This supplier benefits from the unexpected rise of home construction

The housing construction market has been going pretty strong against the odds. Most investors thought rising interest rates and mortgages would hurt home sales and new construction, but that proved wrong.

While high mortgage rates do make some people not buy, it also makes homeowners not sell so they don’t lose their incredibly cheap mortgages. In the meantime, some people have to buy new homes and turn to newly constructed buildings.

This sustained demand, combined with the rising prices of lumber, metal, and other construction materials due to inflation, benefited construction supplier companies.

Boise Cascade (BCC) is a good example of those. The company sells lumber and other construction items such as doors, decking, metal products, and roofing. As the company’s profits surged in recent quarters, its stock price has also risen sharply.

However, the market does not believe that it would continue like that, being overly pessimistic. It fails to acknowledge that as long as the industry is strong, the company will do well.

Thus, Boise Cascade showed up on our screen. The company makes a great FA Alpha 50 name due to its potential for high returns and low expectations from the market.

Investor Essentials Daily:

Tuesday FA Alpha 50

Powered by Valens Research

The housing market has been volatile in recent years, with periods of high demand followed by periods of low demand.

This volatility is being driven by a number of factors, including the pandemic, the state of the economy, and rising interest rates.

Surging inflation led to the most aggressive interest rate policy by the Fed ever, causing mortgage rates to increase. Most investors thought this would be the end of the housing bubble. Demand and prices would fall, and construction would stop.

They couldn’t be more wrong…

High interest rates certainly slowed down demand for home purchases. But it turns out high mortgages also mean that existing homeowners do not want to sell.

If they did, they would have to lock in a much higher mortgage rate on their purchase instead of the near 0% rates they secured during the pandemic.

While this is the case, there are people that have to buy a home to build a life. They might get married, have children, work or study at a new location, or just simply move for other reasons.

With existing homes not available, there is only one place they can go to: the construction companies.

The industry is well alive, and now these companies are supplying the entirety of the demand for houses. A lot of construction companies already benefited from this trend in the last two years.

Another big beneficiary of this is the suppliers of the construction industry, such as Boise Cascade (BCC).

It manufactures and distributes wood products and building materials that are used in residential, commercial, and industrial applications by homebuilders, contractors, and retailers.

The rising demand for construction combined with higher prices of the materials produced resulted in high profitability for the company.

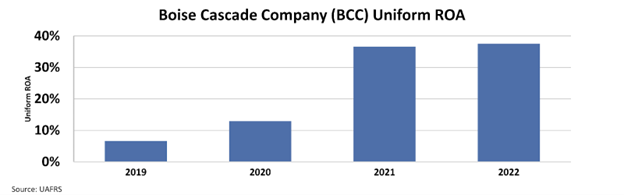

Boise Cascade’s return on assets (“ROA”) jumped from 13% in 2020 to 37% in 2021, which it managed to sustain in 2022.

The chart shows that the company performs incredibly when the construction sector is strong. As long as construction firms operate as it is, we might see even higher returns.

And yet, the market fails to recognize this opportunity.

We can see this through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market expects the company’s ROA to fall below 9%, assuming the demand will collapse.

Given the improvements in the construction sector and the company’s essential position in its supply, these expectations seem overly pessimistic.

Boise Cascade has substantial potential to scale its operations and achieve greater prominence.

That is why Boise Cascade showed up on our screen. The company makes a great FA Alpha 50 name due to its potential for high returns and low expectations from the market.

Throughout financial market history, many of the world’s most successful investors have been candid in their belief that Generally Accepted Accounting Principles (“GAAP”) distort economic reality.

Warren Buffett, for example, once said investors should “concentrate on the world of companies, not arcane accounting mathematics.”

Investors who neglect the very real issues with as-reported accounting can find themselves caught up in investing with the crowd, blindly following hot “themes” without a thorough grasp of how to understand the businesses in question.

The only true way to focus on the “world of companies,” as Buffett suggests investors do, is to present a clear picture of how a business operates, something that can only be done by adjusting financial statements to reflect the arbitrary nature of certain accounting rules that leave much to discretion.

The world’s best investors understand the need to make these adjustments, which allows them to focus not on picking out the most popular companies but rather on looking for great names in sleepy areas that the market isn’t paying much attention to. From there, the goal is to then identify quality companies with significant growth potential at reasonable prices.

That’s exactly what we’ve set out to do with the FA Alpha, our monthly list of 50 companies that rank at the top for quality, high growth, and low valuations.

This list has outperformed the market by 300 basis points per year for over 20 years now, effectively doubling the performance of the market by focusing on the real fundamentals and valuations of companies with our proprietary Uniform Accounting framework.

See for yourself below.

To see the other 49 names on the list, click here.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research