The recent semiconductor squeeze may catapult this firm into the spotlight

With recent shortages of semiconductor chips, a plethora of companies from Samsung to Toyota have spoken out regarding supply chain issues.

With this scarcity, this firm has the potential to make the design and production of chips more efficient than ever before.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

While the news has focused on the trade implications of the Evergreen ship Ever Given stuck in the Suez canal, there is another trade bottleneck brewing. The world has a serious shortage of semiconductor chips, particularly for auto chips and other end markets.

These issues have been prevalent for all participants in the industry, both large and small. Samsung has even spoken out regarding the concerns about the chip scarcity.

Many industry experts believe individual fabricators should be rapidly ramping up chip capacity to match demand.

There are alternative solutions, though.

Another option is for fabricators to expand operations, manufacturing chips for different end markets. By creating a more diversified business, fabricators are less exposed to demand shocks and the risk of shortage is alleviated.

That being said, these companies do not have to make a wide array of chips to fulfill demand. If a manufacturer can design a more efficient way of making chips, this would also help with the scarcity issue.

Completely redesigning an assembly line or iterating on a new wafer design requires a robust, industrial grade software platform for engineers to collaborate within.

Synopsys (SNPS) works with software products and consulting services in the design automation industry to fulfill these needs and more for the market.

The reason Synopsys is relevant in the semiconductor chip discussion is because one of their main operating segments is the semiconductor and system design space.

Although the firm offers solutions that might enable more efficient solutions for chip design and production, it would appear customers don’t see a value in this niche but important service.

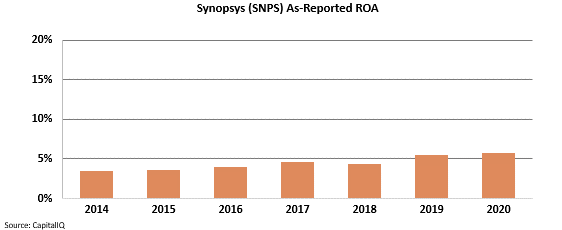

Specifically, the as-reported metrics for Synopsys highlight weak returns. ROA levels have only expanded from 3% in 2014 to 6% in 2020.

Synopsys has failed to get close to U.S. corporate averages near 12%.

See for yourself below.

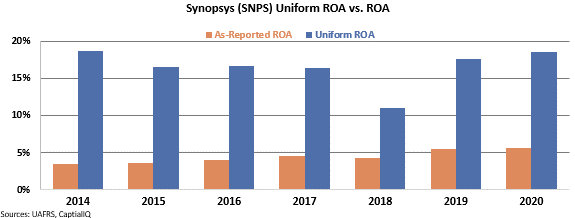

In reality though, this is not an accurate picture of Synopsys’ performance. The firm does have higher than average returns.

Specifically, the firm has been able to sustain 11% over the past seven years. After fading from 17% in 2014 to 11% in 2017, Uniform ROA quickly recovered to 19% in 2020.

When looking through a Uniform Accounting lens, it becomes clear the firm’s business model is efficient.

Clearly, customers are willing to pay a premium for Synopsys’ products. The company’s valuable technology is important for chip manufacturers looking to innovate and ramp up production during this hot time for the market.

SUMMARY and Synopsys, Inc. Tearsheet

As the Uniform Accounting tearsheet for Synopsys, Inc. (SNPS:USA) highlights, the Uniform P/E trades at 33.9x, which is above the global corporate average of 23.5x and its own historical average of 23.9x.

High P/Es require high EPS growth to sustain them. That said, in the case of Synopsys, the company has recently shown a 27% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Synopsys’ Wall Street analyst-driven forecast is a 40% and 5% EPS growth in 2020 and 2021, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Synopsys’ $236.4 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 20% per year over the next three years. What Wall Street analysts expect for Synopsys’ earnings growth is above what the current stock market valuation requires in 2020, but below its requirement in 2021.

Furthermore, the company’s earning power is 3x the long-run corporate average. Also, intrinsic credit risk is 20bps above the risk-free rate and cash flows and cash on hand are consistently exceeding its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a low credit risk.

To conclude, Synopsys’ Uniform earnings growth is above its peer averages, but the company is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research