This beer maker’s stock may look cheap, but there’s more to its low valuation than meets the eye

Vice stocks like tobacco and alcohol have often been stable investments as these stocks are relatively shielded from adverse macroeconomic shifts, enabling them to generate stable and reliable returns over a long period of time.

Nicotine and alcohol are considered consumer staples due to their addictive qualities and cultural significance, which has buoyed their demand for decades.

However, consumer tastes and trends evolve over time, and some vices are losing their hold over the American consumer while others are gaining ground.

As we will see in the case of Molson Coors (TAP), low valuations aren’t always a sign that a stock is undervalued and has room to grow.

In some cases, low valuations stem from underlying issues that aren’t immediately visible on the surface.

Investor Essentials Daily:

Wednesday News-based Update

Powered by Valens Research

When people think about staples, household items such as canned goods, dairy products, diapers, and paper towels, typically come to mind.

However, nicotine products and alcoholic beverages are commonly also considered staples due to their addictive properties and foothold in society. Due to this, stocks in these industries are often seen as reliable by investors who seek stable growth and profitability over long periods of time.

Demand for nicotine and liquor are relatively inelastic, because while financial situations may change, consumers’ demand for these products generally does not waver.

That said, while these products are relatively insulated from economic swings, evolving consumer behaviors and tastes can impact vices.

Tobacco and cigarette use have long been linked to cancer and other adverse health conditions.

The tobacco industry’s growth has been limited for decades due to products’ links to cancer and numerous health risks for users, leading to stricter rules and regulations put in place to discourage consumption. As consumers have become more cognizant of the hazards of smoke-based tobacco, consumption has fallen to 11% of adults today.

In the face of a shrinking smoking population, nicotine companies have experimented with new forms of products, from e-cigarettes to smokeless tobacco products.

Nicotine pouches have emerged as the most popular smoke-free alternative. Unlike traditional smokeable products, these pouches contain nicotine powder and other flavorings, making them highly marketable to younger individuals and consumers who want to lessen or quit smoking entirely.

Industry players like on!, Velo, and Zyn, have flooded the market with their offerings in recent years.

Among these brands, Zyn—owned by Swedish Match, a company acquired by Philip Morris International (PM) in 2022 for $16 billion—has captured a significant share of the American nicotine pouch market, with shipment volumes increasing from 132 million during the first quarter of 2024 to 202 million in the first quarter of 2025.

In January of this year, U.S. health officials greenlit Zyn to continue selling its smoke-free products after discovering that these offerings pose a lower risk of serious health conditions than cigarettes.

Due to the emergence of smoke-free nicotine products, the substance is seeing renewed demand, leading to investor optimism for big tobacco companies like Philip Morris.

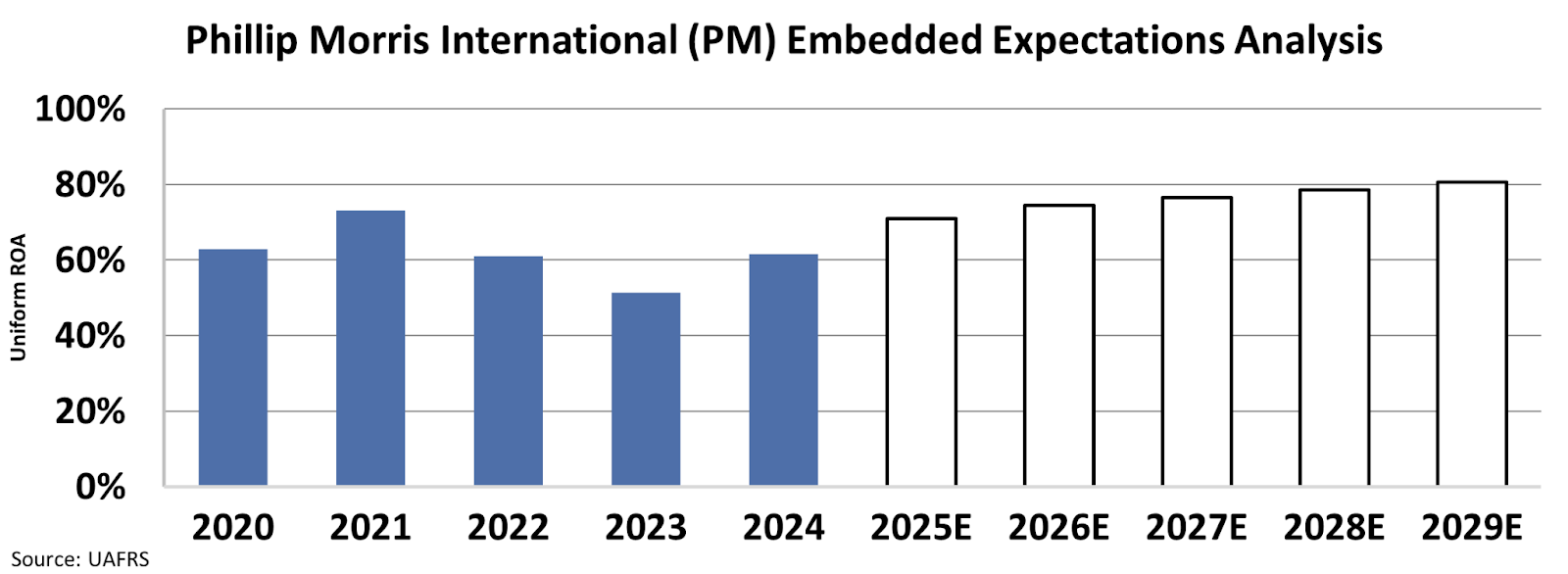

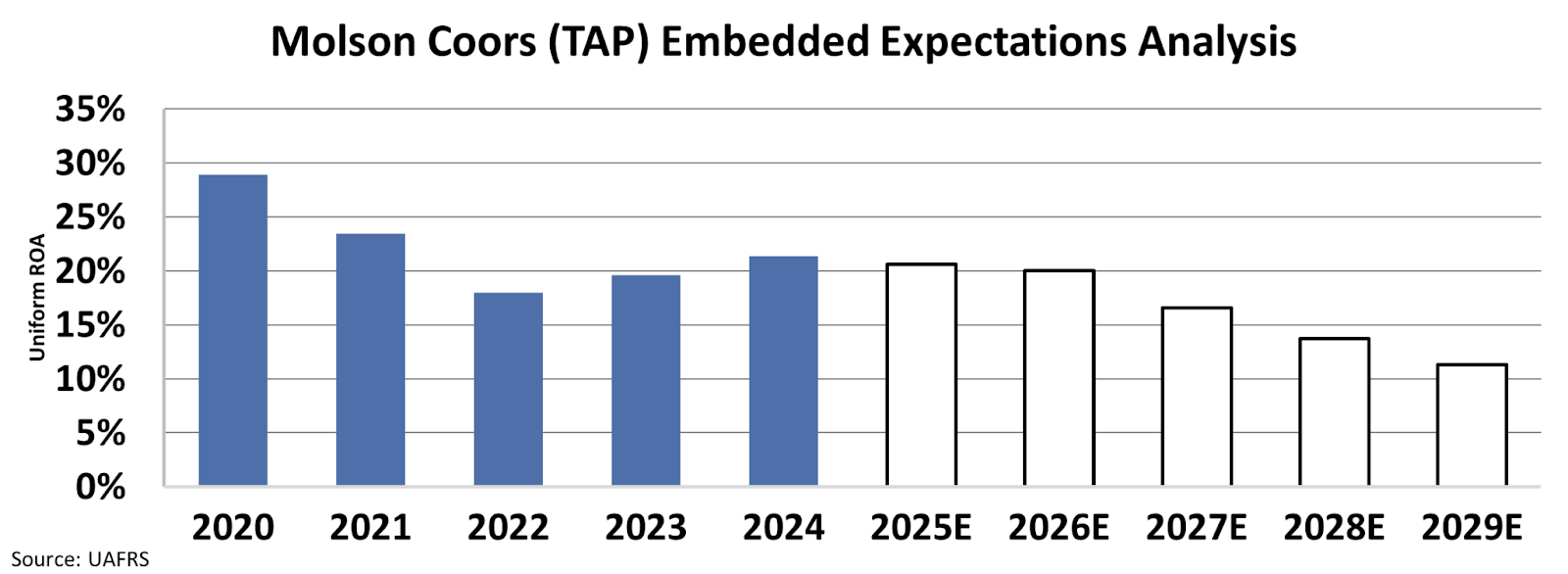

We can see what the market thinks through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At current stock prices, the market expects Philip Morris’Uniform return on assets (“ROA”) to reach 80% by 2029, a sharp rise from the 61% returns it delivered in 2024.

The market expects this level of return because Philip Morris—through its new smokeless products—has positioned itself to ride the wave of smoke-free nicotine.

While corners of the tobacco industry are in the midst of a resurgence, it seems parts of the alcohol industry are moving in the opposite direction.

Molson Coors (TAP) owns well-known brands such as Coors, Miller, and Blue Moon. Throughout the years, the company has established itself as one of the most popular beer brands in the U.S.

Beer has largely been considered one of the most popular vices and the most popular alcoholic beverage for decades. However as consumers become increasingly health-focused, alcohol, and beer specifically have been facing growing criticism from consumers.

Given recent studies articulating beer’s health risks and its own links to cancer, people have reconsidered this popular beverage, in fact around 56% of adults have recently reduced alcohol consumption due to health and lifestyle reasons.

Beer, which was once the favorite alcoholic beverage for 47% of U.S. drinkers, is now preferred by just 34% of consumers.

Changing consumer preferences has presented a challenge for Molson Coors, whose product portfolio revolves heavily around beer. And the market recognizes this threat.

At current valuations, the market expects Molson Coors’ Uniform ROA to decline to 11% by 2029, a steep drop from the 21% returns it generated in 2024.

With fewer people seeking alcoholic products, and Molson Coors’ limited portfolio outside of beer, the market’s cautionary stance towards the company seems justified.

Companies like Molson Coors are heavily reliant on consumer behavior that favors their products. With preferences shifting, there’s not much upside to this stock.

Although the company looks cheap on the surface, there’s a reason as to why valuations are on the decline.

Investors should be cautious when looking at this business. Oftentimes, a cheap stock is cheap for a reason.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research