Spending cuts and regulatory shifts are squeezing this insurer

Health insurance has long been seen as one of the market’s most dependable businesses for decades.

This is due to the fact that insurers could set their own prices for monthly premiums. And since these firms represent so many customers, they possess tremendous leverage over hospitals and drugmakers.

However, this seems to be shifting. The Trump administration has stripped Biden-era subsidies through the Big Beautiful Bill which cut roughly $1 trillion from Medicaid.

And most recently, the administration just proposed a 0.9% increase for Medicare insurers in 2027—far below the 4% to 6% increase expected by Wall Street and down from the 5% increase health insurers got this year.

UnitedHealth (UNH), one of America’s biggest insurers saw its stock drop by 9% during after-trading hours. Moreover, investors are expecting a steep decline in its returns in the coming years.

Investor Essentials Daily:

Wednesday News-based Update

Powered by Valens Research

Health insurance has long been considered as one of the market’s most dependable businesses.

It’s because for decades, these companies could set their own prices for monthly premiums. Since these firms represent so many customers, they gained tremendous leverage over hospitals and drugmakers.

That structure helped create giants like UnitedHealth (UNH), Elevance Health (ELV), and Cigna (CI). These firms weren’t the flashies but they were reliable. UnitedHealth was up more than 100,000% since the 1980s at the start of this year.

Elevance and Cigna have both risen by several thousand percent in a similar time frame.

Profitability held up even through economic downturns. During the pandemic, returns improved as government subsidies sought to keep enrollments stable.

However, this once-dependable backdrop is shifting. President Donald Trump is pushing drugmakers to cut prices. And insurers, once largely ignored, are now under scrutiny. President Trump is framing them as part of the cost problem rather than a neutral intermediary.

As a result, the market is growing uneasy with health insurers after gaining ground in recent years.

Health insurers were boosted in recent years partly due to Washington.

Pandemic-era legislation expanded Affordable Care Act subsidies, pulling millions of new members into exchange plans.

One subsidy opened signups to folks of all income levels, not just lower-income groups. Another limited payments as a percentage of household income.

But those subsidies became a major political debate during the recent government shutdown. While they help provide health care coverage to more Americans, they’re also expensive.

Congress chose not to extend them. They’ve since expired.

As subsidies end, enrollment is shrinking. And it’s skewing older—meaning higher medical costs per member and less profitability, on average.

Medicaid is moving in the same direction. The Big Beautiful Bill, signed back in July, is expected to cut roughly $1 trillion from the program.

These changes are scaring investors away from health insurance. Unfortunately, UnitedHealth and its peers are about to get squeezed further.

The Trump administration is proposing nearly flat reimbursement rates for Medicare insurers in 2027. Wall Street analysts were expecting a 4% to 6% increase. However, the administration proposed a rate of 0.09%, corresponding to roughly $700 million.

Not only does this fall short of Wall Street expectations, it is also down from the 5.06% increase health insurers got this year.

According to Chris Klomp, the director of Medicare and Deputy Administrator of the Centers for Medicare & Medicaid Services, the proposed measure seeks to ensure Medicare insurers have stable reimbursement and improve payment accuracy.

In response to the proposal, an insurance industry group noted that the proposed measure “could result in benefit cuts and higher costs for 35 million seniors and people with disabilities.”

Shares of UnitedHealth—which is also the biggest Medicare insurer based on membership—dropped by more than 15% following the news.

With insurers like UnitedHealth in the crosshairs of regulators, investors are worried that this firm’s best years may finally be behind it.

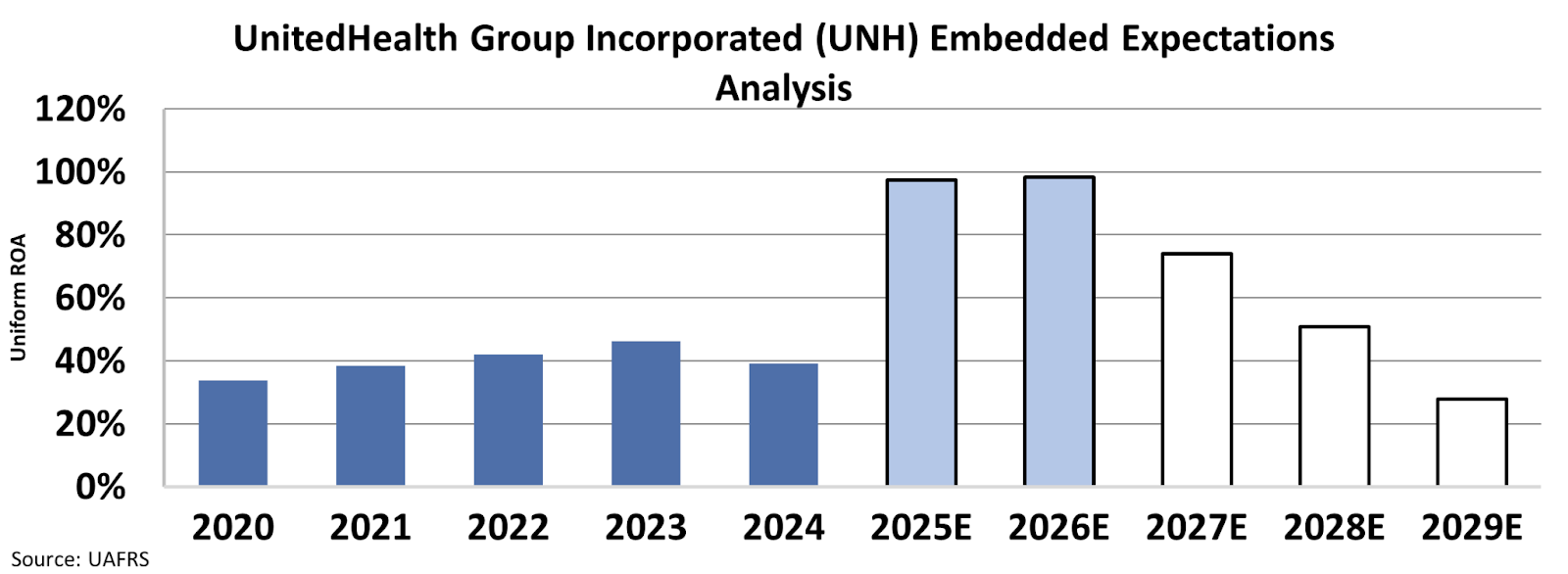

We can see this through Valens’ Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

UnitedHealth has generated a Uniform return on assets (“ROA”) that’s well above 30% from 2020 to 2024. Wall Street analysts are expecting returns to peak at 98% by 2026.

However, the long-term expectations of investors are bleak. By 2029, they expect UnitedHealth’s Uniform ROA to decline steeply to 28%.

With regulators putting UnitedHealth and its peers under more scrutiny, investors are worried that these companies can no longer deliver consistently high returns.

Even though the health insurance business model hasn’t changed, the industry’s relationship with the government definitely has. Their business models rely heavily on government policy, making political and regulatory shifts all the more impactful.

With policy momentum shifting against insurers, investors should adopt a cautionary stance towards UnitedHealth and the industry as a whole.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research