Rising oil prices don’t give this company a clean bill of health

As oil prices begin to rocket back, there is an opportunity for this company to recover, after years of little demand.

That said, investors have to first look at the credit picture when analyzing this investment decision, given rating agencies are not always accurate when evaluating debt.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

With the surging recovery in oil prices, investors are beginning to get excited about capital expenditures returning to the industry.

As oil prices are drastically rising and the recovery remains strong, there is one part of the market that will be a major winner.

After months became years of stagnant demand for oil and relatively low prices, the service providers have taken on huge debt loads to stay alive. The oil crash in the middle of the decade, coupled with the collapse in the midst of the pandemic back in March of 2020, has led many to the brink of bankruptcy.

However, with the recovery in place, this has all changed. These players have significant opportunities ahead. And they must be capitalized on to make up for years of drought.

Service providers like Schlumberger (SLB) may experience material secular tailwinds and positive consumer trends.

Ratings agencies can now relax a bit more with the recovery in place, particularly for service providers, since these companies were always rated as investment grades. With reinforced demand, the odds of bankruptcy are becoming theoretically slimmer.

Specifically, Moody’s, one of the major rating agencies, rates Schlumberger’s unsecured debt as an investment grade A2 rating, with the implied assumption of an under 1%+ risk of default over the next five years.

However, after so many years of being forced to take on debt with low cash flows, this may only be wishful thinking on the part of the rating agencies.

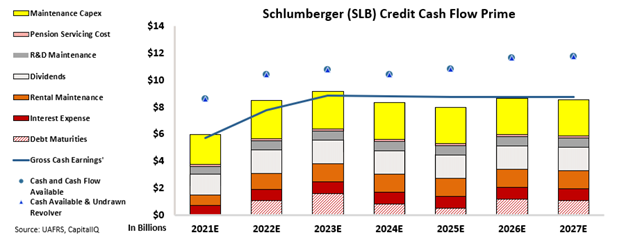

Our Credit Cash Flow Prime (CCFP) analysis is able to get to the heart of the firm’s true credit risk.

In the below chart, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

As depicted, Schlumberger’s cash flows fail to cover operating obligations over the next few years. This makes it difficult to comfortably give the company an investment grade rating, with a 1% chance of going bankrupt over the next five years.

Rather than a name with barely any risk, Schlumberger is actually in a position that investors should not overlook. This is why Moody’s A2 high yield rating, with an under 1%+ risk of default expectation does not make sense.

Using the CCFP analysis, Valens rates Schlumberger as a high yield HY2+ rating. This rating corresponds with a default rate around 25% within the next five years, a more realistic projection once a holistic understanding of the company’s risk is taken into account.

SUMMARY and Schlumberger Limited Tearsheet

As the Uniform Accounting tearsheet for Schlumberger Limited (SLB:USA) highlights, the Uniform P/E trades at 28.3x, which is above the global corporate average of 23.7x, but below its historical Uniform P/E of 31.2x.

High P/Es require high EPS growth to sustain them. In the case of Schlumberger, the company has recently shown a 63% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Schlumberger Wall Street analyst-driven forecast is a 6% EPS decline and a 41% EPS growth in 2021 and 2022, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Schlumberger’s $36 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 5% annually over the next three years. What Wall Street analysts expect for Schlumberger’s earnings growth is below what the current stock market valuation requires in 2021, but is above that requirement in 2022.

Furthermore, the company’s earning power is in line with the corporate average. Also, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a high dividend risk.

To conclude, Schlumberger’s Uniform earnings growth is in line with its peer averages, but the company is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research