Tesla’s 2024 reality check

In 2024, the electric vehicle (“EV”) industry faced significant challenges, including disappointing sales, valuation drops, and a slower pace of growth.

Tesla’s growth rate declined, Apple canceled its EV project due to low demand signals, and General Motors delayed its phase-out of gasoline vehicles.

High-profile EV startups like Rivian, Lucid, and Fisker saw substantial valuation declines after failing to meet targets.

Tesla’s valuation dropped significantly, reflecting adjusted market expectations.

While the EV market’s future remains promising, mainstream adoption is now understood to be a longer and more complex process than previously anticipated.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

The once high-flying electric vehicle industry has hit turbulence in 2024 as disappointing sales reports and valuation adjustments have exposed the challenges of scaling a new technology.

After years of hypergrowth fueled by optimism around EVs, the reality of mainstream adoption has set in with demand failing to meet inflated expectations.

EV sales year-over-year growth slowed to 50% in 2023 – a stark contrast from the triple-digit increases investors had grown used to.

This signaled mainstream adoption may not follow the exponentially rising curve that bullish forecasts predicted.

In February 2024, Apple (AAPL) delivered another blow when it abruptly canceled “Project Titan” after a decade of secret development work on an electric vehicle. The tech giant admitted demand signals did not justify the massive investments required to enter the automotive market.

Around the same time, General Motors (GM) pushed back its timeline for phasing out gasoline vehicles by 5 years to 2040, acknowledging consumer behavior is changing more gradually than planned.

Other brands like Ford (F) also felt pressure, delaying some EV launches amid weaker demand.

The negative headlines continued as darling startups like Rivian (RIVN) saw their valuations plunge over 80% after missing production targets and raising costs significantly.

Lucid (LCID), Arrival (OTCMKTS:ARVLF), and Fisker (FSR) all lost billions in market value as well.

The flurry of disappointing news shook confidence in an industry that had been priced for relentless gains.

Tesla (TSLA), which traded at over 300 times earnings at its 2021 peak, lost close to 60% of its valuation as expectations adjusted.

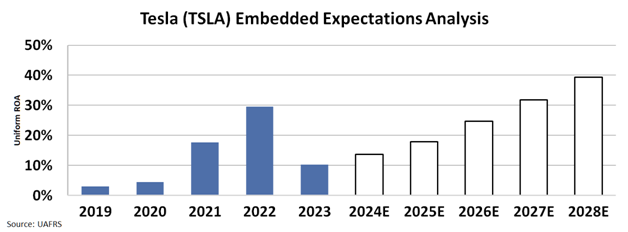

Despite this, Tesla is still priced for a big surge in Uniform return on assets (‘‘ROA’’).

Take a look…

However, this surge in Tesla’s ROA might not materialize due to the numerous demand headwinds facing the electric vehicle industry.

With sales growth slowing across the sector, Tesla will find it increasingly challenging to continue expanding deliveries at the breakneck pace of the past.

Rising costs from inflation and supply chain issues are also squeezing automaker margins.

As a result, investing in Tesla currently involves a significant amount of risk, as the stock remains priced for high earnings growth that now appears unlikely to unfold given the cooling EV market.

2024 has shown mass adoption of EVs will be a long slog, not a smooth upward curve.

While EVs represent the future, mainstreaming technologies on this scale takes decades of investment and problem-solving as realities replace visions of perfection.

The industry turbulence has brought valuations back to earth and expectations in line with the challenges ahead.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research