There are more opportunities from digital payments than you might realize

As the West catches up to places like China in the area of digital payments, cash is becoming less and less common as a form of paying for everyday items.

With innovative technologies like QR codes and digital wallets, whose adoption has been supercharged due to the pandemic and the need to limit face-to-face interaction, it is only logical to believe companies stuck in the cash economy will be left behind.

Yet, for one firm making the transition to the cashless economy, as-reported metrics fail to show how profitable the digital payments space truly is.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

Today, with the proliferation of credit and debit cards and easy-to-use instant payment apps provided by digital payments companies like Square (SQ) and services such as PayPal (PYPL)’s Venmo, many people often speak of the “death of cash.”

Lugging around large bills means losing your ability to pay for anything if you lose your wallet or something worse happens. Digital transfers and card payments make life much easier for consumers, not only from a security standpoint but also from a convenience perspective as well.

Unlike in the past, a wallet filled with cash can now be replaced by a digital wallet or app on your smartphone, which can be used to make a wide array of payments at a growing number of locations.

For the more tech savvy, this means the days of stopping by the local bank branch to use an ATM are largely over, as the click of a button on a computer or smartphone can fulfill essentially the same need.

Logically, this secular decline in the use of cash should lead to a declining use of ATMs.

Taking this thought process further, a decline in use of ATMs should also hurt companies like Euronet Worldwide (EEFT), which runs 37,000 ATMs and hundreds of thousands of point-of-sale (“POS”) terminals for financial institutions, retailers, and merchants around the world.

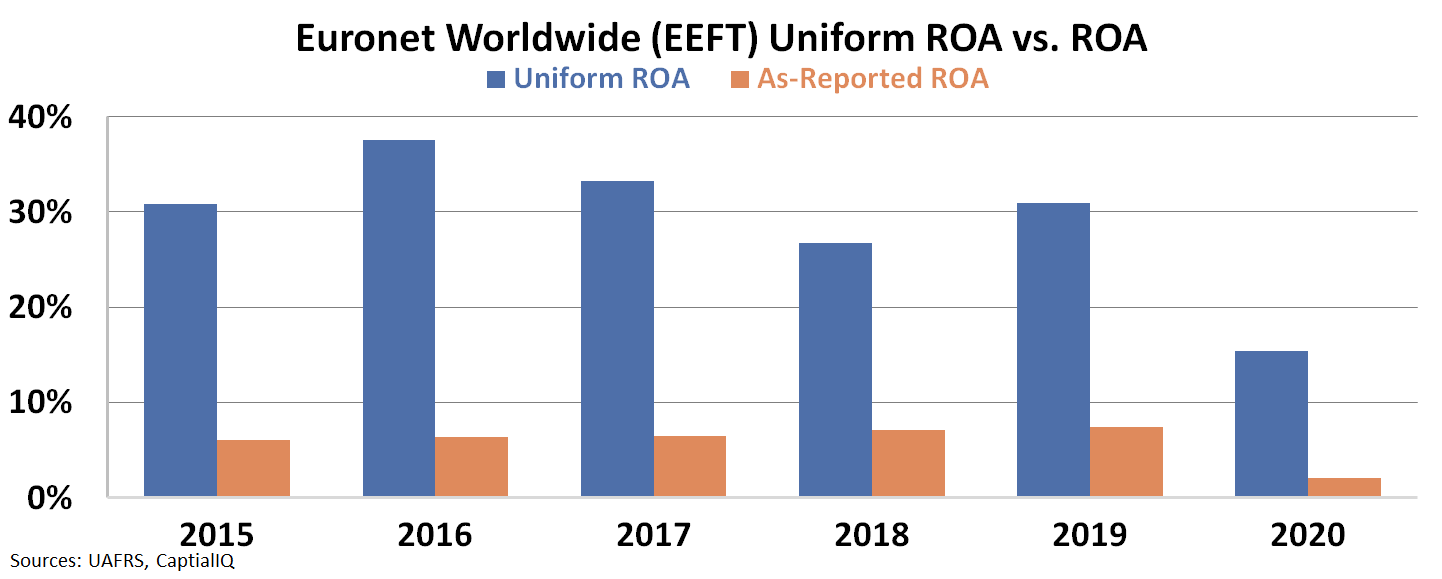

Looking at as-reported metrics, this thesis seems to be vindicated, with Euronet appearing to be a struggling business with its heavy focus on ATMs.

In fact, over the past five years return on assets (“ROA”) have been stuck in the mid-single digits range at around 6%-7%, before the pandemic led to a bruising collapse to 2% in 2020.

See for yourself below…

In reality however, Euronet is much more than the dying ATM provider as-reported metrics make it out to be.

The company has actually been doing a great job shifting away from cash towards digital payments, exemplified by both its ePay and money transfer businesses, which includes direct peer-to-peer transfer functionality.

These focus areas are the most profitable areas of the business, and have been for a while now. Given this exposure to the digital payments space, we would expect ROA to be significantly higher than the corporate average of 12% levels as-reported metrics suggest.

On a Uniform Accounting basis, these suspicions turn out to be correct, as Uniform ROA has been consistently much higher than as-reported ROA, reaching a peak of 38% in 2016 and declining only to 15% in 2020, not 2%.

As it turns out, Euronet has been fully aware of the coming “death of cash” and what it means for its business for quite a while.

The moves it has taken in the digital payments space demonstrate not only the strength and adaptability of its business model, but also just how well-run a company it really is.

Relying on as-reported metrics, investors would be led to believe Euronet is a zombie company destroying economic value by operating below its own cost of capital. In reality, just the opposite is true.

SUMMARY and Euronet Worldwide, Inc. Tearsheet

As the Uniform Accounting tearsheet for Euronet Worldwide, Inc. (EEFT:USA) highlights, the Uniform P/E trades at 23.6x, which is around the global corporate average of 21.9x but below its historical average of 32.7x.

Market average P/Es require moderate EPS growth to sustain them. That said, in the case of Euronet, the company has recently shown a 64% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Euronet’s Wall Street analyst-driven forecast is an EPS growth of 25% and 105% in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Euronet’s $131 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 9% annually over the next three years. What Wall Street analysts expect for Euronet’s earnings growth is above what the current stock market valuation requires through 2022.

Furthermore, Euronet’s earning power is 3x the corporate average. Also, cash flows and cash on hand are almost 5x above its total obligations—including debt maturities and capex maintenance. This signals a low credit risk.

To conclude, Euronet’s Uniform earnings growth is above its peer averages but the company is trading below average peer valuations.

Best Regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research