This benefits management firm fulfills a crucial need

Family-building is a lot more complicated. Roughly 10% of American women have problems conceiving or staying pregnant.

To add to this, fertility care is complex and can often be expensive. That’s why professionals who seek to build a family look for employers that include fertility in their benefit package.

While employers who seek top talent are more than eager to oblige, they also want to minimize cost and complexity associated with this.

That’s where Progyny (PGNY) comes in. It is a benefits management company specializing in fertility, family-building and women’s health.

The company has generated strong returns in recent years. However, investors are expecting its returns to decline steeply in the coming years.

Investor Essentials Daily:

Tuesday News-based Update

Powered by Valens Research

Roughly 10% of American women experience complications related to pregnancy based on data from the U.S. Centers for Disease Control and Prevention.

This is a significant number and it indicates just how challenging it can be to start a family. To add to this, fertility care is expensive and complex.

That’s why career professionals who prioritize family-building are looking for employers who offer benefit programs. Meanwhile, employers who offer these programs want to manage the costs and complexity associated with it.

That’s where Progyny (PGNY) comes in.

Progyny is a benefits management company that specializes in fertility, family-building and women’s health. It helps members navigate a complicated health care journey while improving outcomes and lowering costs.

Progyny’s programs include, preconception, fertility, family planning, pregnancy, postpartum, parenting, child well-being, menopause, and midlife care.

The company doesn’t just work with employers and members. It also supports payers, health plan providers, consultants, labor unions, and individual payors.

Progyny currently serves over 600 clients as of 2026. Members are given access to over 1,000 fertility and women’s health specialists. The company also enjoys retention rates of nearly 100%, with expansion rates at over 30% for 2026.

The key to Progyny’s stickiness among its target client base lies in its ability to manage costs effectively.

Medical costs have risen 27% from 2022 to 2025. In the same period, Progyny’s costs have only risen 5%. Based on company estimates, around 30% savings has been generated by its clinical outcomes.

Aside from having a sticky business, the company doesn’t rely on a single massive client or industry to generate revenue. Its exposure is spread out in healthcare, labor, technology, financial services and insurance, telecom, and media and entertainment industries.

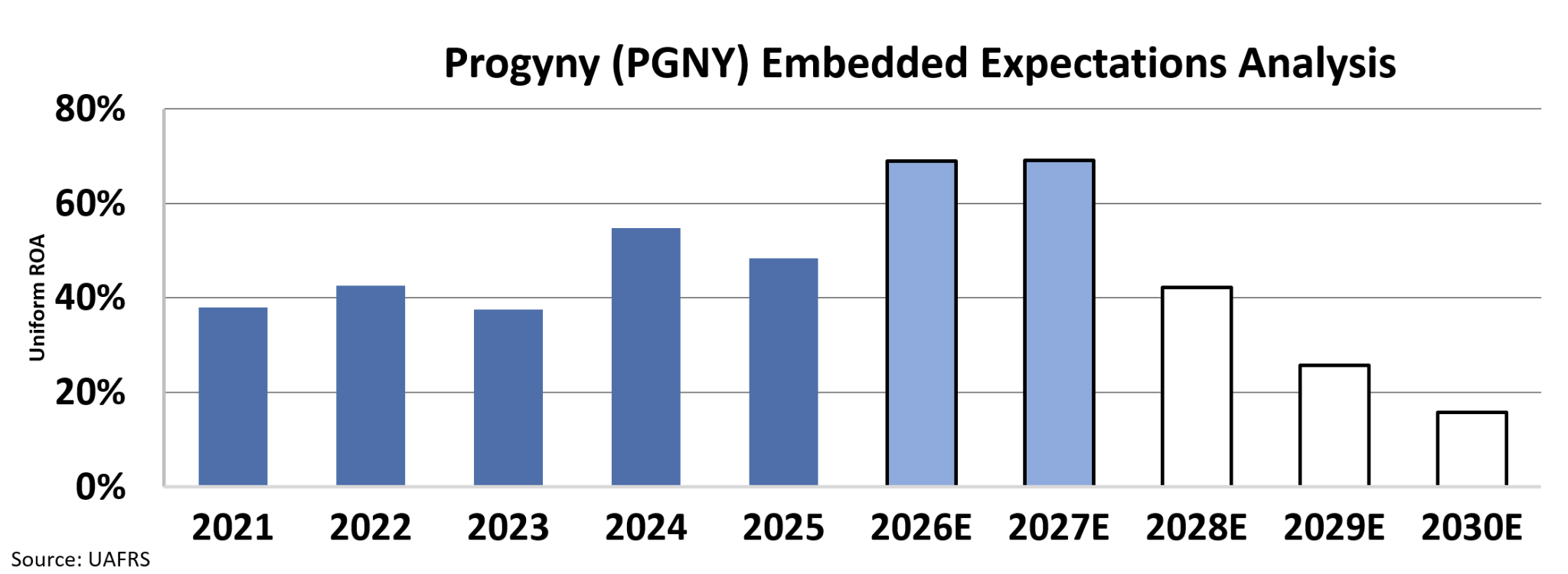

As a result, Progyny has enjoyed strong returns in recent years. Since 2021, its Uniform return on assets (“ROA”) have remained above 30%.

That doesn’t mean the firm hasn’t faced any bumps.

In 2024, Progyny announced it had lost Amazon (AMZN) as a client, with the engagement being terminated at the beginning of 2025. As a result, the company’s stock dropped as investors questioned whether it could maintain its growth.

That said, the business proved resilient even after losing a major client. In 2025, delivered a Uniform ROA of 48%, a slight decline from the 55% it posted in the year prior.

As mentioned above, Progyny has diversified its client base to over 600. And with its customers spread out across different industries, it has mitigated the effects of another Amazon-like event.

Progyny is also attempting to achieve higher growth through its Progyny Select offering. It is a fertility and women’s health program that’s designed to cater to employers with over 100 employees.

The company continues to be a strong performer. Aside from generating a Uniform ROA of nearly 50% last year, it also posted a Uniform asset growth of 26%.

That said, investor sentiment doesn’t reflect Progyny’s performance. It currently trades at a below-average Uniform P/E of 8x. This valuation also signals that investors are expecting returns to fall.

Wall Street analysts expect returns to continue climbing to nearly 70% in the next two years.

However, at current valuations, investors expect returns to drop to 16% by 2030, a steep decline from the 30%+ returns the company has delivered in recent years.

These growth assumptions are overly pessimistic. Progyny may have lost a key customer, but that doesn’t mean its core advantages have been eroded entirely.

The company boasts a diverse client base, high rate of expansion, strong retention levels, and lower costs.

If Progyny continues to maintain its core advantages, then it could outperform expectations and provide upside in the process.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research