Investors are too quick to write off this established media company

As technology continues to change, it’s easy to drop the last generation and focus on the next trend. However, technology doesn’t disappear overnight. Adoption is often a messy process, and investors can often ditch a successful firm too early.

Using GAAP accounting, today’s company appears to be struggling to stay relevant. However, its real Uniform returns tell a different story.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

Investors are always looking to invest in the next big idea. Every investor hopes to buy the next Apple (AAPL) or Amazon (AMZN) at the ground floor. One phrase for this phenomenon is “Fear of Missing Out,” or FOMO

The newest example of FOMO can be seen around developments like 5G. Channels like CNBC love to report on new exciting 5G stocks to invest in right now, before 5G fully takes over for 4G.

Another disruptor is the rise of streaming. With the rise of Netflix (NFLX), investors are already moving to on-demand content in the hundred of millions. Conversely, this means investors are no longer excited about traditional TV business models like cable.

Pundits are decrying the death of traditional TV, with cable companies being forced to unbundle channels to service demand. Traditionally, cable companies were able to charge large premiums by packaging news, sports, and entertainment all in one purchase.

Now, news can be read or watched on platforms like Twitter (TWTR) or Youtube. Services like NFL Redzone or ESPN+ allow users to pay only for the sport they watch. Netflix, Hulu, and Disney+ are streaming shows directly to users’ smart devices.

This means investors are weary of a name without any of these advantages like Fox (FOXA).

In 2018, Fox sold off many of its assets to Disney (DIS) including its prized 21st Century Fox assets and its 30% stake in Hulu. Rather than investing into the future, it seemed like Fox was doubling down around its core legacy assets like the Fox news channel.

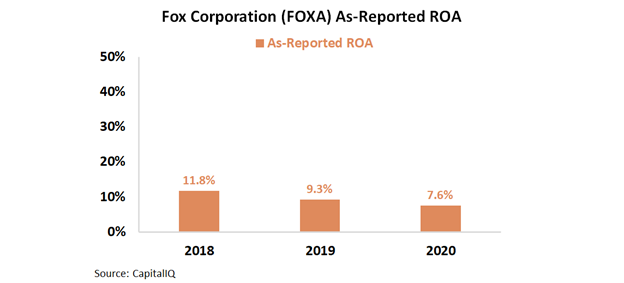

The as-reported numbers help tell the same story. It appears Fox is struggling to stay relevant with this dogged adherence to its old competitive advantage. Since 2018, GAAP returns have fallen below corporate averages of 12%, down to just 8% in 2020.

Using as-reported metrics, it’s no wonder investors look at Fox and view it as a company stuck in the past.

In actuality, this view has more to do with GAAP distortions than it does with reality. As-reported accounting around items like goodwill, interest expense, and other line items is artificially smothering the company’s profitability.

When looking through a Uniform Accounting lens, it becomes clear that the firm’s business model is better than it seems.

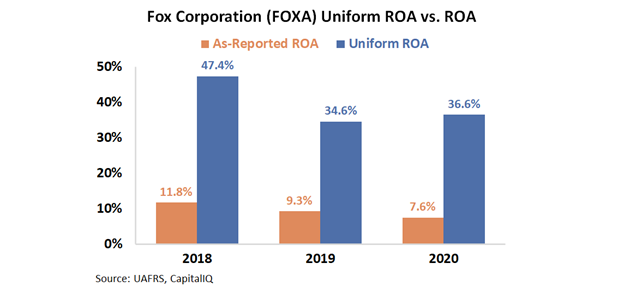

Using UAFRS, we can see Fox’s profitability has declined since 2018. However, it has fallen from far loftier heights of 47%. Returns are still at 37% levels in 2020, more than three times corporate averages.

Investors are often too quick to write off companies like Fox due to distortions in GAAP accounting. While different internet services are disrupting Fox’s traditional business model, cable news is still a profitable business.

While investors are ready to jump ship at the first sign of the next big thing, they are missing out on an established business still printing money for investors. It is easy to let the newest, flashiest trend distract from solid, safe investments.

Without Uniform Accounting, investors would write off still profitable names like Fox and chase potentially other investments in the name of FOMO.

SUMMARY and Fox Corporation Tearsheet

As the Uniform Accounting tearsheet for Fox Corporation (FOXA:USA) highlights, the Uniform P/E trades at 9.1x, which is below the global corporate average of 25.2x, but above its own historical average of 7.0x.

Low P/Es require low EPS growth to sustain them. In the case of Fox Corporation, the company has recently shown an 8% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Fox Corporation’s Wall Street analyst-driven forecast is an 18% EPS growth in 2021 and an 18% EPS decline in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Fox Corporation’s $33 stock price. These are often referred to as market embedded expectations.

The company can have Uniform earnings shrink by 15% per year over the next three years and still justify current stock prices. What Wall Street analysts expect for Fox Corporation’s earnings growth is above what the current stock market valuation requires in 2021, but below that requirement in 2022.

Furthermore, the company’s earning power is 6x the long-run corporate average. Also, cash flows and cash on hand are over 5x its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low dividend and credit risk.

To conclude, Fox Corporation’s Uniform earnings growth is in line with its peer averages but the company is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research