The unspoken truth of investing in real estate

The real estate market has been blown open by the pandemic, with little sign of slowing down in 2021. Climbing real estate prices in a recession are unique, and it impacts spending in other related industries.

We have often referred to this market shaking event as the “At-Home Revolution,” and have stressed these shifts in spending aren’t going to end with the pandemic. We will discuss how this should shift your asset allocation strategy, if at all.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

The pandemic has thrown seasonal demand out the window. Traditional market “hot-spots” have been passed over for new ground.

Traditionally, the homes near large cities by the coast see the most prominent price increases. However, in 2020 small metropolitan markets like Pittsburgh, Cleveland, and other city suburbs are seeing the biggest gains.

Millennials have been late to homeownership compared to previous generations. This has had far reaching effects, such as reduced spending around cars, the decline of suburbs, and even lower government revenues from real estate taxes.

Now, the pandemic has forced the hand of many millennials to buy, causing home prices to surge.

Record low mortgage rates accelerated home buying for many, as rates plummeted after Fed action. Price increases have already canceled out any benefit for consumers, and prices are still going up.

Normal seasonality in the housing market dictates sales are heaviest in the summer, when parents can get kids into the school system before the next year starts.

The rise in home prices never slowed down through this winter, and with summer approaching once again, it’s unlikely this trend will change. As this CNBC article highlights, prices rose by 8.4% across the nation year-over-year in October. This is the largest month to month move in over a decade.

As of the most recent data released by FRED, home prices rose by almost 10% from February 2020 to the end of the year.

With the “At-Home Revolution” in full swing, rising home prices and red-hot demand will be a feature of housing for many more months to come.

Those who are looking to invest in real estate have a lot to think about today.

There is a booming market, and long-term tailwinds for the move away from cities to suburbs and rural areas. Folks are looking for more space, and remote working is increasingly accepted across large companies across America.

As the benefits of living in a city fade, some investors may be thinking a smart investment would be homes in areas that people would want to be buying in. However, the math doesn’t check out on buying real estate as an investment.

To clarify, we are not talking about buying the home your family will live in. This also doesn’t cover buying a vacation property now that folks can work remotely, nor an upgrade to a different part of the country.

Whether or not people should rent or buy a home they plan on living in or using regularly is a separate discussion and revolves around how long the home will be lived in, whether they want to make any changes, and more.

When we say buying a home as an investment, we are strictly referring to buying a home as a “passive” investment that the investor plans to rent out as a source of income.

Many bloggers and pundits love to talk to the benefits of passive home investment like it is a no-brainer, but the reality of managing such an investment is hard work. There is a real cost in time and money which makes “passive” real estate investing into more of a career.

The landlord needs to worry about finding and keeping high quality tenants who will not damage the property. They need to build a network of relationships with service providers who can repair the inevitable wear and tear on the house.

If an investor doesn’t want to spend a significant amount of time dealing with these headaches, they can hire a real estate manager, but this would eat directly into any rental income.

Even if an investor didn’t have to worry about any of these things, the economics simply don’t make sense.

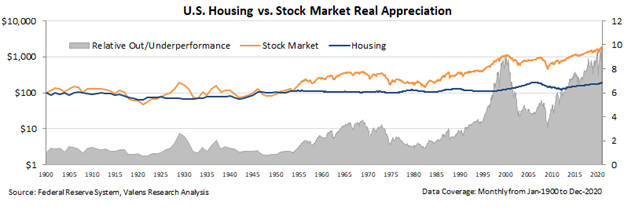

As we mentioned, this was a banner year for home prices and demand. From February to December, home prices were up almost 10%! However, there was another truly passive investment up almost three times that amount, at 26% in the same period.

Just buying the S&P 500.

Even in one of the best times for home appreciation in the past twenty years, an investor who spent only a few minutes to buy into an S&P 500 index outperformed real estate.

This has applied historically as well. If an investor were to invest $100 into the U.S. housing market in 1900, they would have $189.57, adjusted for inflation. If that same investor had invested in the stock market, they would have $1,866.84… a return almost ten times higher.

Buying the S&P doesn’t concentrate risk like home ownership does, any active participation which eats into returns, or any market knowledge to get right.

Leverage doesn’t help home ownership’s case either. Even assuming 80% leverage on a home, the return would be around 45%, minus the cost to borrow.

Meanwhile, with just 1x margin on the S&P 500, the return would be a little less than 52%, with a lot less leverage than the same home investment. Again, this would come at a lot less effort, and a lot more diversification, as the investment would be spread across 500 well performing companies.

This is not to be anti-home ownership, or to say people should only be renting. Homeownership can be a rewarding endeavor for those looking to switch from renting to buying.

For investors looking at passive real estate as the place to park their money, it’s important to measure these options against the tried-and-true investment into the best companies in the world.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research