This toolmaker is quietly making a killing by supporting America’s housing boom

Wall Street—and Main Street for that matter—loves a good story.

Whether it is flashy special purpose acquisitions companies (SPACs) or unprofitable tech darlings, the past year and a half have demonstrated the euphoria markets can exhibit for the “new” and exciting.

Today’s company is nothing of the sort. It is a simple manufacturer of industrial tools and equipment, hardware items, and security products.

Perhaps a boring business on the surface, but when viewed through a Uniform Accounting lens, it becomes clear there is plenty to excite investors.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

By today’s standards, Stanley Black & Decker (SWK)—perhaps best known for its DeWalt power tools—is an incredibly boring business.

With markets infatuated by the prospects of new technologies such as artificial intelligence and electric vehicles, manufacturing tools simply fail to excite.

Fortunately for those skeptical of crowds and concerned with real business fundamentals, seemingly uninspiring companies such as Stanley Black & Decker may actually present attractive investment opportunities.

This is especially true today, with stock markets trading at or near all-time highs around the world.

Oftentimes, when the hype fades and markets adjust, the companies best positioned are those with a long history of stability, strong assets, and high returns.

Yet, sorting genuine value from the cacophony of companies that make up the stock market is a truly difficult task—one best suited for those able to properly analyze the real, undistorted economic picture of companies in question.

Stanley Black & Decker is a prime example of how investors can be led astray by as-reported financials.

While the company does produce a range of essential items, given the wide variety of existing tool brands available on the market, one would expect it to largely operate a low-return, commodity business.

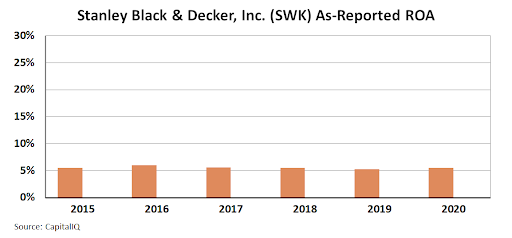

Looking at as-reported return on assets (ROA) of around 4%-6% over the last six years, this thesis would appear to be confirmed, making Stanley Black & Decker appear to be a cost-of-capital business at best.

However, in reality the company’s valuable brands, ranging from its namesake Stanley and Black & Decker brands to the more industrial Paladin and Pengo, have made it an impressively resilient and high return business, with Uniform ROA actually around 25% levels over the past decade, well above the corporate averages around 12%.

This discrepancy illustrates just how misleading as-reported figures can be.

Stanley Black & Decker is an incredibly stable, high return business with a slew of strong brands and a long history of successful acquisitions.

Yet, relying solely on as-reported metrics would lead to a fundamentally different picture of the company – one which would not reflect economic reality.

SUMMARY and Stanley Black & Decker, Inc. Tearsheet

As the Uniform Accounting tearsheet for Stanley Black & Decker, Inc. (SWK:USA) highlights, the Uniform P/E trades at 20.3x, which is below the global corporate average of 23.7x, but above its own historical average of 18.0x.

Low P/Es require low EPS growth to sustain them. In the case of Stanley Black & Decker, the company has recently shown a 14% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Stanley Black & Decker’s Wall Street analyst-driven forecast is a 6% and 9% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Stanley Black & Decker’s $208 stock price. These are often referred to as market embedded expectations.

The company needs to have Uniform earnings grow by 3% per year over the next three years in order to justify current stock prices. What Wall Street analysts expect for Stanley Black & Decker’s earnings growth is above what the current stock market valuation requires in 2021 and 2022.

Furthermore, the company’s earning power is 5x the long-run corporate average. Also, cash flows and cash on hand are almost 3x its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a low credit and dividend risk.

To conclude, Stanley Black & Decker’s Uniform earnings growth is well below its peer averages. However, the company is trading well below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research