This Company Has Doubled Due to Low Inflation, but That May Be Coming to an End

In the land of distribution, especially food distribution, inflation and volumes are king.

The way a distributor makes money, quite simply, is by being the warehouse and logistics connection between sellers and buyers.

By aggregating products from suppliers they can get more customers who don’t want to have to get things piecemeal. By aggregating demand from customers they can negotiate the best prices from suppliers by buying in larger volumes, helping profitability and making them more competitive versus peers.

The importance of high volumes for distributors is obvious. If a distributor can have higher volume, they don’t just get good discounts, they also can turnover their inventory of goods more often in a year.

Higher volumes means higher revenue, more revenue per dollar tied up in inventory, so higher returns. It also means higher profits because the company is getting higher utilization of their fixed warehouse and distribution fleet. The benefit of high volumes is obvious, as is the reverse when volumes decline.

Inflation is another key factor that impacts the profitability of distributors. There is often a lag for their ability to raise prices, versus the cost of their goods rising. In the short-term this can squeeze margins in a highly inflationary environment. When there is a rare moment of deflation, it would be helpful, but generally the benefit there is offset by issues with volumes.

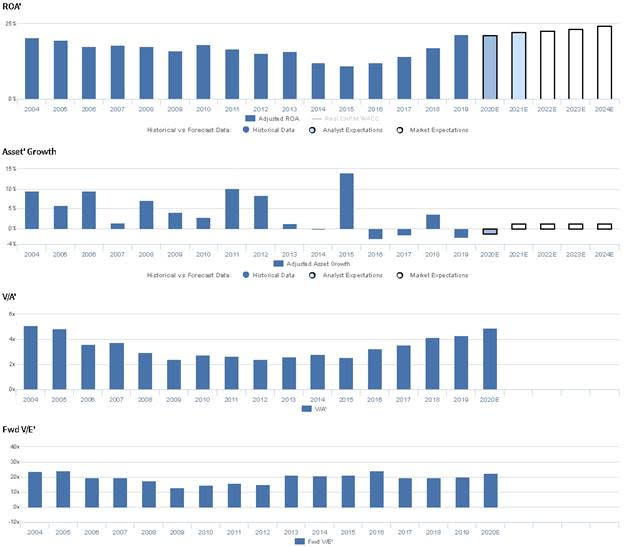

Over the past few years Sysco (SYY), a distributor of food and other restaurant supplies to the restaurant industry has benefitted from increased volumes for their products, and also from relatively tame inflation. Because of those two drivers, Sysco’s Uniform ROA has doubled since 2015, and the stock has also.

At current valuations, the market is expecting Sysco to continue to have this beneficial environment going forward, of low inflation and strong volume growth. The market is pricing Sysco to see Uniform ROA, which is already at all-time peaks, to continue to rise going forward. But management is growing more concerned about their outlook for food costs and inflation, and they’re concerned about volume and revenue growth trends, which could lead to the market having to lower expectations.

Market expectations are for Uniform ROA to reach new peaks, but management may be concerned about food cost, revenue, and volume growth

SYY currently trades slightly above historical averages relative to UAFRS-based (Uniform) Earnings, with a 22.7x Uniform P/E. At these levels, the market is pricing in expectations for Uniform ROA to expand from 22% in 2019 to 24% in 2024, accompanied by 1% Uniform Asset growth going forward.

Analysts have less bullish expectations, projecting Uniform ROA to sustain 22% levels through 2021, accompanied by 1% Uniform Asset shrinkage.

Historically, SYY saw fading profitability levels, which have rebounded in recent years. Uniform ROA slowly compressed from 21% in 2004 to 11%-12% levels in 2014-2016, driven by deflationary pricing environment headwinds and a failed US Foods merger, before rebounding to 22% in 2018. Meanwhile, Uniform Asset growth has been somewhat volatile, positive in 12 of the past 16 years, though leaning more negative in recent years, while ranging from -3% to 14%.

Performance Drivers – Sales, Margins, and Turns

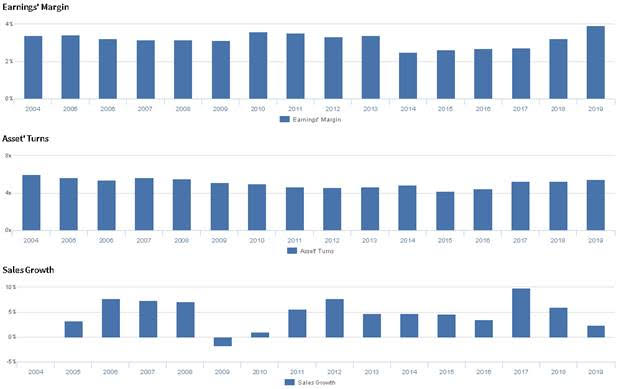

Trends in Uniform ROA have been driven by trends in both Uniform Earnings Margin and Uniform Asset Turns. After improving from 3% in 2004-2009 to 4% in 2010-2011, Uniform Margins regressed back to 3% levels from 2014-2018 before returning to 4% in 2019. Meanwhile, Uniform Turns steadily declined from 6.0x in 2004 to 4.2x in 2015, before rebounding to 5.5x through 2019. At current valuations, markets are pricing in expectations for Uniform Margins and Uniform Turns to continue expanding.

Earnings Call Forensics

Valens’ qualitative analysis of the firm’s Q1 2020 earnings call highlights that management may be concerned about further top-line softness in 2020 and about the impact of food cost inflation on profitability. Furthermore, they may be exaggerating the incremental business opportunities they expect to see given their market share, and they may lack confidence in their ability to sustain local case volume growth. Finally, they may be concerned about the effectiveness of their talent acquisition model, and they may lack confidence in their ability to meet their pipeline execution guidance.

UAFRS VS As-Reported

Uniform Accounting metrics also highlight a significantly different fundamental picture for SYY than as-reported metrics reflect. As-reported metrics can lead investors to view a company to be dramatically stronger or weaker than real operating fundamentals highlight. Understanding where these distortions occur can help explain why market expectations for the company may be divergent.

As-reported metrics significantly understate SYY’s profitability. For example, as-reported ROA for SYY was 9% in 2019, materially lower than Uniform ROA of 22%, making SYY appear to be a much weaker business than real economic metrics highlight. Moreover, while Uniform ROA rebounded from 11% in 2015 to 22% in 2019, as-reported ROA only improved from 7% to 9% over the same period of time, significantly distorting the market’s perception of the firm’s recent profitability trends.

Today’s Tearsheet

Today’s tearsheet is for Accenture. Accenture trades at market average valuations. The company has recently had double digit 13% Uniform EPS growth. EPS growth is forecast to moderate to 4%-6% a year the next two years. At current valuations, the market is pricing the company to see earnings stay flat going forward.

The company’s earnings growth is forecast to be in line with peers, but company is trading at a slight discount to peer average valuations. The company has strong returns, and no risk to their dividend.

Regards,

Joel Litman

Chief Investment Strategist