Some economists’ concern for the economy extends past the release of a vaccine

Some economists are concerned about the possibility of inflation after the lifting of stay-at-home orders.

As buyers return to old levels of spending and firms see constrained supply, more money could chase fewer goods, leading to inflation.

However, this view of inflation is not rooted in fact. By looking at historical levels of inflation, we can understand how much of a risk the economy has of an inflationary spiral.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

In April, the United States Congress signed off on a coronavirus relief package at over three trillion dollars. It has become apparent the U.S. will continue to spend large amounts of money to keep businesses and individuals afloat during this time of forced economic contraction.

This aggressive fiscal stimulus has investors concerned for 2021 and 2022. For economist Charles Goodhart, the real crisis will come after a vaccine or treatment arrives for the coronavirus.

After the crisis is in the rear view mirror, buyers could rush out to stores, restaurants, and concerts, to spend all the money they didn’t in 2020. However, this increased demand could be matched with a lack of supply, as factories, farms, and service centers would have been understaffed during the pandemic.

This rise in demand and shock to supply would drive up prices, causing large amounts of destabilizing inflation.

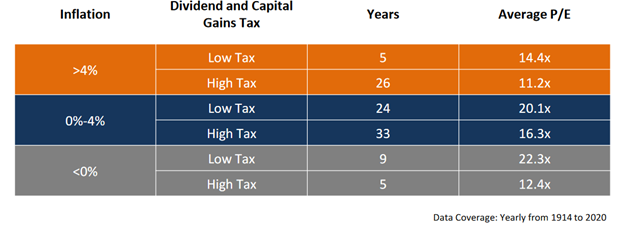

Not only would this inflation cause an impact to the wider economy, it would directly affect the valuation of the stock market. As we talked about in April, the tax environment and inflation will directly impact the average price to earnings, or P/E ratio, of the stock market.

As you can see, inflation between 0% and 4% calls for valuations of 20.1x in the current low tax environment. Environments with inflation over 4% calls for P/E ratios of 14.4x on average. Were inflation rates to rise too high, stocks could drop by 34% as P/E falls from current 21.9x P/E (on 2021 earnings) due to inflation pressures.

And that is before we even get into what could happen if there is a “blue sweep” of the Presidency, House, and Senate and taxes are raised to pay for current and future programs. In a high tax high inflation environment, P/Es drop to 11.2x.

For context, that would mean a 50% drop in valuations, before even calculating how lower earnings, due to higher taxes, would also mean the P/E was on a lower earnings number.

This is why economists and policymakers are concerned about the risk of a serious inflation driven contraction. However, this scenario is not backed up by the data, for two key reasons.

The first of these can be found in the measure of historic inflation over time. The chart below shows the percentage change in the consumer price index, or CPI year over year. The CPI is a basket of goods which US households tend to buy every year, such as groceries, apparel, and housing. It is meant as a proxy to track consumer inflation.

As you can see from the chart below, since 1991 the United States has been able to keep down periods of high inflation. During the summer of 1996, the Fed privately began targeting an inflation rate of 2% to best facilitate economic growth.

Over the past 24 years, inflation has been low and consistent. The Fed has been successful in moderating inflation. In response to the phenomenon of stagflation in the 1970s, Milton Fiedman developed an inflation theory centered around monetary policy. As the regulation of monetary policy is completely under control of the Federal Reserve, it has taken on the mantle of reining in inflation.

To highlight how inflation has been properly controlled in the past 30 years, we can look at the 2008 economic crisis. After large stimulus packages, the economy saw no material impact to inflation, despite the quantitative easing that was enacted. This indicates large stimulus packages can have little impact on inflation, if correct monetary policy is applied.

The second reason the US is not primed for an inflation crisis is because of the capacity utilization, which we talked about last week. Capacity utilization is currently sitting at 30-year lows.

While this is traditionally a red flag for any economist, in this situation, it means as a vaccine or treatment is rolled out in 2021, there will not be a huge supply shock on the economy. As the percentage of capacity utilization rises, supply will catch up with demand and prices will stay level.

In aggregate, inflation risk for the U.S. economy is low, due to a history of successful monetary policy and cratering asset utilization. Inflation is not likely to lead to a massive dip in the US stock market. A post-election tax hike could be a very different story…

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research