Tariffs can eat into this tech company’s profits

Tariff fears sent shockwaves through the market after President Trump unveiled an extensive plan, triggering steep declines in major indices and heavy sell-offs in stocks with international exposure.

Technology hardware companies like HP (HPQ) and Dell were particularly hard hit, with HP experiencing its largest intraday drop in years due to concerns over increased costs and limited profit margins.

These additional tariff costs, combined with HP’s existing profitability challenges and rising debt, could force the company to pass on costs to consumers, potentially dampening sales and eroding shareholder returns.

Investor Essentials Daily:

Friday News-based Update

Powered by Valens Research

With tariff fears rocking the market this week, we focused on the companies that are possibly more shielded from the downside this week.

When President Trump unveiled his extensive tariff plan last week, markets responded with immediate concern.

The S&P 500 fell by 4.8%, the Dow Jones Industrial Average dropped 4%, and the Nasdaq plummeted by 6% in a single trading day.

Investors moved quickly to shed stocks with international exposure as they feared potential damage to corporate profits across industries.

Some of the companies hardest hit from tariffs are technology hardware firms like Dell and HP (HPQ).

HP saw its shares plummet 13% in a single day, pushing the stock price to its lowest point since early January 2021, marking the company’s largest intraday drop since 2019.

This reflects serious concerns about how new tariff policies will impact the company’s already challenged business model.

The immediate trigger for HP’s sell-off was the announcement of tariffs up to 54% on imports from China, now up to 145%.

With gross margins already below 20%, the company has little room to absorb these expenses without passing them to consumers.

Price hikes, however, risk further dampening demand in an already soft market for PCs and printers.

Even before the tariff announcement, HP was dealing with significant headwinds.

The company has been struggling to meaningfully grow its top line for several years, while its bottom line continues to show concerning declines.

In its first quarter 2025 results, HP reported a modest 2% revenue increase year-over-year, a 2% decrease in gross profit, a 10% drop in operating profit, and a 9% decline in net income.

These results show HP’s ongoing profitability challenges, with net profit margins declining from 7% to just 4% since 2020.

The company’s debt position also remains a worry.

HP has over $1 billion in current debt that matures in 2025, which it has not reduced since Q3 2024.

Without significant improvement in revenue and profitability, maintaining both debt service and shareholder returns will be increasingly difficult.

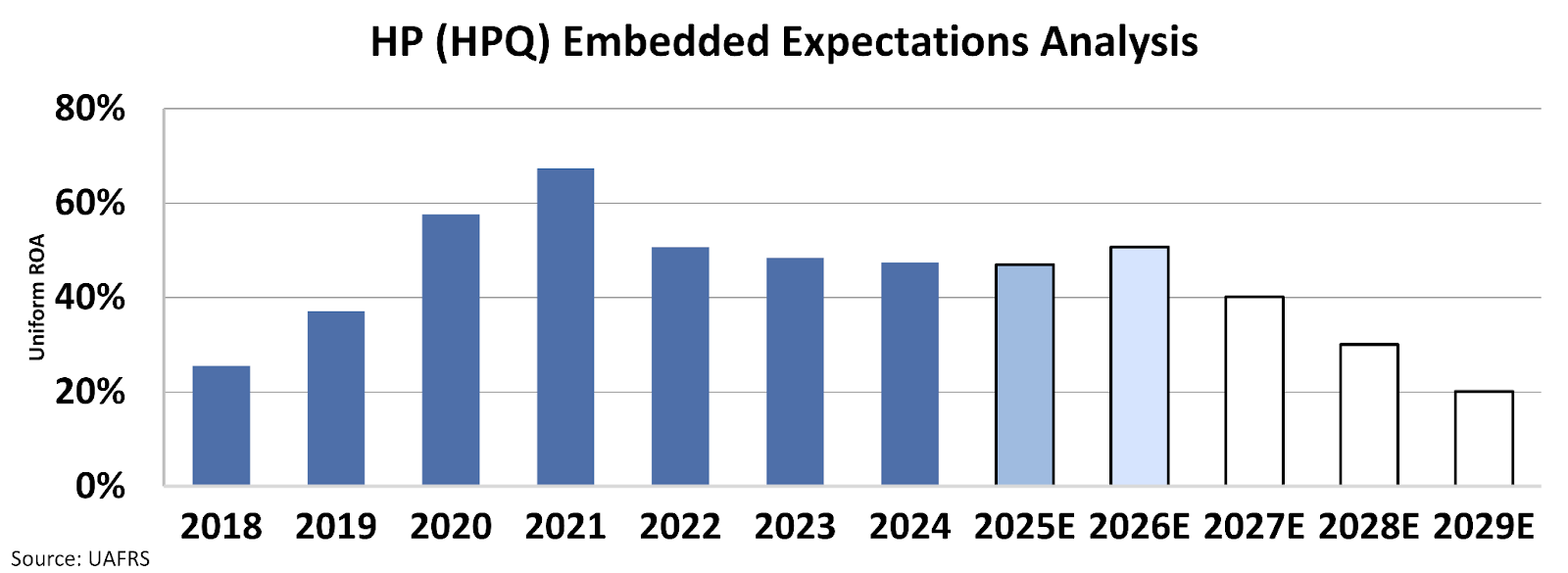

The market is aware of all these headwinds and prices in HP’s future accordingly.

We can see what the market thinks through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market predicts that the company’s Uniform return on assets ”ROA” declined to 20% from 47% last year.

The additional costs associated with tariffs are an almost insurmountable headwind.

For companies with already narrow profit margins and high material expenses, the tariffs could force a reconsideration of growth strategies and might even trigger an erosion of shareholder yields.

Investors are aware that the technology hardware market has limited flexibility when it comes to raising prices without sacrificing demand, especially in the current economic climate.

The situation is further complicated by potential operational adjustments.

HP is expected to pass the costs along to its customers, a move that might curtail sales in a market already witnessing low growth.

Even if revenue growth picks up modestly, sustaining profit margins could be a challenge.

Investors should be cautious investing in companies that could be significantly affected from tariffs like HP.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research