The restless billionaire is active again…do his actions lead to profits?

Carl Icahn is best known for his activist investing endeavors. Across Wall Street, he is notorious for forcing change within his portfolio companies.

Recently, he has been in the headlines again, not only for his pursuit to change McDonald’s (MCD), but for a documentary released about his life by HBO. Those who know his life or have seen the documentary may know his strategy with McDonald’s is different.

To better understand his strategy and whether he has set his portfolio up for success, let’s use Uniform Accounting to analyze his largest holdings and answer a simple question—are the companies currently well poised for future upside?

Also below, a detailed Uniform Accounting tearsheet of the fund’s largest holdings.

Investor Essentials Daily:

Friday Uniform Portfolio Analytics

Powered by Valens Research

One of the most prominent activist investors of the past forty years has been Carl Icahn. He earned the reputation of being cutthroat and often antagonizing towards the executives at companies he takes over.

Recently, HBO released Icahn: The Restless Billionaire, a documentary that has earned rave reviews from critics and industry insiders alike for exploring the activist veteran’s sometimes abrasive strategy, along with some of his biggest wins.

In exploring some of the biggest stances he has undertaken in his time on Wall Street, they note he is not done working on instigating change just yet.

In just the past month, he has been back in the headlines for another cause. This time, Icahn has launched a campaign against McDonald’s (MCD) to change the way the company buys pork.

Icahn is pushing McDonald’s to require all of its U.S.-based pork suppliers to abandon the practice of keeping pigs confined in gestation crates that are so small that the pigs can’t move around.

In 2012, Icahn forced McDonald’s to commit to phasing these crates out by 2022, but the company recently announced it was delaying the complete phase out until 2024.

Unlike Icahn’s normal activist campaigns, this one isn’t being accomplished by force. Instead of taking a major stake in McDonald’s, he only owns about 200 shares worth $50,000. Animal welfare is a passion project for Icahn, but his portfolio still contains many other firms where his priorities are profit.

As Carl Icahn takes his latest stand, now is a good opportunity to review the rest of his portfolio. To do so, let’s examine this fund through our Uniform Accounting lens.

Economic productivity is massively misunderstood on Wall Street. This is reflected by the 130+ distortions in the Generally Accepted Accounting Principles (GAAP) that make as-reported results poor representations of real economic productivity.

These distortions include the poor capitalization of R&D, the use of goodwill and intangibles to inflate a company’s asset base, a poor understanding of one-off expense line items, as well as flawed acquisition accounting.

It is no surprise that once many of these distortions are accounted for, it becomes apparent which companies are in reality robustly profitable and which may not be as strong of an investment.

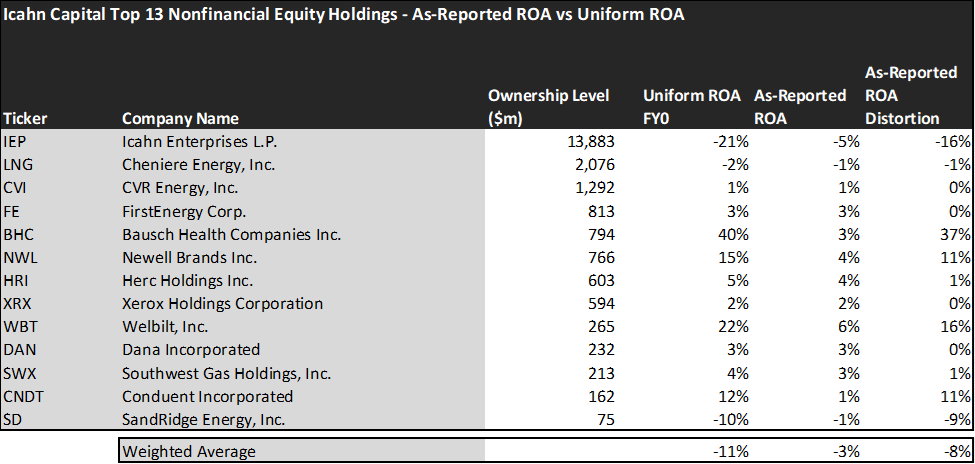

Contrary to what one might expect with the tech boom of the past decade, many of Icahn’s largest holdings remain in the industrial’s sector.

In particular, nearly 58% of the fund’s holdings are in his own industrial business Icahn Enterprises (IEP).

The average as-reported ROA among Icahn’s top 13 names is a miniscule -3%, which doesn’t even beat the average cost of capital in the market. In reality, though, these companies perform even worse, with a -11% Uniform ROA.

The fund’s namesake industrials business Icahn Enterprises, for example, doesn’t return -5%. It actually provides drastically poorer returns, at a -21% Uniform ROA. As an activist, Icahn oftentimes invests in turnarounds when they are inexpensive to unlock future value.

However, some of his other investments are much stronger than they appear. For example, Bausch Health Companies (BHC) does not have 3% returns. Rather, as a company with a strong position, it has a 40% Uniform ROA.

Largely, once we account for Uniform Accounting adjustments, we can see that many of these companies are mispriced investments that Icahn is hoping to turn around and unlock value.

These dislocations demonstrate that most of these firms are in a different financial position than GAAP may make their books appear. But there is another crucial step in the search for alpha. Investors need to also find companies that are performing better than their valuations imply.

Valens has built a systematic process called Embedded Expectations Analysis to help investors get a sense of the future performance already baked into a company’s current stock price. Take a look:

This chart shows four interesting data points:

- The Uniform ROA FY0 represents the company’s current return on assets, which is a crucial benchmark for contextualizing expectations. While the average Uniform ROA this year is surprisingly low, as we mentioned, Icahn tends to invest in asset-intensive turnarounds, so this isn’t as surprising.

- The analyst-expected Uniform ROA represents what ROA is forecasted to do over the next two years. To get the ROA value, we take consensus Wall Street estimates and we convert them to the Uniform Accounting framework.

- The market-implied Uniform ROA is what the market thinks Uniform ROA is going to be in the three years following the analyst expectations, which for most companies here is 2023, 2024, and 2025. Here, we show the sort of economic productivity a company needs to achieve to justify its current stock price.

- The Uniform P/E is our measure of how expensive a company is relative to its Uniform earnings. For reference, average Uniform P/E across the investing universe is roughly 24x.

Embedded Expectations Analysis of Icahn paints a clear picture of the fund. The stocks it tracks are cheaper than market expectations as they are ready for a turnaround.

The fund has analysts expecting average ROA to increase from -11% to 18%, the market is only pricing these companies to grow their economic profitability to 11%.

Icahn’s namesake company Icahn Enterprises may be able to outperform market expectations of earning 11% returns by reaching analyst expectations of 21%.

On the other hand, companies like SandRidge Energy (SD) might end up in a situation where investors may find themselves disappointed in the returns they end up achieving. With the market pricing in expectations of 6%, falling to analyst expectations of -27% would mean significant downside.

This just goes to show the importance of valuation in the investing process. Finding a strong industry is only half of the process. The other, just as important part, is attaching reasonable valuations to the companies and understanding which are the most fundamentally sound investments.

To see a list of companies that have great performance and stability also at attractive valuations, the Valens Conviction Long Idea List is the place to look. The conviction list is powered by the Valens database, which offers access to full Uniform Accounting metrics for thousands of companies.

Click here to get access.

Read on to see a detailed tearsheet of the largest holding in Icahn Enterprises.

SUMMARY and Cheniere Energy, Inc. Tearsheet

As Icahn Enterprises’ largest individual stock holdings, we’re highlighting Cheniere Energy, Inc.’s (LNG:USA) tearsheet today.

As the Uniform Accounting tearsheet for Cheniere Energy, Inc. highlights, its Uniform P/E trades at 16.1x, which is below the global corporate average of 24.0x, but above its historical average of -15.2x.

Low P/Es require low EPS growth to sustain them. In the case of Cheniere Energy, the company has recently shown a Uniform EPS decline of 1,820%.

Wall Street analysts provide stock and valuation recommendations that, in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Cheniere Energy’s Wall Street analyst-driven forecast is for EPS to decline 191% and 15% in 2022 and 2023, respectively.

Meanwhile, the company’s earning power is below the long-run corporate averages and, cash flows and cash on hand are below total obligations—including debt maturities and capex maintenance. Moreover, Cheniere Energy is 110bps above the risk-free rate. Together, these signal moderate dividend and credit risks.

Lastly, Cheniere Energy’s Uniform earnings growth is below its peer averages, but is trading in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research