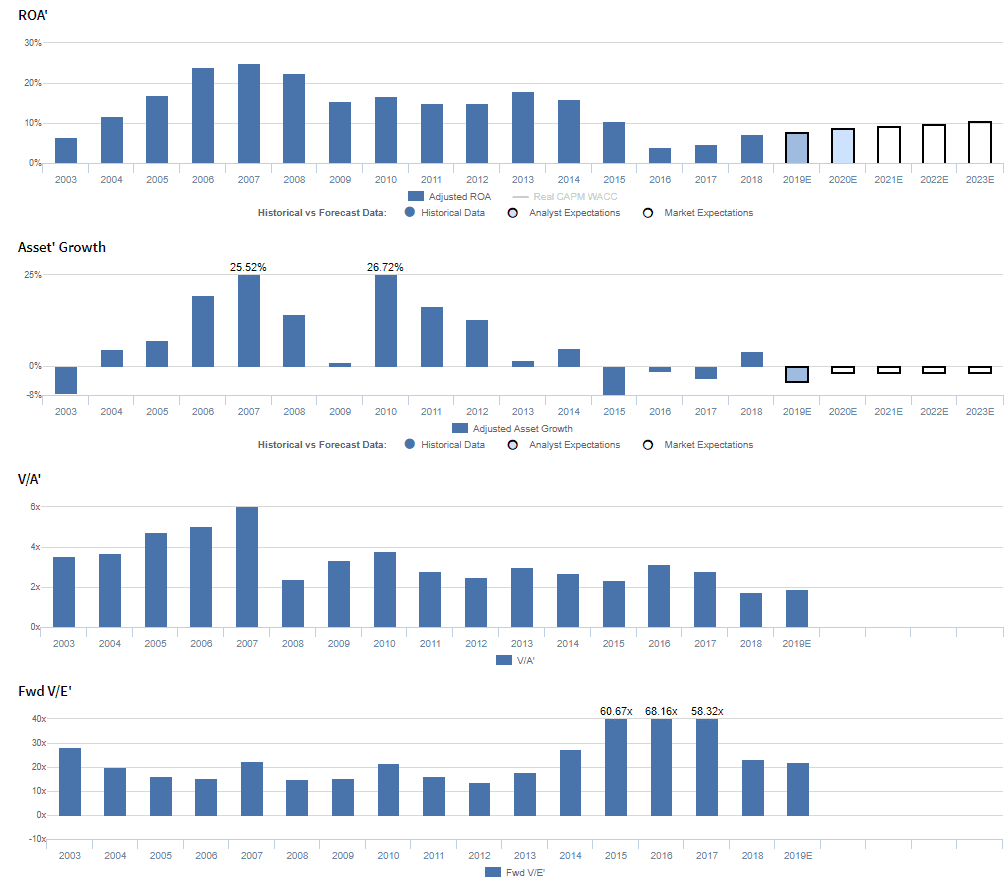

Schulmberger Embedded Expectations Analysis – Market expectations are for a recovery in Uniform ROA, but management appears concerned about OneStim, margins, and their international operations

SLB currently trades slightly above corporate averages relative to UAFRS-based (Uniform) Earnings, with a 21.0x Uniform P/E. At these levels, the market is pricing in expectations for Uniform ROA to expand from 7% in 2018 to 10% in 2023, accompanied by 2% Uniform Asset shrinkage going forward.

Analysts have similar expectations, projecting Uniform ROA to improve to 9% in 2020, accompanied by 4% Uniform Asset shrinkage.

Historically, SLB has seen cyclical, but generally declining profitability. Uniform ROA improved from 7% in 2003 to a peak of 25% in 2007, before falling to 15%-17% levels from 2009-2012. Thereafter, Uniform ROA expanded to 18% in 2013, before falling to a low of 4% in 2016 in the wake of the global oil glut, and rebounding slightly to 7% in 2018. Meanwhile, Uniform Asset growth has been volatile, positive in 12 of the past 16 years, while ranging from -8% to 27% with most of their Uniform Asset shrinkage coming since 2015 due to the aforementioned oil glut.

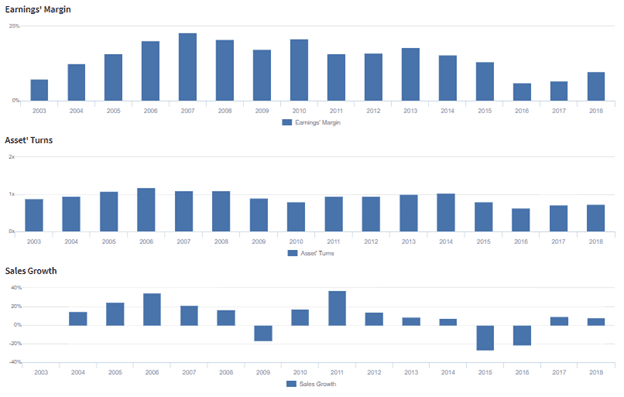

Performance Drivers – Sales, Margins, and Turns

Cyclicality in Uniform ROA has been driven primarily by trends in Uniform Earnings Margins, and to a lesser extent, Uniform Asset Turns. After improving from 7% in 2003 to a peak of 23% in 2007, Uniform Margins compressed to 17% in 2009, before rebounding to 21% in 2010. Thereafter, Uniform Margins faded to 6% in 2016, before recovering to 10% in 2018. Meanwhile, after improving from 0.9x in 2003 to 1.2x in 2006, Uniform Turns compressed to 0.8x in 2010, before rebounding to 1.0x in 2014, and fading to 0.6x-0.7x levels from 2016-2018. At current valuations, markets are pricing in expectations for Uniform Margins and Uniform Turns to return to levels not seen since before the collapse in oil prices.

Earnings Call Forensics

Valens’ qualitative analysis of the firm’s Q3 2019 earnings call highlights that management may be concerned about the sustainability of recent performance improvements, ongoing headwinds to growth on land, and OneStim activity. Furthermore, they appear concerned about the sustainability of recent international revenue growth and margin expansion, and they may lack confidence in their ability to meet their full year international revenue growth target. Additionally, they appear concerned about the impact of their ongoing divestitures and about the impact of their decision to pursue margin over scale for OneStim. Finally, management appears concerned about their ability to meet their book-to-bill ratio target for OneSubsea, and they may lack confidence in their ability to meet their North American margin improvement target.

UAFRS VS As-Reported

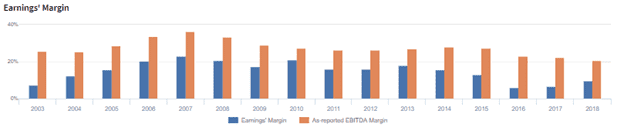

Uniform Accounting metrics also highlight a significantly different fundamental picture for SLB than as-reported metrics reflect. As-reported metrics can lead investors to view a company to be dramatically stronger or weaker than real operating fundamentals highlight. Understanding where these distortions occur can help explain why market expectations for the company may be divergent.

As-reported metrics significantly overstate SLB’s margins, one of the primary drivers of profitability. For example, as-reported EBITDA margin for SLB was 21% in 2018, materially higher than Uniform Earnings Margin of 10% in the same year, making SLB appear to be a much stronger business than real economic metrics highlight. Moreover, since the global oil glut, as-reported EBITDA margin has consistently been at least 2x higher than Uniform Earnings Margin, distorting the market’s perception of the firm’s recent performance.

Schlumberger Tearsheet

As our Uniform Accounting tearsheet for Schlumberger highlights, Schlumberger trades slightly above market average valuations. The company has recently had 75% Uniform EPS growth. EPS growth is forecast to remain positive, at 7% in 2019, and 16% in 2020. At current valuations, the market is pricing the company to see earnings grow by 5% a year going forward.

The company’s earnings growth is forecast to be slightly above peers in 2019, but the company is trading only in line with peer average valuations. The company has low returns relative to current corporate averages, but no cash flow risk to their strong dividend.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research