The Fed has opened the floodgates for the next phase of the economic cycle

For most of the past two years, the Federal Reserve has been quietly draining liquidity from the financial system through quantitative tightening.

The Fed has been buying from banks less and less. It effectively refused to let banks lend to it. And that leads to a problem. If QT goes on for too long, banks run out of places to lend their money.

However, it seems the Fed is finally ending QT, as it formally announced in late October last year that it would end it by December 1.

Officially, the move was described as a “technical adjustment.” In reality, it’s a clear sign that the Fed wants to stimulate the economy.

And for investors, this means that banks will be more comfortable lending again.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

Banks are at their limit.

For most of the past two years, the Federal Reserve has been quietly draining liquidity from the financial system.

Interest-rate hikes grabbed most of the headlines. But the central bank was also applying a more subtle force through quantitative tightening (“QT”).

QT is a way for the Fed to influence the money supply. It can cool down the economy by selling investments like U.S. Treasurys or mortgage-backed securities. Or it can choose not to reinvest the proceeds from maturing Treasurys, essentially sitting on cash instead of injecting it back into the economy.

When the Fed is growing its balance sheet, it’s called quantitative easing (“QE”)—the opposite of QT. QE means the Fed is buying assets, usually from banks.

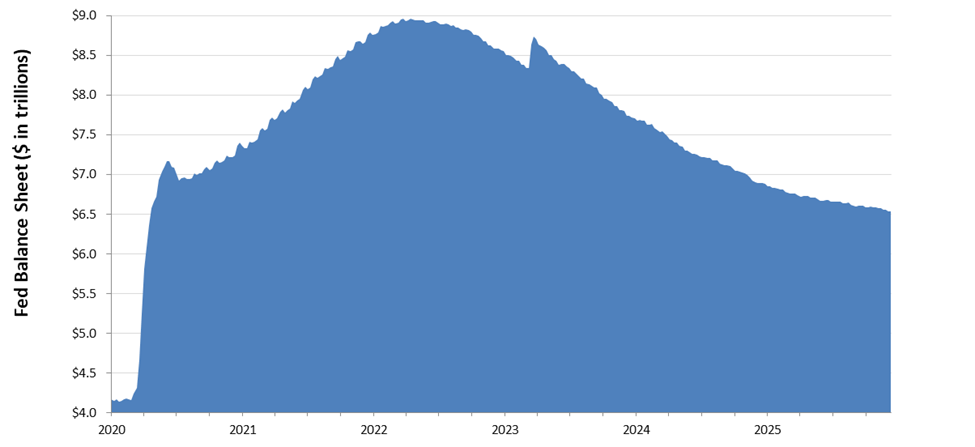

Because of this dynamic, the Fed’s balance sheet is a good proxy for bank reserves (meaning the cash banks have parked with the Fed). And as seen in the chart below, that balance sheet has been sliding for years.

The Fed has been buying from banks less and less. It effectively refused to let banks lend to it.

And that leads to a problem. If QT goes on for too long, banks run out of places to lend their money.

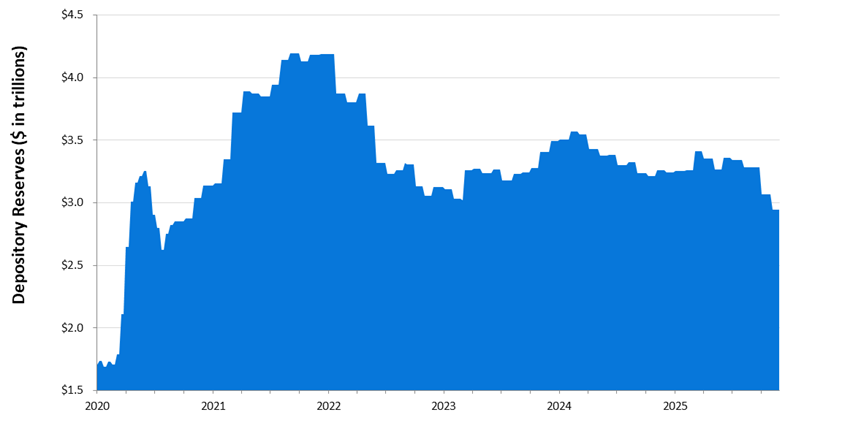

Bank reserves have fallen off a cliff in recent months. They’re now below $3 trillion for the first time since late 2020.

Check it out…

This represents the lower bounds of what banks consider comfortable for day‑to‑day operations. Reserves give them liquidity in an emergency. So the lower that buffer is, the more careful they have to be with lending.

Put simply, when reserves dip too far, banks will pull back from lending.

The Fed seems to realize what’s going on. It announced in late October last year that it would end QT as of December 1.

Officially, the move was described as a “technical adjustment.” In reality, it’s a clear sign that the Fed wants to stimulate the economy.

The central bank reinvested its maturing investments and bought $40 billion in short‑term Treasurys in December last year. Officials have been careful to avoid calling it QE. But the effect is the same.

Liquidity is easing. The Fed’s balance sheet is no longer shrinking. Soon enough, banks will be more comfortable lending again.

These changes won’t happen overnight. Investors will have to exercise patience. But it’s another positive sign for credit. Bank lending standards may even loosen up within the first two quarters of 2026.

The broader backdrop remains supportive. Earnings growth is solid. Valuations are reasonable. Investor sentiment has cooled from earlier extremes.

And now, liquidity is no longer shrinking beneath the surface. This is just what the economy needs to keep powering forward.

The Fed isn’t ready to start throwing around the term QE. But its actions speak clearly. There’s a floor under liquidity and we’ve reached it. The system has to stop tightening.

There’s no guarantee that it’ll be smooth sailing ahead. But things look a lot better in the next phase of the economic cycle.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research