This CEO went head-to-head with his former boss to win this industry, Uniform Accounting shows why investors have been excited he won

Sometimes leaders need to fail, or get “kicked out” of the roost, before they have true success.

Today’s company’s CEO was always viewed as a great leader, but it wasn’t until he created his own company, and ended up going head-to-head with his former boss, that he really took off.

As-reported metrics make his business not look like it is that successful, but TRUE UAFRS-based (Uniform) analysis shows that the firm has been able to produce impressive profitability and strong growth that justify the sky high valuations it has seen.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

After returning from his service as a Red Cross driver in France in 1919, Walt Disney sought to return to his childhood employer, the Kansas City Star.

As a child, he had worked as a paperboy and is still featured prominently on the Star’s website as a “Famous Employee.”

But when he applied as a cartoonist, he was turned down. Various accounts say different things, but the general idea was that the Star didn’t think he was “creative enough.” He then applied to be a clerk, and was turned down. Then a truck driver, again turned down. He wasn’t creative or employable enough beyond a teenage paperboy.

We all know how his career turned out.

100 years later the mammoth he created is worth nearly $200 billion. Disney+ is taking over streaming. The parks, although currently closed, are located all over the world.

A similar story played out years later. Oprah Winfrey was an evening news reporter in Baltimore, but eventually got fired. She was told she was “unfit for TV news.” She was offered a spot in a daytime TV show as consolation, and again, we all know the story from there.

Oprah’s show aired for 25 years, and she is now worth over $3 billion by some estimates.

There are plenty of articles out there that will list many other similar, inspirational stories. Sometimes, to find true success, one needs to fail at their original plan. Or in some cases, they just need to leave the proverbial roost.

Marc Benioff is one of the most recent examples of new scenery breeding success.

However, in his case, he was clearly good enough for his prior role. After starting at Oracle out of college, Benioff was quickly named Rookie of the Year, and by 26, was promoted to Vice President. He was the youngest person to hold that position at the time.

So, in 1999, when Benioff left Oracle in his mid-thirties to start Salesforce and build a customer relations management (CRM) platform, he was leaving on good terms.

In fact, his prior boss, Larry Ellison, even chipped in to invest in this new business idea. Ellison recognized Benioff’s talent and supported his former all-star employee.

But this relationship would soon sour.

After early success, Benioff found out that Ellison, then a Salesforce board member, had been building a CRM service within Oracle, that directly competed with Salesforce itself. This eventually culminated in Benioff firing Ellison from the Salesforce board, and a more competitive relationship thereafter.

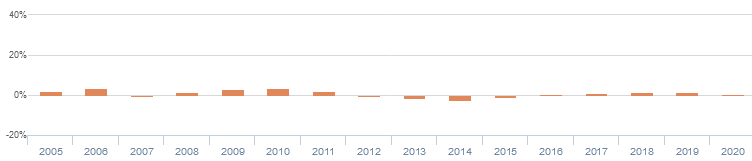

As we highlighted last Tuesday, Oracle had—and still has—a strong, high-return business, which makes this move by Ellison appear a mystery at first glance. Salesforce had relatively limited returns, and still has negative economic profitability:

The chart above highlights a company that hasn’t seen as-reported ROA improve beyond 5% at any point. Why would Oracle invest in an industry like CRM that clearly had limited potential?

It’s possible that Salesforce operates in a way that is focused on price competition and undercutting opposition, which is why their returns have been so low. Maybe Ellison thought Oracle could create a more valuable CRM solution and avoid price competition.

Or it’s possible the data is wrong, and CRM is actually highly lucrative.

After making the appropriate adjustments under Uniform Accounting, it’s clear that the second answer is correct.

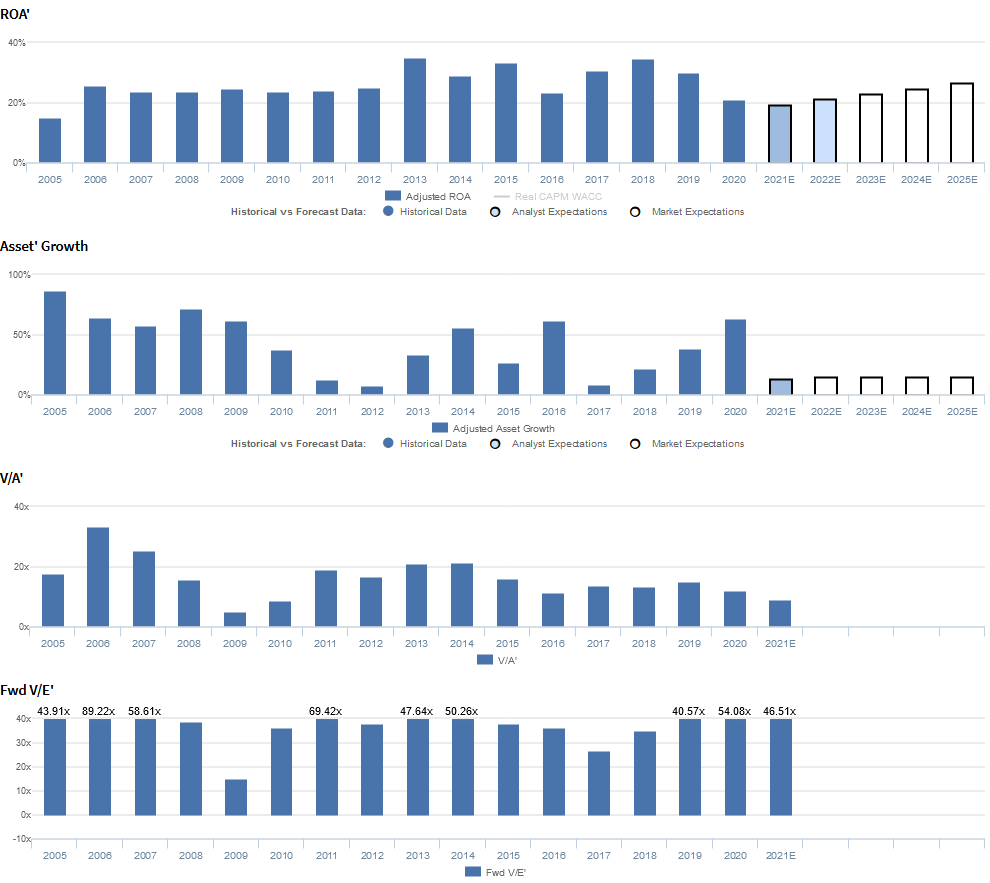

The chart above highlights that Salesforce’s Uniform ROA has actually been north of 20% since 2006, a business that has massive returns that almost rival Oracle’s 30%+ Uniform ROA levels.

Even more compelling, Salesforce has done this while also growing its Uniform assets by 30%+ in most years. This is a business that could invest massive amounts, and continue to get a return over 5x the cost of capital. Salesforce looks a lot like Oracle in Ellison’s early days.

That is why he wanted a piece back then.

Today, Salesforce’s returns remain strong, and as mentioned, so has growth. However, unlike in 1999, way more people want to be invested than just Ellison.

As a result, share prices have rocketed higher, and valuations have followed. The market clearly recognized the brilliance of what Benioff was doing, even if the numbers didn’t show it.

salesforce.com, inc. Embedded Expectations Analysis – Market expectations are for Uniform ROA to expand, but management may be concerned about MuleSoft, client wins, and digital transformation

CRM currently trades near historical highs relative to Uniform earnings, with a 46.5x Uniform P/E (Fwd V/E’).

At these levels, the market is pricing in expectations for Uniform ROA to expand from 21% in 2020 to 27% in 2026, accompanied by 15% Uniform asset growth going forward.

However, analysts have less bullish expectations, projecting Uniform ROA to remain at 21% by 2022, accompanied by 13% Uniform asset growth.

Since 2005, CRM has seen consistently robust profitability. Initially, the firm saw Uniform ROA improve from 17% in 2004 to 26% in 2006, before stabilizing at 24%-25% levels through 2012.

Since then, Uniform ROA expanded to a peak of 35% in 2018, and subsequently declined to 21% in 2020.

Meanwhile, the firm’s strategy of serially acquiring smaller firms has driven consistent, robust Uniform asset growth, ranging from 5%-87% since 2004.

Performance Drivers – Sales, Margins, and Turns

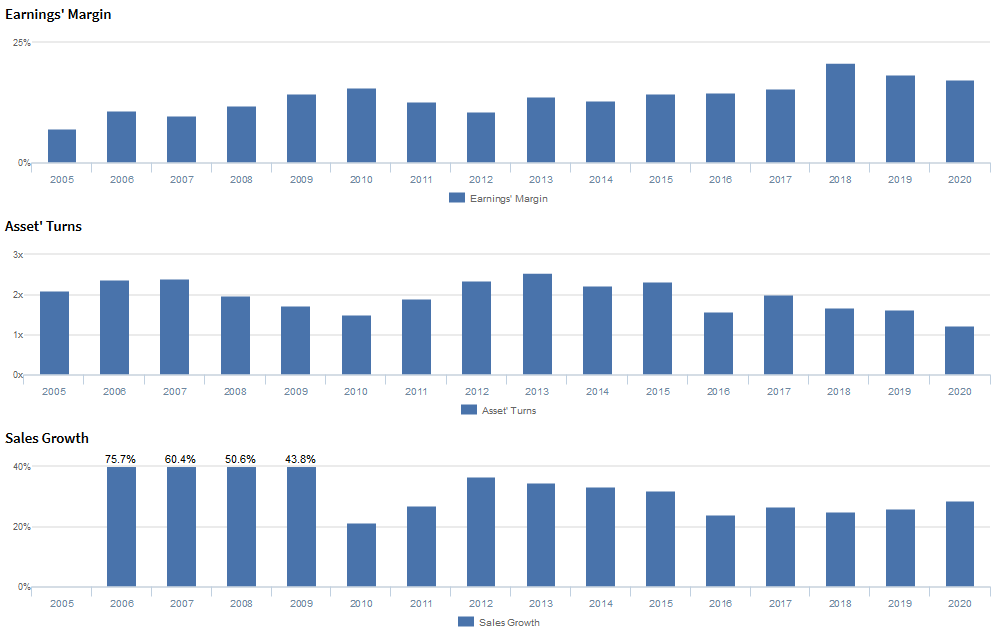

Consistent strength in Uniform ROA has been driven by the firm’s ability to offset declining Uniform asset turns with improvements in Uniform earnings margin.

From 2005-2010, Uniform margins improved from 7% to 18%, before fading to 11% in 2012. Thereafter, Uniform margins rebounded to 21% in 2018 and fell back to 17% in 2020.

Meanwhile, Uniform turns improved from 2.1x in 2005 to 2.4x in 2005-2006 before falling to 1.5x in 2010.

Since then, the firm has seen Uniform asset turns compress markedly to a low of 1.2x in 2020, excluding 2.5x outperformance in 2013.

At current valuations, markets are pricing in expectations for material improvements in both Uniform earnings margins and Uniform asset turns.

Earnings Call Forensics

Valens’ qualitative analysis of the firm’s Q3 2020 earnings call highlights that management is confident that their strategy is focused on creating a seamless customer experience and that they were glad to see 15% sales cloud growth.

However, management may be exaggerating the potential and significance of their MuleSoft acquisition, the strength of their positioning in the current macro environment, and their ability to meet sales guidance.

In addition, they may be concerned about the launch of their manufacturing and consumer goods clouds, and the sustainability of client wins in Europe and Latin America.

Finally, they may lack confidence in their ability to provide clients with a single view of every customer, and they may be overstating their customers’ focus on digital transformation.

UAFRS VS As-Reported

Uniform Accounting metrics also highlight a significantly different fundamental picture for CRM than as-reported metrics reflect.

As-reported metrics can lead investors to view a company to be dramatically stronger or weaker than real operating fundamentals highlight. Understanding where these distortions occur can help explain why market expectations for the company may be divergent.

As-reported metrics significantly understate CRM’s profitability.

For example, as-reported ROA for CRM was just 1% in 2020, substantially lower than Uniform ROA of 21%, making CRM appear to be a much weaker business than real economic metrics highlight.

Moreover, as-reported ROA has never exceeded 4%, while Uniform ROA has not fallen below 23% since 2006, distorting the market’s perception of CRM’s historical profitability ceiling for nearly two decades.

SUMMARY and salesforce.com, inc. Tearsheet

As the Uniform Accounting tearsheet for salesforce.com, inc. (CRM) highlights Uniform P/E trades at 46.5x, which is above corporate average valuations and around historical average valuations for the company.

High P/Es require high EPS growth to sustain them. In the case of Salesforce, the company has recently shown a Uniform EPS growth of 14%.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Salesforce’s Wall Street analyst-driven forecast is for robust Uniform EPS growth of 1% in 2021, and 27% in 2022.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $154 per share. These are often referred to as market embedded expectations.

In order to meet current market valuation levels, Salesforce would have to have Uniform earnings grow 28% each year over the next three years.

What Wall Street analysts expect for Salesforce’s earnings growth is below what the current stock market valuation requires.

Meanwhile, the company’s earnings power is 4x corporate averages, and their robust cash flows and cash on hand signal that there is low risk to the company’s operations and credit profile.

To conclude, Salesforce’s Uniform earnings growth is above peer averages, while the company’s price to earnings is also above peer average valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research