Not all companies have the same standards for taking on leverage, with today’s firm being a special case

Using a leverage ratio is an easy way to measure the credit profile of a firm. Firms with levels too high deserve higher bond yields since they are riskier. Better ratios warrant lower yields.

However, not all firms have the same target for a healthy credit ratio. Today’s firm is able to maintain an above average credit ratio due to its unique operations, which the market isn’t fully understanding.

Below, we show how Uniform Accounting restates financials for a clear credit profile.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

A key standard for credit investors is looking at the leverage ratio of a firm. A firm’s leverage ratio is the percentage of its debt in relation to its earnings before interest, taxes, depreciation, and amortization (EBITDA).

By looking at firms through the lens of leverage ratios, a credit analyst can get a quick understanding of how well a company can service its debt from cash flows.

If a firm’s leverage ratio is too high, it could mean the management team was reckless, taking on more debt than could be serviced in an effort to drive growth.

However, if the leverage ratio is too low, it could indicate to investors management is purposefully avoiding some amount of healthy debt. Management could have no sound strategy for growth, or the C-Suite is concerned over the strength of future cash flows.

The largest factor in determining how much leverage a firm can take on is the volatility of its returns. Companies with stable earnings can handle higher leverage because they are able to plan out their interest expense and debt servicing year after year without difficulty.

Equity investors love if these types of firms can increase their leverage, as this directly improves return on equity (ROE). This ability to take on leverage compounds the higher these stable earnings are, as more interest can be covered.

A great example of this kind of company is Transdigm (TDG). Transdigm is run by former private equity (PE) executives who have applied their expertise in the PE space to a T for Transdigm.

Transdigm uses significant leverage to acquire aerospace firms that have successfully locked one of their parts into a successful airframe. Then, Transdigm shuts off all R&D spend to maximize the cash flow of the business and pay down the debt.

By expertly navigating this business cycle for different aerospace companies, Transdigm is able to maintain a high leverage ratio and put out large, consistent earnings. However, the debt market rates Transdigm debt as a risky asset, with bond yields of 5.7%, due to the large amount of debt on its balance sheet.

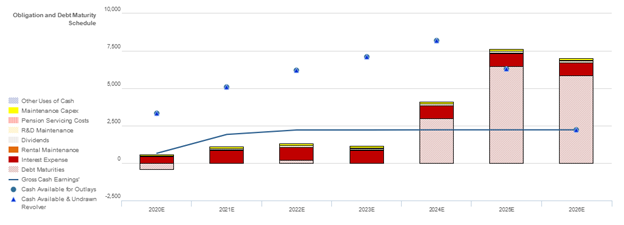

As you can see from the Credit Cash Flow Prime, Transdigm is currently able to pay all of its obligations with cash flows alone through 2023, and cover 2024 through its cash on hand.

While Transdigm’s leverage ratio is high, it’s important to not look at a single metric in a vacuum. By using Uniform Accounting and the Credit Cash Flow Prime, we can see that the company’s high cash flows leave Transdigm able to continue servicing its obligations.

The big spread between cash flows and obligations also means it’s likely creditors will let the company refinance its debt. With no debt maturities in the next few years, the firm will have no issues continuing to execute on its strategy.

The market is pricing Transdigm as a high yield bond, a firm that could have liquidity issues going forward. The reality is quite different and so investors are being overcompensated for the company’s real credit risk.

TDG’s Strong Cash Flows and Healthy Liquidity Merit Ratings Improvement

Credit markets are grossly overstating TDG’s credit risk with a YTW of 5.735% and a CDS of 440bps, relative to an Intrinsic YTW of 2.245% and an Intrinsic CDS of 236bps.

Meanwhile, S&P is overstating the firm’s fundamental credit risk, with their highly speculative B+ credit rating three notches lower than Valens’ XO- (BB+) credit rating.

Fundamental analysis highlights that TDG’s cash flows should comfortably exceed operating obligations in each year going forward.

Moreover, the combination of the firm’s cash flows and healthy liquidity levels should allow it to navigate all obligations including debt maturities until 2025 when the firm faces a material $6.5bn debt headwall.

That said, the firm has an ample debt runway to improve its future cash flows, and despite a non-existent recovery rate, the firm’s sizable market capitalization and history of successful refinancing should allow access to credit markets to refinance, if necessary.

Incentives Dictate Behavior™ analysis highlights mostly negative signals for credit holders. TDG’s compensation framework should drive management to focus on margin expansion and revenue growth, which should lead to Uniform ROA expansion and higher cash flows available for servicing obligations, but may also incentivize management to overleverage the balance sheet and overspend on assets.

In addition, management members do not hold material amounts of TDG equity, indicating they may not be well-aligned with shareholders for long-term value creation.

That said, management members are not well compensated in a change-in-control scenario, limiting event risk for creditors.

Earnings Call Forensics™ of the firm’s Q2 2020 earnings call (5/5) highlights that management may be exaggerating their M&A outlook, and might be concerned about continued coronavirus headwinds.

Moreover, they may be concerned about their ability to meet EBITDA margin expectations and about further supply and demand headwinds going forward.

Finally, they may be concerned about greater than expected headwinds in the OEM market, and weakness in passenger miles going forward.

TDG’s strong cash flows, healthy liquidity, and sizable market capitalization indicate that credit markets and S&P are overstating credit risk. As such, a tightening of credit spreads and ratings improvement are likely going forward.

SUMMARY and TransDigm Group Incorporated Tearsheet

As the Uniform Accounting tearsheet for TransDigm Group Incorporated (TDG:USA) highlights, the company trades at 27.0x Uniform P/E, which is above global corporate average valuation levels and its historical average valuations.

High P/Es require high EPS growth to sustain them. That said, in the case of TransDigm, the company has recently shown an 80% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, TransDigm’s Wall Street analyst-driven forecast projects a 41% shrinkage in 2020, followed by an 11% shrinkage in 2021.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $426 per share. These are often referred to as market embedded expectations.

Furthermore, the company’s earnings power is 8x the corporate average. Furthermore, total obligations—including debt maturities, maintenance capex, and dividends—are above total cash flows. However, cash flows and cash on hand will be insufficient to service material debt headwalls starting in 2025, signaling high dividend risk and credit risk.

To summarize, TransDigm is currently seeing below average Uniform earnings growth, but the company is trading in line with peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research