This digital marketing firm is one of the few that successfully monetizes AI

Artificial intelligence is reshaping industries, and Zeta Global’s (ZETA) marketing cloud, powered by its ZOE AI tool, helps companies find and engage customers more efficiently.

Its platform sits in a $19 billion market but generated only $1 billion in revenue in 2024, leaving ample room for growth as it serves over 44% of the Fortune 100.

Zeta has grown revenue by 38% in the past year and expanded its largest client contracts through a “land and expand” strategy.

Despite these strong fundamentals, a short‑seller report, filled with inaccuracies, drove the stock down 52%, creating what could be a significant revaluation opportunity.

Investor Essentials Daily:

Tuesday News-based Update

Powered by Valens Research

Artificial intelligence has been at the forefront of the market for the last year as new advancements in technology continue to show industry-altering potential.

While the next few years will lead to the birth of a plethora of new technologies, the winners will be companies that can use AI effectively and monetize their solutions.

This is the basis for Zeta Global’s (ZETA) entire business model.

The company’s marketing cloud, powered by the Zeta Opportunity Engine (“ZOE”) AI tool, helps companies identify potential customers and optimize their marketing strategies.

It plugs into existing sales software and examines data and interactions to uncover ways to sell and market more efficiently.

Not only does ZOE identify leads, but it also recommends the best ways to engage them. Ultimately, its job is to make selling easier, a space within AI that’s bound for growth.

Zeta’s platform is in the “marketing technology” market, which is valued at $19 billion and expected to keep growing by ~14%.

As of 2024, the firm only had a small slice of this industry with a revenue of $1 billion, meaning it has plenty of share left to capture.

Zeta services every major sector and more than 44% of Fortune 100 companies. As more companies invest in AI tools, Zeta’s business has been booming. In the past year, its revenue has increased by 38%.

As the firm grows its customer base, it’s also figuring out how to make more money from existing customers, using its “land and expand” strategy.

Zeta signs small contracts to get customers in the door. Then, once it shows how valuable it is, customers spend more money on adding new features and users to the platform.

That’s how the company grows clients into scaled customers that spend at least $100,000 per year, and super-scaled customers that spend at least $1 million. In the past year alone, Zeta grew scaled customers by 19% and super-scaled by 10%.

Scaled customers who’ve been with the company less than a year spend about $600,000 on average. Once they’ve been around for one to three years, they spend about $1.3 million per year. After three years, they spend upwards of $2.1 million.

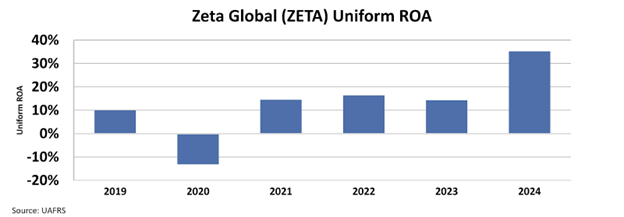

Zeta has leveraged a maturing customer base, an asset-light model, and valuable technological moat to garner a Uniform return on assets ”ROA” of over 35%, while still growing at an impressive 30%+ clip.

Despite this, the firm only trades at a 16x Uniform P/E, well below current market averages.

This is due in part to disparaging headlines in November that led the stock to plummet 52% within a week.

An activist short report was published accusing Zeta of round-tripping revenue, having management with shady backgrounds, and relying on suspect business practices to acquire customer information it uses as part of its business.

However, a closer read highlights reasons not to panic. For instance, the report discusses Zeta’s auditor as Ernst & Young despite the fact that the firm has never audited Zeta (Deloitte is the company’s auditor).

Meanwhile, the company’s only likely client with “round tripping” potential (where it has a relationship where it is both paying a vendor, and the vendor is paying them) is Snowflake.

This large data lake and cloud vendor has this type of relationship with many customers, and Zeta’s business does not seem to be unique in this regard.

Plus, the company has been clear that it follows strict rules about how to get customer consent to access data, and the parts of its business referenced in the short report are immaterial parts of its business.

As such, many of these concerns that continue to be a short-term valuation overhang appear to be overblown.

Lingering concerns about the validity of the short report appear to explain how, despite a fantastic business model and powerful tailwinds, the market hasn’t grasped Zeta’s profitability potential.

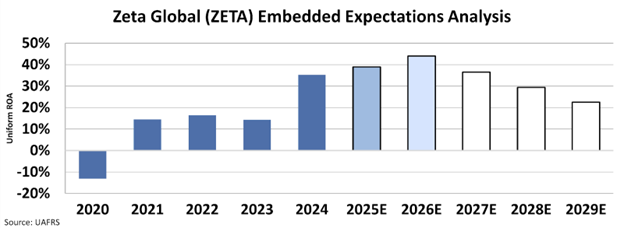

We can see what the market thinks through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market expects the company’s Uniform ROA to decline to around 22% from 35% last year.

With time and continued strong execution, Zeta could be met with a significant revaluation.

Zeta is a great example of how smart AI users have some of the biggest potential in the AI ecosystem.

It has proven the viability of its own AI tools, and as more companies flood the market with products and innovations, Zeta should be well-positioned to support their marketing efforts.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research