Start-up firms are normally a no-go for credit investors, Uniform Accounting analysis highlights why this negative-earnings business is different

Start-up companies are often avoided by equity investors due to their inherent risk and high valuations. These factors are even more applicable to credit investors, as they need to be more risk averse.

However, often, the market will condemn a start-up firm as a risky investment despite fundamental strengths in the balance sheet. As today’s firm continues to build liquidity and build a strong history of credit payments, it is likely the bond prices will recover.

Below, we show how Uniform Accounting restates financials for a clear credit profile.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Many investors tend to avoid putting their money with start-up firms for a variety of factors. There are no guarantees of future cash flows, as investors are unsure of the future demand of a product. With little prior performance, investors have no ability to benchmark performance.

Furthermore, start-up firms are often priced at sky-high valuations due to Wall Street’s excitement about potential future earnings.

Sometimes, after an initial public offering, a company will follow the example of Beyond Meat or Zoom and realize massive stock appreciation. However, for every Beyond Meat or Zoom, there is a pets.com or Groupon, firms who have struggled to live up to their initial expectations.

The aversion to chasing these stocks for value-oriented equity holders is multiplied for a credit investor. An equity investor is more willing to buy a firm at a massive valuation because of the potential for future disruption in a field. On the other hand, future earnings will not pay this year’s debts and make a credit investor back their principal.

However, credit investors have been skittish over the ride-sharing platform Uber (UBER) only because of its short history, not the strength of its balance sheet.

Uber, currently, has negative cash flows, which spooks credit investors. However, Uber also currently has sizable liquidity which would be able to cover all expenses through the next few years.

Furthermore, Uber currently has a massive market capitalization of $57 billion. To put this into perspective, Uber could issue enough equity to completely pay off its debt over the next five years and only dilute current equity holders by 9%.

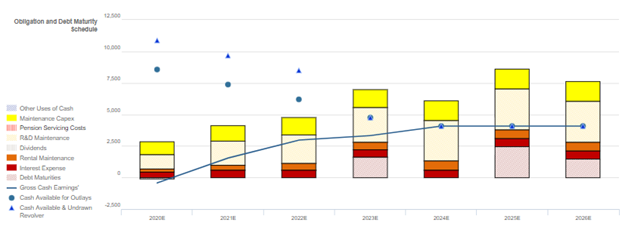

As you can see, with no debt headwalls until 2023, Uber is not in immediate risk of bankruptcy, as evident in the Credit Cash Flow Prime for the firm below.

This significant liquidity, combined with their sizable market capitalization, gives Uber flexibility in tackling their upcoming debt headwalls. By trimming maintenance capex or their sizable R&D spend, Uber should not have any issues with credit going forward.

However, this is not reflected in Ubers current high yielding debt of 6.1%. The market looks to Uber as a typical risky start-up company, and has priced it accordingly. However, due to this, the credit yield may be overstating the company’s true fundamental credit risk.

UBER’s Perceived Credit Risk is too Negative Despite its Healthy Credit Profile

Credit markets are grossly overstating credit risk with a cash bond YTW of 6.904% relative to an Intrinsic YTW of 0.984% and an Intrinsic CDS of 64bps. Meanwhile, Moody’s is materially overstating UBER’s fundamental credit risk with its highly speculative B2 credit rating five notches below Valens’ XO (Baa3) credit rating.

Fundamental analysis highlights that UBER’s cash flows should fall short of operating obligations in each year going forward.

However, following its recent debt issuances, the combination of the firm’s cash flows and ample cash on hand should be sufficient to cover all obligations including debt maturities until 2023, when the firm faces a material $1.6bn debt headwall.

Meanwhile, the firm has a multi-year debt runway to improve cash flows and ample capex and R&D flexibility to free up liquidity in the near-term. Furthermore, UBER’s large market capitalization and robust 340% recovery rate on unsecured debt should allow the firm access to credit markets to refinance if necessary.

Incentives Dictate Behavior™ analysis highlights mostly positive signals for investors. UBER’s compensation framework should drive management to focus largely on margin expansion and top-line growth, which should lead to Uniform ROA improvement.

Meanwhile, management members hold material amounts of UBER equity relative to their annual compensation, indicating that they are likely well-aligned with shareholders for long-term value creation.

Additionally, management members have low change-in-control compensation indicating they are not incentivized to pursue a buyout, and UBER’s large market capitalization limits event risk related to a sale of the company.

However, management is not penalized for overleveraging the balance sheet, increasing risk for credit holders and potentially reducing cash flows available for servicing debt obligations.

Earnings Call Forensics™ analysis of the firm’s Q1 2020 earnings call (5/7) highlights that management is confident their actions have resulted in a $1bn+ reduction in annualized fixed costs, that their Eats business should continue to grow due to the coronavirus pandemic, and that they put transit options on their app.

However, they are also confident that their Rides business declined so much that shared data is sparse. Moreover, they may be concerned about declines in Rides trips and gross bookings, global food industry business consolidation, and their headcount reductions.

In addition, they may lack confidence in their ability to sustain Eats gross bookings growth, achieve their long-term 15% take rate target, and continue to improve their cost structure.

Management may also be exaggerating the ability of their ATG investments to become profitable, their Eats existing customer engagement, and the technology, logistics, and local know-how necessary to operate at their scale on a global basis.

Finally, they may lack confidence in their ability to sustain Q2 growth rate improvements and promote social distancing through their app.

UBER’s ample cash on hand, robust recovery rate, and sizable market capitalization indicate that credit markets and Moody’s are overstating the firm’s fundamental credit risk. As a result, a tightening of credit spreads and a ratings improvement are both likely going forward.

SUMMARY and Uber Technologies, Inc. Tearsheet

As the Uniform Accounting tearsheet for Uber Technologies, Inc. (UBER:USA) highlights, the company trades at a negative 12.5x Uniform P/E, which is way below global corporate average valuation levels and its historical average valuations.

Negative P/Es only require low EPS growth to sustain them. That said, in the case of Uber, the company has recently shown a 41% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Uber’s Wall Street analyst-driven forecast projects no earnings growth in 2020, followed by a 68% shrinkage in 2021.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $33 per share. These are often referred to as market embedded expectations.

Meanwhile, the company’s earnings power is below corporate averages. Furthermore, total obligations—including debt maturities, maintenance capex, and dividends—are below total cash flows, and intrinsic credit risk is 64bps above the risk-free rate, signaling moderate risk to its dividend and operations.

To summarize, Uber is currently seeing above average peer Uniform earnings growth. However, the company is trading below peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research