This company is excited to welcome chip manufacturers home

After seeing the supply chain failures during the pandemic, governments and companies are ramping up their investments to prevent these issues from not happening again.

The urgency in fixing supply chains and making them more secure is particularly urgent in the semiconductor space and there is a big winner of this.

That is the semiconductor equipment companies like ASML Holding (ENXTAM:ASML). The company has already seen the demand skyrocket for its advanced semiconductor systems in 2021.

The investments in supply chain and infrastructure are just starting and this might be the beginning of a decade of high profitability for the company.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

We have been talking about how the U.S. and the rest of the world have ignored supply chain investments for the last decade.

It came back to haunt us…

Issues with supply chains became glaringly obvious when the pandemic hit.

Companies had problems getting their hands on the raw materials and key components and customers began to see delayed and canceled orders.

Now, governments and companies are working together to make supply chains more resilient and efficient.

For instance, the Bipartisan Infrastructure Bill that was passed by Congress in 2021 allowed spending as much as $1.2 trillion on these efforts.

This includes renewing existing infrastructure, building new roads, bridges, and rails, and delivering high-speed internet to underserved areas.

This isn’t just true in the U.S. either.

This move has in particular been apparent in the semiconductor space. The U.S. and other nations are scrambling to convince semiconductor companies to build chip facilities in their nations.

While this might mean rising costs for chip manufacturers, there is one clear winner in all this.

That is the semiconductor equipment makers who are going to be selling a lot more kits to these new facilities.

ASML Holding (ENXTAM:ASML) is a great example. The company develops and sells advanced semiconductor equipment systems for memory and logic chip makers.

As investments in this space ramped up after the pandemic in 2021, the company has seen its earnings margins and asset turns surge to all-time high levels in the last decade.

Have a look at it yourself…

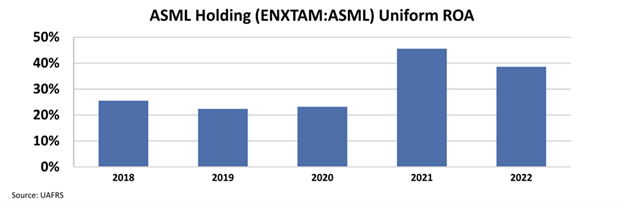

The Uniform return on assets (ROA) of the company doubled from 23% in 2020 to 46% in 2021. That is a massive increase in only one year.

The business was still booming last year, and the company managed to keep the ROA around 40%.

This is the start of a decade of investments in supply chains and infrastructure.

The Supply Chain Supercycle is only beginning, and governments will collaborate with companies to make supply chains more efficient.

This is also what the Wall Street analysts are thinking. They are estimating a 44% Uniform ROA in 2023, showing that the company can continue to see increasing demand.

Considering these facts, it would not be surprising to see the business continue to boom and profitability stay high.

SUMMARY and ASML Holding N.V., Tearsheet

As the Uniform Accounting tearsheet for ASML Holding N.V., (ASML:NLD) highlights, the Uniform P/E trades at 31.2x, which is above the corporate average of 18.4x but around its historical P/E of 31.6x.

High P/Es require high EPS growth to sustain them. In the case of ASML, the company has recently shown a 59% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, ASML’s Wall Street analyst-driven forecast EPS to grow immaterially in 2022 and by 32% EPS growth in 2023.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify ASML’s $602 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 6% annually over the next three years. What Wall Street analysts expect for ASML’s earnings growth is below what the current stock market valuation requires in 2022 but above its 2023 requirement.

Furthermore, the company’s earning power is 8x its long-run corporate average. Moreover, cash flows and cash on hand are 3x its total obligations—including debt maturities, capex maintenance, and dividends. Also, the company’s intrinsic credit risk is 30bps above the risk-free rate.

All in all, this signals low dividend risk.

Lastly, ASML’s Uniform earnings growth is in line with its peer averages but above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research