There’s a downside to today’s “IPO mania”

2026 is a banner year for IPOs. SpaceX (SPCX), which recently went public, has the honor of being the largest IPO of all time after raising $75 billion.

So far, the market has seen sixty prominent IPOs this year raise nearly $40 billion (before the SpaceX IPO), which is the strongest first half since 2021.

While this makes for an interesting backdrop to a market that has continued to shrink for 23 years, it’s precisely the same reason that’s giving anxiety to some investors.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

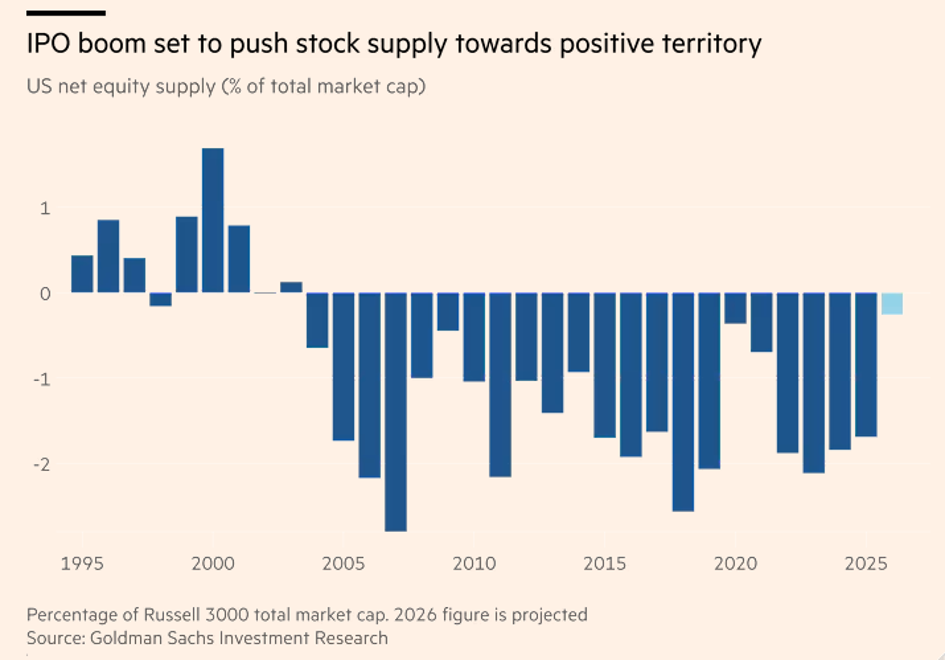

A flood of new shares is hitting Wall Street in 2026.

The SpaceX (SPCX) IPO was arguably the biggest-ever event on Wall Street. It’s the largest initial public offering of all time after it raised $75 billion for the company, but it’s not alone.

OpenAI and Anthropic are expected to follow as soon as this year, giving investors a rare shot at owning some of the most important AI companies on the planet.

That makes 2026 an exciting year for the markets, but it also makes some investors anxious.

The last time the market had this much fresh equity to digest, the dot-com bubble was near its peak.

Since then, and for 23 years, the market has been shrinking.

When measured, the net equity supply in the U.S., or the supply of new shares from IPOs minus buybacks and companies going private, the supply has been shrinking every year since 2003.

However, this year may be on pace to buck that trend.

Goldman Sachs expects U.S. net equity supply to be roughly flat in 2026. It also expects a bigger wave of supply in 2027 because this year’s IPO lockups will expire and more shares become available for trading.

Chart from FT

The IPO market is already heating up. So far, the market has seen sixty prominent IPOs this year raise nearly $40 billion (before the SpaceX IPO), which is the strongest first half since 2021.

Goldman estimates it could reach a record $225 billion thanks to this year’s flagship offerings.

And that doesn’t even include money from already-public companies, like Alphabet’s (GOOGL) $85 billion offering, or the similar sales being discussed by Meta (META) and Oracle (ORCL).

Investors have a few concerns about this trend. For example, some investors are worried that the shrinking share count has been a quiet tailwind for stocks for over two decades. If demand stays the same and the supply of stocks shrinks, prices should rise naturally.

Plus, there’s the fear that investors will get fatigued. New shares need buyers, and if investors want SpaceX, OpenAI, or Anthropic, they may need to sell existing holdings to make room.

Richard Bernstein of Janus Henderson (JHG) put the fear plainly. He said record new issuance is a classic sign of a bubble, and that the three biggest IPOs will raise more money than all IPOs during the 1999 to 2000 tech bubble, even after adjusting for inflation.

However, that argument is missing the point.

Companies are issuing stock because AI requires enormous lumps of cash. Data centers and all the equipment needed to stock and power them are going to cost big tech companies hundreds of billions of dollars per year.

For much of the past two decades, major companies had more cash than productive places to spend it. Buybacks were the natural answer. That’s no longer the case.

That backdrop means this IPO wave will test investor appetite. If demand weakens, future IPOs could perform worse than SpaceX’s did. If lockup expirations swamp the market next year, recent buyers might feel pressure to sell.

Right now, the bigger story is infrastructure spending. All of this money is being raised to build AI data centers, not to pay dividends or buy back shares.

That makes this year’s equity-supply flip less threatening than it looks. Equity isn’t scarce anymore, but it can still get more valuable as companies invest in future earnings growth.

Investors should expect bumps as the market absorbs these huge IPOs. And they should stay constructive as long as companies keep turning that cash into growth.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research