By sticking to the basics, this technology distribution firm made the most of the pandemic

Often, the flashiest industries and companies hog the investing news cycle, excluding companies in more mundane industries. Investors believe this company to be boring, propelling them to undervalue the business.

The firm’s path to focus on core IT services is valued highly by consumers, but investors would completely miss this trend by ignoring the Uniform Accounting metrics of Synnex.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

Some investors believe this company to be operating in a boring industry, and pass it right by.

The company operates in the technology distribution industry, helping businesses sort through and purchase large amounts of electronics. While this seems like a sleepy industry, there is more than meets the eye.

This firm acts more as a value-add reseller, where it takes in various hardware and software products and offers value by integrating them into different pieces of a bigger solution for customers.

They are especially important for customers who would not normally be able to complete this integration process on their own, let alone the help of an enterprise.

This is why this firm’s services are highly valued.

One of the largest technology distributors today is Synnex (SNX). On a higher level, Synnex works in the distribution, logistics, and integration services for the technology space.

Specifically, the distributor helps with data center and cloud installation, among other technology solutions for businesses.

Additionally, after merging with Convergys, the company decided to spin off Concentrix and list it separately on the U.S. stock exchange.

This should allow the technology distributor to focus on its core IT services and distribution business.

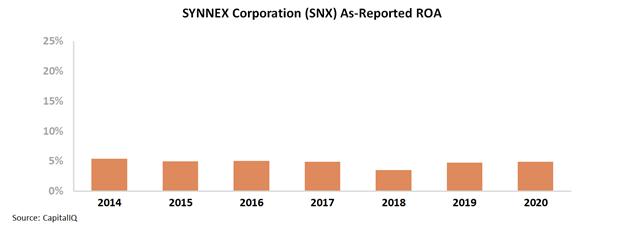

However, using as-reported metrics, it would appear Synnex has been unable to profit from this model.

As shown in the below chart, the firm’s as-reported return on asset (ROA) levels have been around 5% levels since 2014.

These levels would lead investors to believe the firm is posting weak profitability levels, well below the U.S. corporate average of 12%.

In reality, this is not an accurate picture of Synnex’s performance. Over the past few years, the firm has been able to grow its ROA well above corporate averages.

When looking through a Uniform Accounting lens, it becomes clear that the firm’s business model is better than it seems. Investors should not be sleeping on this anymore.

Specifically, the company’s ROA levels are much higher than GAAP portrays and have expanded from 12% in 2014 to 17% in 2020.

As you can see, Synnex’s Uniform ROA levels are trending better than as-reported metrics over the same timeframe, which portrays how easily as-reported metrics can misrepresent reality.

In reality, the firm’s path to focus on core IT services is valued highly by consumers, but investors would completely miss this trend by ignoring the true, Uniform Accounting metrics of Synnex.

SUMMARY and SYNNEX Corporation Tearsheet

As the Uniform Accounting tearsheet for SYNNEX Corporation (SNX:USA) highlights, the Uniform P/E trades at 14.2x, which is below the global corporate average of 25.2x, but around its own historical average of 13.3x.

Low P/Es require low EPS growth to sustain them. That said, in the case of Synnex, the company has recently shown a 9% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Synnex’s Wall Street analyst-driven forecast is a 30% EPS shrinkage in 2021, followed by a 4% EPS growth in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Synnex’s $90 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 9% per year over the next three years. What Wall Street analysts expect for Synnex’s earnings growth is below what the current stock market valuation requires in 2021, but above its requirement in 2022.

Furthermore, the company’s earning power is 3x the long-run corporate average. Also, intrinsic credit risk is 200bps above the risk-free rate and cash flows and cash on hand are almost twice its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a low dividend and credit risk.

To conclude, Synnex’s Uniform earnings growth is below its peer averages, and the company is also trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research