This month’s screen yields a name that would never appear on investors’ radar without Uniform Accounting

Even those who created and oversaw corporate America’s accounting rules were aware of their inherent inconsistencies. They understood that leaving complex bookkeeping items to the discretion of accountants can easily distort comparability between companies and industries.

In response, the best investors understand the need for adjusting the financial statements, which provides a true picture of economic reality and allows them to find companies that exhibit three characteristics: high quality, strong growth potential, and low valuations.

Today, we highlight our QGV 50, which emulates this investment strategy to produce outsized returns in excess of the market over long periods of time.

We’ll take a look at one company in particular on this month’s QGV 50, describing how as-reported metrics distort economic reality and can lead investors to miss significant opportunities.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

Throughout financial market history, many of the most successful investors have consistently decried the shortcomings of common accounting practices.

Keen on analyzing the financial statements, they see accounting rules that often blur the lines between what is real and what is the result of mere discretion, making it difficult for them to compare apples-to-apples.

But it’s not only investors. Even the regulators themselves, who are responsible for creating the accounting rules and standards companies must follow, believe that Generally Accepted Accounting Principles (“GAAP”) distort economic reality.

Past Chairmen of the Financial Accounting Standards Board (“FASB”), which sets and improves upon GAAP, have even called the rules “internally inconsistent; misleading, confusing; inaptly named” and “likely to be misunderstood.”

Investors who neglect the very real issues with as-reported accounting can find themselves investing blindly, without a thorough grasp of how to understand the businesses in question.

In order to succeed, investors must develop a clear picture of how a business operates, something that can only be done by adjusting the financial statements to account for the arbitrary nature of certain bookkeeping standards.

The world’s best investors understand the need to make these adjustments, which allows them to focus not on picking out the most popular companies, but rather looking for great names in sleepy areas that the market isn’t paying much attention to. From there, the goal is to then identify quality companies with significant growth potential at reasonable prices.

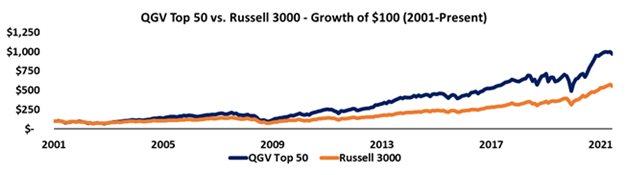

That’s exactly what we’ve set out to do with the QGV 50, our monthly list of 50 companies that rank at the top for quality, high growth, and low valuations.

This list has outperformed the market by 300bps per year for over 20 years now, effectively doubling the performance of the market by focusing on the real fundamentals and valuations of companies with our proprietary Uniform Accounting framework.

See for yourself below.

One of this month’s top QGV 50 names is StepStone Group (STEP), a specialized asset manager that helps pension funds and endowments get unique exposure to private markets.

The company allows its clients to create diversified, customly-tailored portfolios in areas like private equity and real estate to help them meet increasingly difficult investment return targets.

What’s interesting about StepStone is that it’s an independent provider of investment strategies, mostly through the separately managed accounts (“SMAs”) it offers.

This means the company is unencumbered by the conflicts of interest often faced by big names like Blackstone (BX) or BlackRock (BLK) that pension fund clients may already have exposure to.

Unlike these big players, whose products often pool money from many investors into large funds, StepStone adds value for clients by providing them individually constructed portfolios.

Instead of having to choose a large fund from the investment giants that most closely aligns with their objectives, StepStone lets its clients focus on exactly what they need to meet their goals.

Institutional investors, many of whom are faced with the increasing pressure of dwindling options to deliver promised returns, trust StepStone because of its unbiased approach to asset management.

Not to mention, the company’s process is incredibly scaleable.

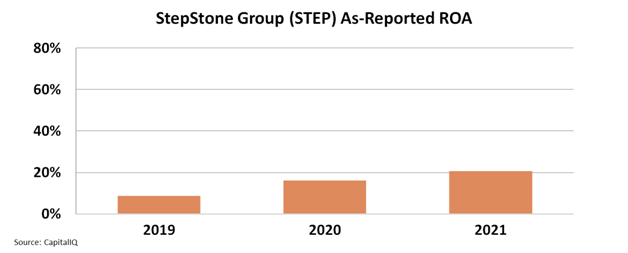

This trust and scalability first starts to come across when looking at as-reported metrics, which show that the firm’s as-reported return on assets (“ROA”) stood at an impressive 21% this past fiscal year, part of a trend of steadily increasing returns since 2019.

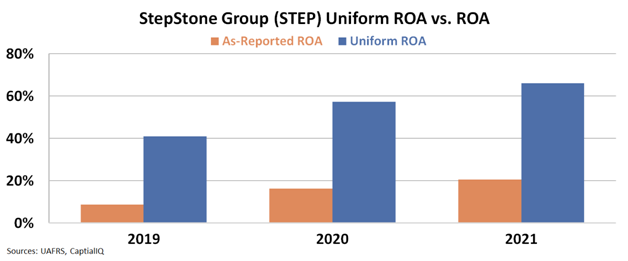

In reality, even these impressive figures understate how profitable StepStone and its suite of personalized portfolio solutions really are.

Looking at Uniform Accounting metrics, we can see that the firm’s real Uniform ROA was 66% last year, as clients rushed to StepStone’s offerings to get exposure to private markets. At the same time, the company has been able to aggressively re-invest in its future, with Uniform asset growth of 68% in 2021.

With a Uniform price-to-earnings ratio (“P/E”) of just 7.7x, StepStone is a high-return, high-growth company that is also trading well below market averages.

But most importantly, investors relying on as-reported metrics might miss this quality, growth, and value story altogether, as GAAP figures show an as-reported P/E of 40.5x, making it seem like the market already understands the potential of StepStone’s business.

Looking at economic reality through the lens of Uniform Accounting, we can see that StepStone isn’t just a robust high-growth name, it’s also inexpensively valued as well, which is why it was flagged by this month’s QGV 50.

If it were easy to find great companies with growth potential trading at favorable prices, professional investors would be out of the job. And yet, with Uniform Accounting it is, and that’s why the QGV 50 has had such tremendous success beating the market over the years.

To learn more about the QGV 50 and see the other 49 companies on the list this quarter, click here to get full access today.

SUMMARY and StepStone Group Inc. Tearsheet

As the Uniform Accounting tearsheet for StepStone Group Inc. (STEP:USA) highlights, the Uniform P/E trades at 7.7x, which is below the global corporate average of 24.3x, but above its historical P/E of 3.5x.

Low P/Es require low EPS growth to sustain them. In the case of StepStone, the company has recently shown an immaterial Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, StepStone’s Wall Street analyst-driven forecast is an 11% EPS shrinkage in 2022 and immaterial EPS growth in 2023.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify StepStone’s $47 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 2% annually over the next three years. What Wall Street analysts expect for StepStone’s earnings growth is below what the current stock market valuation requires in 2022, but near that requirement in 2023.

Furthermore, the company’s earning power in 2021 is 11x above the long-run corporate average. Moreover, cash flows and cash on hand are 29x its total obligations—including debt maturities and capex maintenance. All in all, this signals a low credit risk.

Lastly, StepStone’s Uniform earnings growth is in line with peer averages, but the company is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research