The quick-service market may be highly competitive, but this multinational firm can warrant a reevaluation of its stock

The quick-service restaurant industry is a highly competitive yet lucrative industry, generating $509 billion in sales last year.

However, over the past few years, this segment has had to deal with volatile conditions that brought about price inflation and changing customer tastes. As a result, margins have compressed and the pressure to remain profitable has intensified.

Despite this, Restaurant Brands (QSR), continues to perform steadily.

The Canada-based, quick-service restaurant firm is known for being the company behind Burger King, Tim Hortons, and Popeyes.

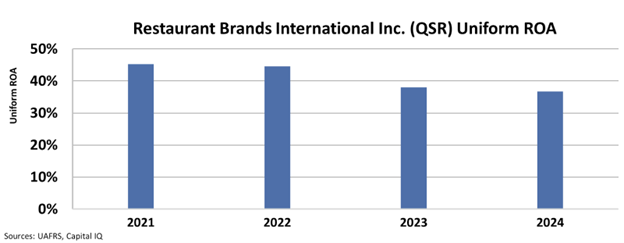

Restaurant Brands has steadily increased its revenues from $7.2 billion in 2021 to $11.52 billion last year. Likewise, its returns have remained above 35% during the same period.

However, despite generating a Uniform ROA of 37% and a Uniform asset growth of 16% last year, the company trades at a Uniform P/E of just 16.3x, well below corporate averages.

Investor Essentials Daily:

Tuesday News-based Update

Powered by Valens Research

The quick-service restaurant industry is one of the most highly competitive and lucrative segments in the food & beverage space, generating $509 billion in sales in 2024.

However, over the past few years, these firms have had to contend with a rapidly-evolving and highly-volatile business landscape. Not only are customers becoming more health conscious, they’re also changing their eating habits due to price inflation.

GLP-1 drugs and a renewed focus on health have led consumers towards healthier eating habits and food alternatives. Meanwhile, a combination of price inflation and growing consumer pressure has weighed on restaurant demand.

Based on Economic Research Service (“ERS”) forecasts, food-away-from-home prices are predicted to increase by nearly 4% this year.

Aside from those trends, tariffs, high ingredient costs, and surging labor costs are eating into already razor-thin margins for most restaurants.

Yet despite this volatile environment, Restaurant Brands (QSR), continues to perform steadily.

Headquartered in Canada, Restaurant Brands is one of the largest operators of quick-service restaurants, lagging behind just McDonald’s (MCD), Starbucks (SBUX), and Subway in terms of locations.

The company was formed in 2014 following the $12.5 billion merger of American chain Burger King and Canadian coffee brand Tim Hortons. In 2017, the company added Popeyes to its portfolio, before acquiring Firehouse subs in 2021.

Thanks to the company’s popular brands and fast-food’s robustness compared to traditional restaurants, Restaurants Brands has achieved stable profitability in recent years despite the headwinds facing its industry.

Since 2021, the company has grown its revenues from $7.2 billion to $11.52 billion last year. Meanwhile, the firm’s Uniform return on assets (“ROA”) has remained above 35%, with the company earning 37% returns in 2024 while generating a Uniform asset growth of 16%.

Yet despite its steady performance, the company trades at a Uniform P/E of just 16.3x, below corporate averages.

This valuation signals that the market remains cautious about the trends affecting and the competition that’s happening in the quick-service industry. However, the company has demonstrated its ability to weather intense competition and steadily generate above average returns over the long-term.

If Restaurant Brands can maintain its consistent profitability, its stock could warrant a reevaluation and provide upside to investors.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research