This data storage manufacturer could warrant upside as the demand for storage intensifies

The AI boom is accelerating data center buildouts and IT- and cloud-related spending.

While mainstream narrative has centered around the design and acquisition of advanced AI chips, there’s another section of the tech market that’s seeing surging demand.

AI-related workloads don’t just require computational horsepower—these processes rely on data storage too.

That’s why after seeing storage prices fall sharply to all-time lows in 2023, manufacturers of NAND and HDD memory are seeing demand skyrocket, to the point where a supply shortage is expected to persist.

With HDDs set to see an uptick in demand, resulting in higher prices, Western Digital (WDC) is positioned to capitalize. Even though the company’s returns trended negatively in 2023 and 2024, it’s seen an improvement this year, generating a Uniform ROA of 12%.

Despite this improvement, the market is betting against the company, expecting returns to remain at just 15% by 2030.

Investor Essentials Daily:

Wednesday News-based Update

Powered by Valens Research

As mentioned in past articles, today’s artificial intelligence (“AI”) boom is accelerating expenditure towards the acquisition of advanced chips and other information technology– (“IT”) and cloud-related spending.

AI-related workloads require not only massive amounts of energy but also vast amounts of computational horsepower. However, that doesn’t end there.

These complex computations consume petabytes of data that need to be processed and stored. In this regard, NAND, a type of non-volatile flash memory used in most solid state drives (“SSDs”), has attracted demand from hyperscalers due to fast read and write speeds, which are highly sought after in training advanced AI models.

But that’s not the only type of storage AI firms want access to. Traditional hard disk drives (“HDDs”) are seeing an uptick in demand because these are significantly cheaper on a per-terabyte basis than their SSD counterparts.

Moreover, while AI models consume petabytes of data, not all of it has to be accessed at once, making HDDs a reliable and cheaper option for storing “cold data”—data that remains in storage and is not needed for immediate retrieval.

This year alone, the storage market is forecasted to generate revenues of nearly $68 billion. Subsequently, market volume is expected to grow to as much as $103 billion by 2030.

In 2023, SSD and HDD prices cratered to all-time lows due to oversupply, prompting storage makers to cut output and stem the downturn’s negative effects. However, by 2024, prices started to climb due to AI-driven demand.

Presently, the storage market is expected to see shortages for both NAND and HDDs, the latter of which has historically remained cheap when SSD prices went up, as hyperscalers race to secure available supply.

With HDDs set to see an uptick in demand, resulting in higher prices, storage makers like Western Digital (WDC) are positioned to capitalize.

Western Digital is one of the leading manufacturers of HDDs alongside Seagate (STX) and Japanese tech firm Toshiba.

At present, the company services both enterprise and consumer markets with a wide variety of offerings ranging high-capacity HDDs, data center drives, storage platforms, external drives, portable drives, network attached storage (“NAS”) solutions.

For the past several years, Western Digital has trailed Seagate, however, the former has slowly closed this gap.

As of early 2025, Western digital has shipped 12.1 million units and an estimated 179.8 exabytes of storage capacity, slightly better numbers than Seagate which sent out 11.4 million units and around 143.6 exabytes of storage.

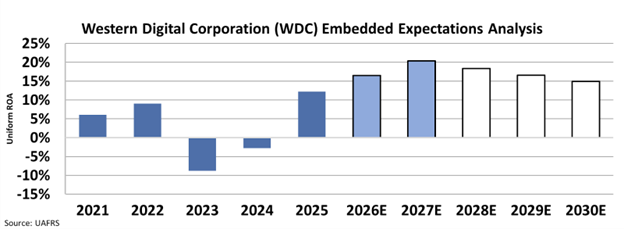

The company, after seeing its returns dip to negative levels in 2023 and 2024 due to storage price drops, saw its Uniform return on assets (“ROA”) trend positively at 12% this year.

With HDD storage comprising around 80% of current data storage, Western Digital is poised to improve its prospects moving forward, especially as demand for storage—from both AI and consumer markets—is still set to grow.

Despite the improvement in its returns, the market remains skeptical of this business.

We can see what the market thinks about this company through our Embedded Expectations Analysis (“EEA”).

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At current valuations, Wall Street analysts expect Western Digital’s returns to climb to 20% in the next two years. However, the market is betting that Uniform ROA will drop to 15% by 2030.

Wall Street analysts on the other hand have a more optimistic viewpoint. Analysts expect Western Digital’s ROA to continue climbing over the next two years, reaching 20% by 2027.

Considering the current AI-dominated environment, analysts believe that Western Digital will benefit from a strong cycle that should prove robust in the coming years.

As Western Digital continues to benefit from growing demand for its storage chips, it could continue to outperform market expectations, warranting equity upside for investors.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research