The market has yet to buy into this retail giant’s promised turnaround

After generating record returns in 2022, retail giant Target (TGT) experienced 12 consecutive quarters of weak or falling sales.

The company built its identity as a go-to retailer for stylish and affordable products. However, it has lost some of its magic due to a combination of inflation, operational shortcomings, and increased competition.

Amid this slump, the company turned to Michael Fiddleke, a 20-year company stalwart and tapped him to be its next CEO.

While Fiddelke has continued to reiterate his commitment to improve Target, investor skepticism on the company continues to remain high, indicating he still has a long way to go in convincing investors that he can successfully turn this stagnating retail giant around.

Investor Essentials Daily:

Friday News-based Update

Powered by Valens Research

A few months ago, we mentioned that retail giant Target (TGT) is pinning its turn around hopes on Michael Fiddelke, a 20-year company veteran upon the announcement of long-time CEO Brian Cornell’s departure.

Fiddelke’s appointment came amid Target’s yearslong slump, which has seen revenue fall from $109 billion in 2023 to $105 billion, after growing in each of the past six years.

This downwards slump has largely been attributed to a combination of inflation, operational shortcomings, and increased competition.

Rising inflation has shrunk spending power, leading many customers to become increasingly mindful of their purchases and cut back on non-essential spending. Meanwhile, shopper experience has declined due to the friction in operating locations as both in-person shopping centers and e-commerce hubs.

Its discontinuation of its price-matching policy and DEI initiatives further alienated customer groups as well.

Rivals Walmart (WMT) and TJX Companies (TJC)-owned TJ Maxx have also gained ground, taking away market share from Target.

In response to the company’s slumping performance, incoming CEO Fiddelke vowed to speed up turnaround efforts which include the improvement of shopping experience, product redesigns, and adoption of advanced tech tools inside the firm.

As part of this strategy, Target plans to spend around $5 billion next year to improve its stores, digital capabilities, and merchandise selection.

Last month, Target announced its plans to cut roughly 1,800 corporate roles as part of its turnaround strategy. The company also announced that it reduced prices on 3,000 everyday items earlier this month and offered trendy exclusives in anticipation of this year’s holiday season.

A partnership with OpenAI was announced earlier this week as well, which will allow users to browse and search Target products through an app in ChatGPT.

Despite Fiddelske’s pronouncements thus far, Target’s struggles continue, as it just reported its 12th consecutive quarter of weak or falling sales earlier this week.

During the third quarter of 2025, the company generated revenues of $25.27 billion, slightly below the consensus estimates of $25.32 billion. Meanwhile, net sales in the same quarter were 1.5% lower compared to last year.

Customers also made fewer visits to Target stores and its website, while simultaneously spending less time during those visits. Traffic dropped by roughly 2.2% and average transaction amount fell 0.5% year over year.

During Target’s third quarter earnings call, Fiddelke reiterated his commitment to turn the company around. And while this pronouncement affirms his commitment to fixing the business, it also shows the firm isn’t in great shape right now.

Investors still have doubts about Target’s turnaround plans. When Fiddelke was announced as the company last August, the company’s shares went down 6.3% and it hasn’t improved since. As of now, the company’s shares are down 37% year-to-date.

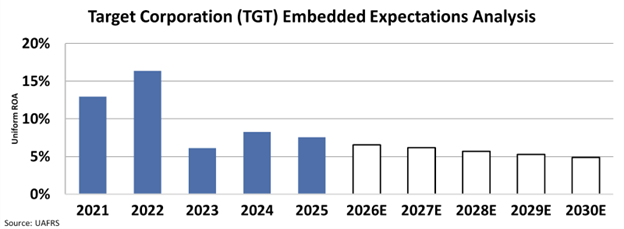

Skepticism around the company’s stock is still high. And we can see this through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At current valuations, investors expect Target’s Uniform return on assets (“ROA”) to go down from 7.6% this year to just 5% by 2030.

It’s clear Fiddelke is committed to turning Target’s business around, as he has shown willingness to streamline the company’s operations while simultaneously spending more to improve its shoppers’ overall experience.

Unfortunately, the company’s turnaround efforts will take time to materialize, especially as it struggles to convince cash-strapped customers to spend more.

Fiddelske still has a long way to go in convincing the market that he can fix Target. Until then, investor skepticism will remain high.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research