This supply chain gem is hidden by the as-reported metrics

We are finally improving our supply chains, and various companies, from industrials to technology, are contributing to it.

However, the potential in this field has been hidden for a while because of the distorted as-reported metrics. A great example of this is the logistics leader C.H. Robinson Worldwide (CHRW).

The as-reported numbers make it seem like the company is barely generating returns of around 10%. However, Uniform Accounting reveals the real picture and shows how much more profitable the company actually is.

That’s why it showed up on our FA Alpha Screen. The market’s lack of understanding of its high returns, the company’s high growth, and low valuations make it a great name.

Investor Essentials Daily:

Tuesday FA Alpha 50

Powered by Valens Research

Supply chain investments are a hot topic at the moment.

The extended lead times and unavailability of products made the U.S. and companies step in to improve their supply chains in order to become more resilient.

Industrial companies are bringing their manufacturing facilities back home from places where they could produce more cheaply. They are also investing in their own infrastructure to provide services to areas that were not possible before.

However, they are not the only ones ramping up their investments in this field. As we talked about last Thursday, there is another set of companies that have seen the potential in supply chains.

These are the technology companies. They are finally making investments in the race to catch up in the world of logistics.

The potential in logistics has been hidden for a while because of distorted as-reported metrics, and a great example of that is the logistics leader C.H. Robinson Worldwide (CHRW).

The company provides freight transportation services and logistics solutions to companies in various industries worldwide.

It has seen demand go up as all the companies tried to navigate through the harsh supply chain environment. With the increasing investments in the space, it will continue to recognize macroeconomic tailwinds.

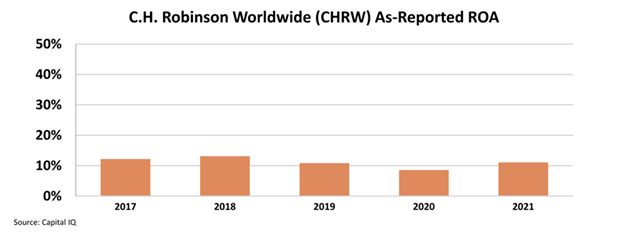

The as-reported return on assets (“ROA”) makes it seem like the company is barely generating returns of around 10%, which is even worse than the corporate averages in the U.S.

The company had a difficult year as the pandemic hit in 2020, and the ROA fell to 9% before recovering to 11% in 2021.

However, for a company that provides essential services for all the other industries, this level of profitability seems low.

This is because of the distortions in as-reported accounting. We can fix it by making more than 130 adjustments needed under Uniform Accounting and uncover the real potential of the logistics business.

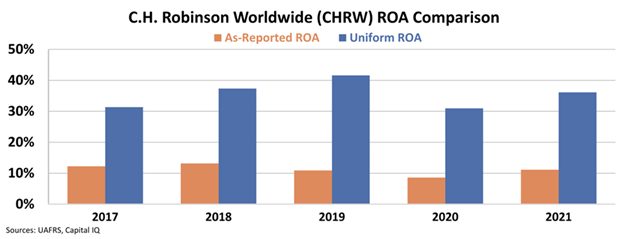

The picture Uniform Accounting shows is incredibly different from what the as-reported accounting suggests.

The Uniform ROA of the business was 42% in 2019. It dropped to 31% during the pandemic and recovered to 36% in 2021, as good as many software firms.

In the last five years, even the least profitable year under Uniform Accounting is much more profitable than the most profitable year under as-reported accounting.

Investors are looking at the wrong numbers, and the market fails to understand how the investments being made because of the Supply Chain Super Cycle may affect the business.

As these investments continue over the next decade, C.H. Robinson Worldwide has the capacity to use its assets more efficiently and be more profitable.

The market’s lack of understanding of the company’s high returns, high growth, and low valuation means that C.H. Robinson Worldwide is a great FA Alpha 50 name.

Throughout financial market history, many of the world’s most successful investors have been candid in their belief that Generally Accepted Accounting Principles (“GAAP”) distort economic reality.

Warren Buffett, for example, once said investors should “concentrate on the world of companies, not arcane accounting mathematics.”

Investors who neglect the very real issues with as-reported accounting can find themselves caught up in investing with the crowd, blindly following hot “themes” without a thorough grasp of how to understand the businesses in question.

The only true way to focus on the “world of companies,” as Buffett suggests investors do, is to present a clear picture of how a business operates, something that can only be done by adjusting financial statements to reflect the arbitrary nature of certain accounting rules that leave much to discretion.

The world’s best investors understand the need to make these adjustments, which allows them to focus not on picking out the most popular companies but rather on looking for great names in sleepy areas that the market isn’t paying much attention to. From there, the goal is to then identify quality companies with significant growth potential at reasonable prices.

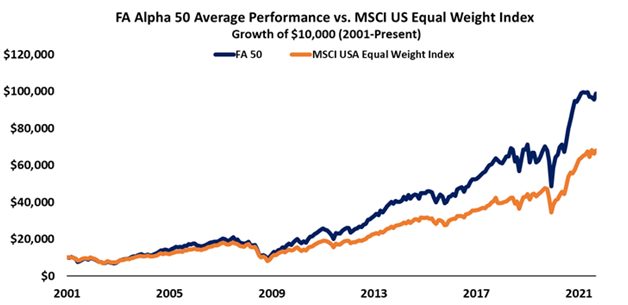

That’s exactly what we’ve set out to do with the FA Alpha, our monthly list of 50 companies that rank at the top for quality, high growth, and low valuations.

This list has outperformed the market by 300 basis points per year for over 20 years now, effectively doubling the performance of the market by focusing on the real fundamentals and valuations of companies with our proprietary Uniform Accounting framework.

See for yourself below.

To see the other 49 names on the list, click here.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research