This consumer staples firm may no longer be the safe play it used to be

Consumer staples firms were once seen as safe bets because they tend to be insulated from macroeconomic headwinds and volatility.

However, with consumers facing significant pressure in recent years, that assumption may no longer be true.

General Mills (GIS) a consumer staples giant recently cut its sales outlook for 2026, citing weak consumer sentiment.

Since 2018, the company has delivered 20%+ returns annually. But with consumer sentiment declining steeply, investors are expecting its returns to plummet in the next few years.

Investor Essentials Daily:

Thursday News-based Update

Powered by Valens Research

Consumer staples firms have long been seen as stable investments because they tend to be insulated from macroeconomic headwinds and volatile market swings.

In past decades where the S&P 500 dipped by 20% or more, the consumer staples sector has generally outperformed the index.

The most recent example of this is the major stock market selloff in 2022. After peaking in January, the S&P 500 fell around 25% by October. In that same period, consumer staples firms like General Mills (GIS) saw their valuations rise.

Fast forward to today, these consumer staples firms may no longer be the safe bets they used to be.

Over the past three years, the S&P 500 has risen by 79%, meanwhile packaged foods firms have only seen steady declines in performance.

And while it’s easy to point to the rise of healthy eating trends and weight-loss drugs as the primary drivers, there’s a more significant factor at play: Consumer pressure.

With prices on the rise, consumers have had to trade down to cheaper alternatives and become more selective about their spending, resulting in lower sales for retailers. In December last year, retail sales stood flat at $735 billion, falling short of the 0.4% increase analysts were expecting.

However, price inflation isn’t the only problem confronting consumers. The latter had been negatively impacted by high interest rates, a cooling job market, stagnating wage growth, and rising delinquencies in recent years.

As a result of all these pressures, consumer sentiment has worsened. According to the Conference Board’s most recent report, U.S. consumer confidence has dropped from 94.2 in December last year to 84.5 in January this year.

With sentiment down, General Mills has been forced to temper its sales outlook and confront the prospect of declining sales.

General Mills is a packaged foods firm known primarily for brands like Cheerios, Wheaties, and Pillsbury. Last year, the company turned to promotions and price cuts to take back the market share it lost due to the previously mentioned consumer trends.

While this strategy worked in winning over a portion of budget-conscious consumers, this hasn’t been enough to stop the company from lowering its sales and profit outlook for 2026.

Earlier this week, General Mills announced that organic net sales would be down 1.5% to 2% for its current fiscal year after “weak consumer sentiment, heightened uncertainty, and significant volatility have weighed on category growth and impacted consumer purchase patterns, resulting in a slower pace and higher cost of volume recovery than initially expected.”

The company’s shares are down 7% after making the announcement.

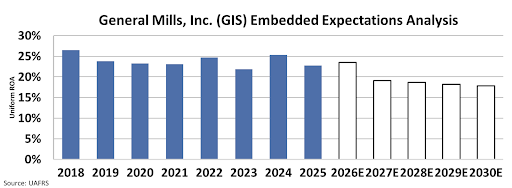

General Mills has historically been a strong performer. Since 2018, the company has delivered a Uniform return on assets (“ROA”) in excess of 20%. However, with consumers facing significant pressure, investors are doubting the company’s ability to sustain this stability.

By 2030, the market expects General Mills’ Uniform ROA to decline to 18%, falling below the 20% returns it has delivered since 2018.

While it will take time to gauge the true health of the consumer as the economy evolves, investors should take care to know General Mills may no longer be the safe play it once was.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research