The oilfield services provider ProPetro is an interesting name to watch as energy prices make headlines

Over the past year, supply chain disruptions and labor shortages have left producers unable to meet resurgent demand coming out of the pandemic, placing strains on global markets and driving higher inflation.

Nowhere has this been more clear than in the energy sector, where supply and demand mismatches, along with constrained capacity and a lack of investment, have led oil prices to reach 5-year highs.

While higher crude prices typically translate into higher profitability for oil and gas companies, the looming transition to renewable energy has dramatically altered the landscape, leaving the future uncertain for many companies.

Yet, for one oil and gas services provider that helps producers with hydraulic fracturing, as-reported metrics fail to capture how profitable the business can be even with low oil prices.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

Oil prices have been rocketing higher over the past 12 months, as strong demand stemming from the global economic recovery pushes up against disrupted supply chains and constrained capacity.

With the Organization of the Petroleum Exporting Countries (“OPEC”) also constraining production levels, prices have now breached previous 5-year highs last seen in 2018, and are now approaching levels not seen since before the 2014 commodities crash.

While light crude prices on the New York Mercantile Exchange (“NYMEX”) are now comfortably in the $80 per barrel range, oil and gas companies haven’t been reacting like they normally have in the past, by ramping up production and investment in new capacity.

From exploration and production (“E&P”) companies that discover and drill for oil, like Exxon Mobil (XOM) and Royal Dutch Shell (RDS.A), or services companies that provide related equipment and expertise, such as Schlumberger (SLB) and Baker Hughes (BKR), most have remained under pressure by shareholders to maintain steady operations and return capital in the form of dividends and share buybacks.

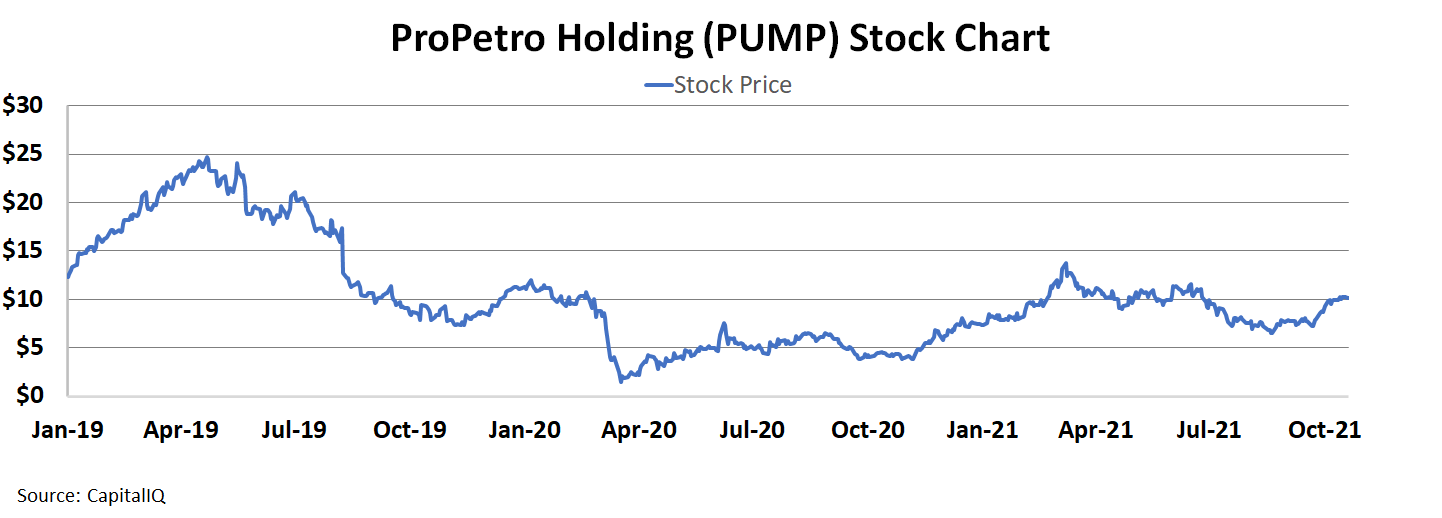

For smaller players such as ProPetro Holding (PUMP), which makes hydraulic fracturing (“fracking”) systems for upstream oil and gas producers, the situation has been similar. Despite surging oil prices, the company’s stock price has actually fallen since this past March.

See for yourself below.

Part of the reason why ProPetro’s shares have been down appears to be a misunderstanding by the market of how good of an oilfield services company it really is.

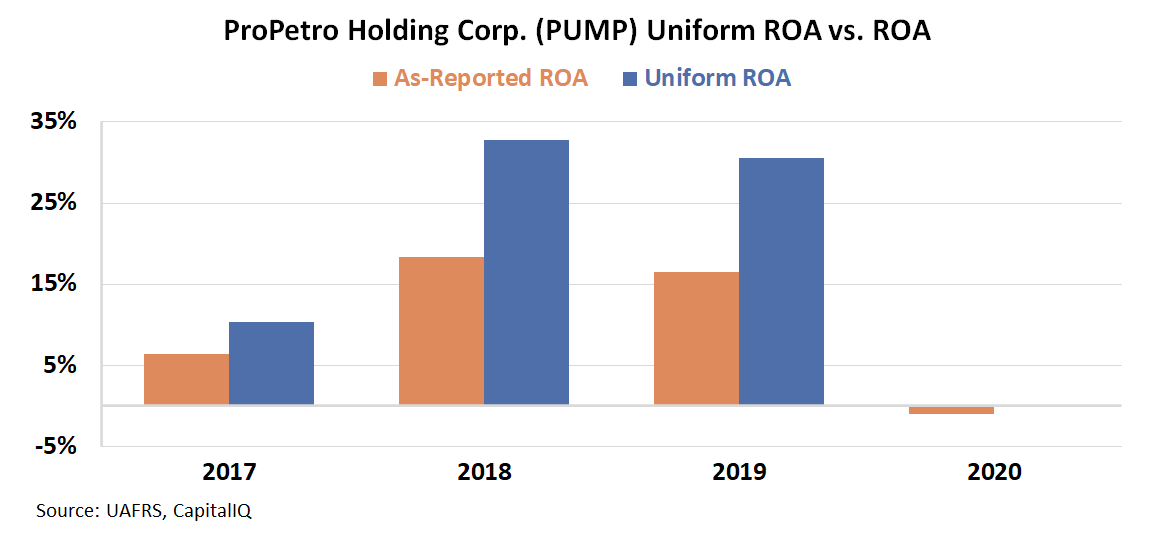

On an as-reported basis, ProPetro’s return on assets (“ROA”) hovered around 15% levels prior to the pandemic, slightly above corporate averages in the U.S. and much higher than peers in the oil and gas equipment and services sector, notably the big three of Schlumberger, Halliburton (HAL), and Baker Hughes.

Yet, with the energy business a difficult one to begin with, especially due to increasing pressure over climate change, only slightly above average returns aren’t nearly enough to excite investors in the space.

It’s only when we take a closer look with Uniform Accounting that we can see ProPetro’s Uniform ROA was actually double what as-reported metrics suggest, sitting at 31% in 2019, potentially providing investors with plenty to be excited about.

ProPetro’s impressive performance prior to the pandemic highlights that even in a lower oil price environment, which we saw in 2019 into 2020, the company was creating value for investors.

With oil prices now surging on the back of strong macroeconomic tailwinds, ProPetro may generate even better returns going forward, contrary to what as-reported metrics might lead investors to believe.

SUMMARY and ProPetro Holding Corp. Tearsheet

As the Uniform Accounting tearsheet for ProPetro (PUMP:USA) highlights, the Uniform P/E trades at 80.3x, which is above the global corporate average of 24.3x and its historical P/E of -236.3x.

High P/Es imply high EPS growth going forward. In the case of ProPetro, the company has recently shown a 101% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, ProPetro’s Wall Street analyst-driven forecast is a 696% EPS growth in 2021 and a 240% EPS decline in 2022.

Furthermore, ProPetro’s earning power in 2020 is below the long-run corporate average. That said, cash flows and cash on hand are at 200% of total obligations—including debt maturities and capex maintenance. All in all, this signals a low credit risk.

To conclude, the company’s Uniform earnings growth is above its peer averages, and the company is also above its average peer valuations.

Best Regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research