Not even the power of online streaming services can take this company down

Despite facing many secular headwinds as a legacy TV broadcasting company, with new technology such as online streaming services, this company has remained resilient.

Rating agencies are lumping this name in with many other struggling companies in the space, which is overly pessimistic considering the company’s real credit health.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

In the nascent days of television, ABC, NBC, and CBS dominated the airwaves. Known as the “Big Three, ” this oligopoly had total control of all advertising spending on TV.

Now, there is more of a fragmented TV viewing audience with multiple channel options across various networks. With the exorbitant cost of running a TV network reduced, competition could enter the space.

Even more disruptively, online streaming has further displaced these legacy TV broadcasters significantly.

Local broadcast affiliates have been particularly hard hit by these trends. These companies have been steadily bleeding viewers for years, if not decades.

Consequently, both equity and credit investors have had extremely bearish outlooks on local news conglomerates for quite some time now.

However, these bearish perspectives might be unwarranted.

The concerns regarding these companies seeing collapsing revenues is so strong that one of the largest players in the space is getting crushed by credit rating agencies.

The E.W. Scripps Company (SSP), founded in 1878, engages in television and newspaper publishing. As mentioned, it is one of the largest companies in the space.

That said, S&P gives E.W. Scripps a highly speculative B rating, with the implied assumption of a 25%+ risk of default over the next five years.

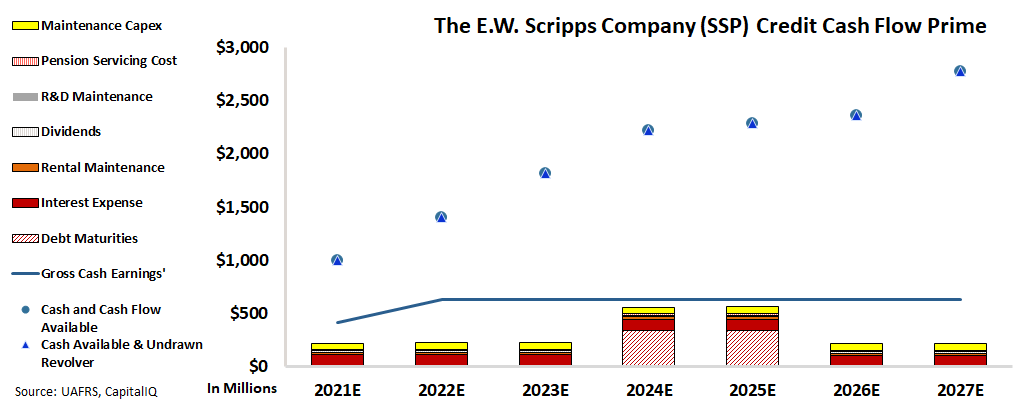

Our Credit Cash Flow Prime (CCFP) analysis is able to get to the heart of the firm’s true credit risk. And it shows a very different credit picture for the company.

In the below chart, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

As depicted, E.W. Scripps has massive cash liquidity and therefore should have no issues handling its obligations going forward. On top of this, even if the firm did not have access to this capital, cash flows alone exceed all obligations by a wide margin each year through 2027.

Rather than a name in distress, The E.W. Scripps is actually a cash flow machine. This is why S&P’s highly speculative rating of a B, with a 25%+ risk of default expectation, does not make sense.

Using the CCFP analysis, Valens rates The E.W. Scripps as an investment grade IG3- rating. This is equivalent to an investment grade A- rating from S&P.

Additionally, this rating corresponds with a default rate below 1% within the next five years, a more realistic projection once a holistic understanding of the company’s risk is taken into account.

Ultimately, Uniform Accounting and the Credit Cash Flow Prime analysis highlights how E.W. Scripps’ credit risk profile is much safer than what rating agencies believe.

Even though it has been a declining business due to the headwinds of more TV channel offerings and online streaming services, the company has been able to remain afloat, and is very unlikely to go bankrupt any time soon.

SUMMARY and The E.W. Scripps Company Tearsheet

As the Uniform Accounting tearsheet for The E.W. Scripps Company (SSP:USA) highlights, the Uniform P/E trades at 22.7x, which is around the global corporate average valuation levels but above historical average valuations of 21.3x.

Average P/Es require average EPS growth to sustain them. In the case of E.W. Scripps, the company has recently shown a 10,213% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, E.W. Scripps’ Wall Street analyst-driven forecast is a 31% EPS decline in 2021 and 55% EPS growth in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify E.W. Scripps’ $21.6 stock price. These are often referred to as market embedded expectations.

E.W. Scripps is being valued as if Uniform earnings were to grow 7% per year over the next three years. What Wall Street analysts expect for E.W. Scripps’ earnings growth is below what the current stock market valuation requires in 2021 but above the requirement in 2022.

Furthermore, the company’s earning power is 2x the corporate average and cash flows and cash on hand are twice its total obligations—including debt maturities, capex maintenance, and dividend. Also, intrinsic credit risk is 540bps above the risk free rate. Together, this signals a low credit and dividend risk.

To conclude, E.W. Scripps’ Uniform earnings growth is below peer averages and the company is trading above average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research