This company is benefiting as much as any other from employees having to work from home, and UAFRS reveals whether the market realizes it

The “At-Home Revolution” has introduced new problems for businesses this company is looking to solve. Today’s firm is aiding employees working from home by solving one specific issue.

Looking at as-reported numbers, it appears the firm has negative returns. Uniform results tell a different story.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

We have talked extensively about the “At-Home Revolution” and how it has affected many companies, including Fortune Brands (FBHS) and Conagra Brands (CAG). The rapid change of consumption patterns across the country and the entire globe has been astonishing.

Demand has spiked for alcohol, cleaning supplies,cyber security systems, and even homes since the beginning of the coronavirus pandemic.

Overall, one of the biggest drivers of the At-Home Revolution has been companies embracing work from home. The coronavirus pandemic forced many companies to move online. Even today, many parts of the country have restrictions about who is able to go into the office.

Many companies are planning to continue the trend even after the pandemic is over. We here at Valens will be partly remote going forward. Furthermore, companies like Facebook (FB), Twitter (TWTR), and Shopify (SHOP) have all declared they will stay at least partially remote after stay-at-home restrictions are fully lifted.

The reason for this is twofold. The first is employees are able to be just as productive or more productive working from home. Working from home allows an employee to eliminate travel time, meaning he or she is able to get more sleep and feel refreshed for the day. Also, working from home allows for a more flexible schedule, boosting company morale.

The other reason is companies can cut down on rental expenses and office spaces. Offices, especially in large urban centers, can be expensive. However, if only 50% of a workforce is in an office at any given time, the company is able to downsize and save a considerable amount of money.

While there are many positives to working from home, companies still need to make changes in order to adapt to the loss of face-to-face interactions. One of the most important technologies is being able to have virtual meetings through a service like Zoom (ZM) or Skype for Business. These platforms allow teams to have important conversations and meetings while still being physically apart from one another.

Signing and executing documents is another essential business action that needs to adapt to the new environment. Legal contracts need to be signed in order to be valid. Without having employees in the same office, it becomes difficult to sign these documents in a reasonable time frame.

One company that has been at the forefront of enabling people to sign documents virtually is DocuSign (DOCU). DocuSign has an intuitive platform that works with both small and large businesses. DocuSign is also accessible through a variety of devices and features many applications.

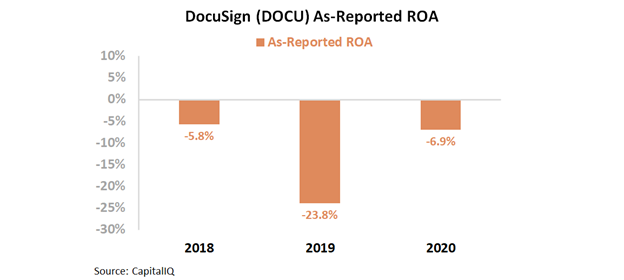

Even with the surging demand it has been seeing, it appears as though DocuSign makes no profit. As-reported return on assets (ROA) has been negative since the firm went public. Most recently, DocuSign had a -7% ROA.

However, this picture of DocuSign is inaccurate. GAAP’s treatment of stock option expenses, among other distortions, is distorting DocuSign’s profitability metrics.

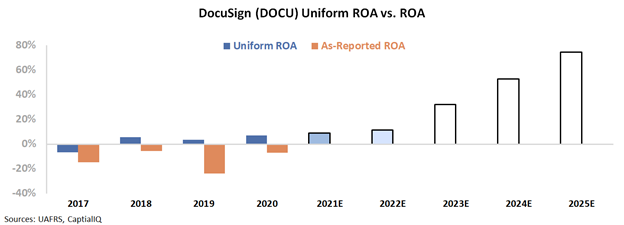

Uniform Accounting shows the firm has had a positive ROA since even before the coronavirus pandemic. This year, Uniform ROA improved to 7%, DocuSign’s highest level ever.

Uniform Accounting is able to demonstrate that DocuSign is in fact a profitable company. However, to obtain a full grasp on the stock, we must look at forecasts and expectations. To evaluate expectations, we can use the Embedded Expectations Framework.

The chart below explains the company’s historical corporate performance levels, in terms of ROA (dark blue bars) versus what sell-side analysts think the company is going to do in the next two years (light blue bars) and what the market is pricing in at current valuations (white bars).

The below graph shows sell-side analysts expect ROA improvements to continue over the following two years and reach 11% in 2022. Then, the market is pricing in Uniform ROA to skyrocket to 74% by 2025.

This would be astronomical growth for a firm which at the moment has below corporate average profitability levels. Even if a large percentage of the American workforce stays at home, it is hard to imagine DocuSign being able to improve its ROA by such a huge margin.

Ultimately, Uniform Accounting shows the true strength of DocuSign’s business. Without it, investors would not be aware DocuSign has positive profitability metrics.

However, the market is expecting sizable Uniform ROA improvement over the following years. Even with positive tailwinds from widespread adoption of working from home, this level appears to be improbable for DocuSign to achieve.

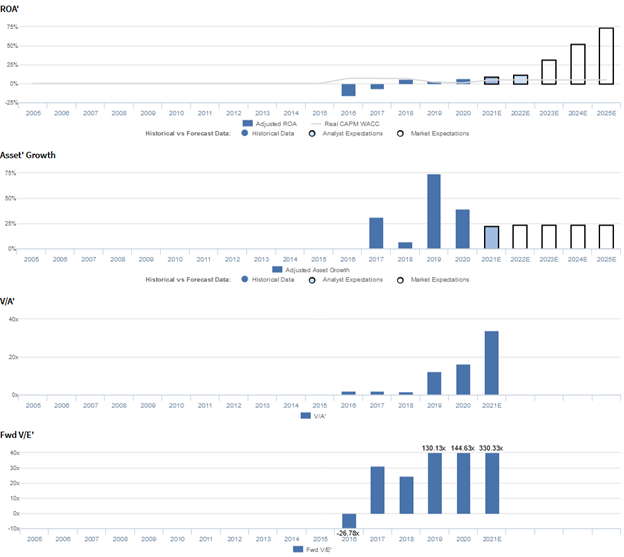

DocuSign, Inc. Embedded Expectations Analysis – Market expectations are for Uniform ROA to reach record highs, but management may have concerns about adoption, costs, and DocuSign Gen

DOCU currently trades at historical highs relative to Uniform earnings, with a 330.3x Uniform P/E (Fwd V/E’). At these levels, the market is pricing in expectations for Uniform ROA to jump from 7% in 2020 to 74% in 2025, accompanied by 24% Uniform asset growth going forward.

Meanwhile, analysts have less bullish expectations, projecting Uniform ROA to only rise to 11% through 2022, accompanied by 23% Uniform asset growth.

Historically, DOCU has seen generally improving profitability. After inflecting from negative levels in 2016-2017 to 6% in 2018, Uniform ROA slipped to 4% in 2019 before rebounding to 7% in 2020.

Meanwhile, Uniform asset growth has been consistent, positive in each of the past four years, while ranging from 7% to 40%, excluding 74% growth in 2019, driven by significant working capital growth post-IPO.

Performance Drivers – Sales, Margins, and Turns

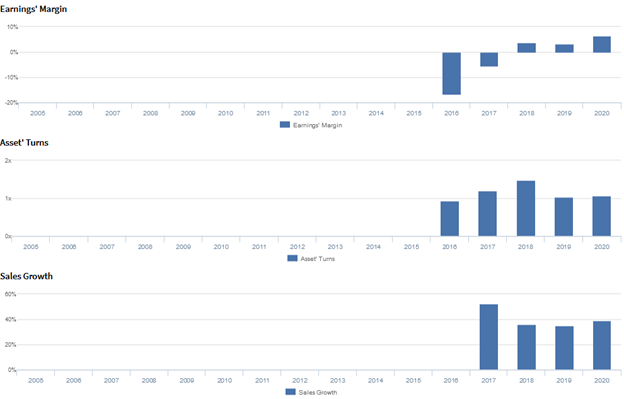

Trends in Uniform ROA have been driven by trends in Uniform earnings margins and Uniform asset turns.

After inflecting from negative levels in 2016-2017 to 4% in 2018, Uniform margins fell to 3% in 2019 before recovering to a peak of 7% in 2020. Meanwhile, Uniform turns improved from 0.9x in 2016 to a peak of 1.5x in 2018, before fading to 1.1x in 2020.

At current valuations, markets are pricing in expectations for a rapid expansion in both Uniform margins and Uniform turns to new peaks.

Earnings Call Forensics

Valens’ qualitative analysis of the firm’s Q1 2021 earnings call highlights that management is confident a significant portion of the 10,000 direct customers came from the e-signature segment.

However, management is also confident Seal is going to have a near-term small dilutive effect on gross margins and that small companies may not need complex CLM systems. Moreover, they may have concerns about the sustainability of customer demand, rising days billing outstanding, and the potential of DocuSign Gen.

Furthermore, they may lack confidence in their ability to continue reducing overall expenses, secure more one-time projects, and sustain gross margins. Management may also have concerns about delays in adoption due to the perception that DocuSign isn’t legal in various markets, continued travel industry headwinds, and their video identification capabilities.

UAFRS VS As-Reported

Uniform Accounting metrics also highlight a significantly different fundamental picture for DOCU than as-reported metrics reflect.

As-reported metrics can lead investors to view a company to be dramatically stronger or weaker than real operating fundamentals highlight. Understanding where these distortions occur can help explain why market expectations for the company may be divergent.

As-reported metrics significantly understate DOCU’s margins, one of the primary drivers of profitability.

For example, as-reported EBITDA margin for DOCU was -15% in 2020, materially lower than Uniform earnings margin of 7% in the same year, making DOCU appear to be a much weaker business than real economic metrics highlight.

Moreover, as-reported margins have remained negative since the firm’s inception, while Uniform margins inflected positively in 2018, significantly distorting the market’s perception of the firm’s profitability ceiling.

SUMMARY and DocuSign, Inc. Tearsheet

As the Uniform Accounting tearsheet for DocuSign, Inc. (DOCU:USA) highlights, the Uniform P/E trades at 330.3x, which is significantly above the global corporate average valuation levels and its historical average valuations.

High P/Es require high EPS growth to sustain them. In the case of DocuSign, the company has recently shown a 109% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, DocuSign’s Wall Street analyst-driven forecast is a 107% and 77% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify DocuSign’s $212 stock price. These are often referred to as market embedded expectations.

In order to justify current stock prices, the company would need to have Uniform earnings grow by 101% per year over the next three years. What Wall Street analysts expect for DocuSign’s earnings growth is above what the current stock market valuation requires in 2021, but below what the market requires in 2022.

Furthermore, the company’s earning power is around the corporate average. However, cash flows and cash on hand are above their total obligations—including debt maturities and capex maintenance. Together, this signals low credit risk.

To conclude, DocuSign’s Uniform earnings growth is above peer averages. Therefore, as is warranted, the company is also trading above average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research