This fund uses a grassroots campaigning technique normally used to push for political change to unlock value in its investments

Letter-writing campaigns not only allow grassroot activists to reach political representatives, it can also help activist investors influence company management.

This activist manager and his fund have championed this technique to push high-quality firms to reach their true growth potential by exploring new business opportunities and avenues, whether through mergers, acquisitions, divestitures, management change, or strategic shifts.

Using as-reported metrics, it’s not clear that this performance can be sustained as the tone of this manager’s activism has softened. However, using Uniform Accounting, we can understand if the fund is still able to identify companies that only need a little push in order to reap massive returns.

In addition to examining the portfolio, we’re including a deeper look into the fund’s largest current holding, providing you with the current Uniform Accounting Performance and Valuation Tearsheet for that company.

Investor Essentials Daily:

Friday Uniform Portfolio Analytics

Powered by Valens Research

One of the favorite tactics among grassroot activist campaigns, particularly in politics, is a letter-writing campaign.

By flooding their representatives with personalized messages from constituents, these activists force-elected officials to have to pay attention to their campaigns. Through these efforts, the activists hope to be able to change their representatives’ opinions and lead them to support the bills or issues that they find relevant.

This type of advocacy has helped give people a stronger voice in their governments for centuries.

However, it is not just activists looking to impact government policy that turn to letter-writing campaigns. From time to time, various activist investing have also dabbled in writing letters to company management in hopes of eliciting change.

One of the great activist letter writers is Dan Loeb, founder and CEO of the hedge fund Third Point. In his early years as an activist at the firm, he was known to be a little more “rough around the edges,” bludgeoning unsuspecting company management teams with opinions on how to better drive shareholder value, or more specifically, how they were destroying it.

Many on Wall Street would wait with bated breath to see which executive was next on Loeb’s list to attack.

Loeb had tremendous success as an activist, enacting change by pushing management teams, at times with scathing letters, to take a deeper look at their business and implement changes that could ultimately lead to greater long-term value for the company and all shareholders.

As he has gained more experience with age, and as his incredible investment track record has become well-known, his tone has softened. Even so, his investment acumen has not diminished. Looking at his portfolio, it’s clear that is the case.

We’ve conducted a portfolio audit of Third Point’s top holdings, based on its most recent 13-F.

We’re showing a summarized and abbreviated analysis of how we work with institutional investors to analyze their portfolios.

Unsurprisingly, as-reported metrics of Third Point’s investments make it look like the fund is not focusing on the potentially lucrative firms that would make an activist investor salivate. In reality, these investments appear to fit the bill, once Uniform Accounting metrics are reviewed.

It’s clear that when Third Point is making its investment decisions, the team is making decisions based on the real data, and looking for opportunities to make an impact.

See for yourself below.

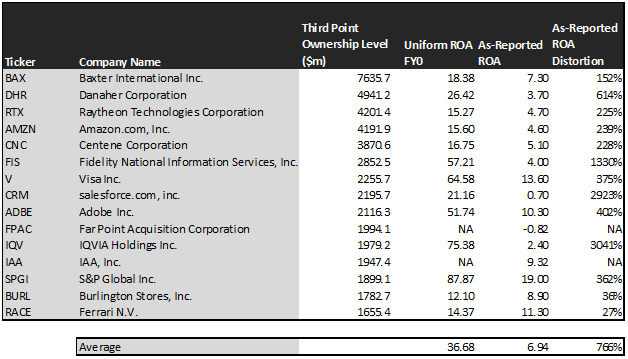

Using as-reported accounting, investors would think Third Point was buying businesses that even activist investors with intentions to influence management wouldn’t recommend.

On an as-reported basis, many of these companies are poor performers with returns that are sometimes even negative, with an average as-reported return on assets (ROA) of just 7%.

In reality, the average company in the portfolio displays an impressive average Uniform ROA of nearly 37%.

Once we make Uniform Accounting (UAFRS) adjustments to accurately calculate earning power, we can see these are the kind of high potential companies that an activist investor would be interested in pursuing.

Once the distortions from as-reported accounting are removed, we can realize that Amazon (AMZN) doesn’t have a 5% ROA, it is actually at 16%.

Similarly, Danaher’s (DHR) ROA is really 26%, not 4%. While as-reported metrics are portraying the company as a below cost-of-capital business, Uniform Accounting shows the company’s real robust operations.

Salesforce.com (CRM) is another great example of as-reported metrics mis-representing the company’s profitability.

Salesforce doesn’t have a 1% ROA, it is actually at 21%. Third Point appears to understand that investors viewing this as a company without a compelling moat, thinking it’s a weak business, are completely incorrect.

The list goes on from there, for names ranging from Adobe (ADBE) and Visa (V), to IQVIA Holdings (IQV), S&P Global (SPGI), and even Ferrari (RACE).

If Third Point were focused on as-reported metrics, it would never pick most of these companies because they look like anything but companies a prudent activist would be focused on.

But it appears that Third Point’s criteria extends past just high-quality firms. It is also focused on companies that can still have solid growth potential—potential it may be able to accelerate.

It wouldn’t necessarily be apparent when looking at the as-reported metrics, but Uniform Accounting metrics paint a complete picture of the fund’s investment philosophy.

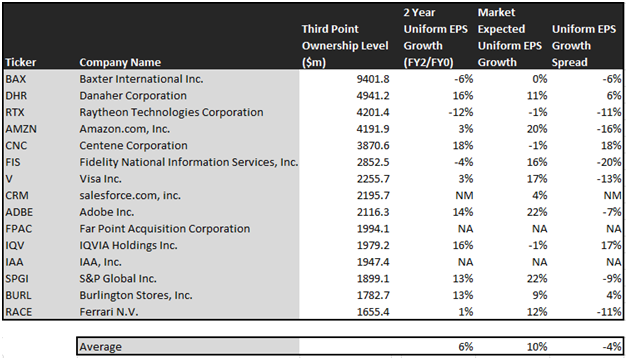

This chart shows three interesting data points:

- The 2-year Uniform EPS growth represents what Uniform earnings growth is forecast to be over the next two years. The EPS number used is the value of when we take consensus Wall Street estimates and we convert them to the Uniform Accounting framework.

- The market expected Uniform EPS growth is what the market thinks Uniform earnings growth is going to be for the next two years. Here, we show by how much the company needs to grow Uniform earnings in the next 2 years to justify the current stock price of the company. If you’ve been reading our daily analyses and reports for a while, you’ll be familiar with the term embedded expectations. This is the market’s embedded expectations for uniform earnings growth.

- The Uniform EPS growth spread is the spread between how much the company’s Uniform earnings could grow if the Uniform earnings estimates are right, and what the market expects Uniform earnings growth to be.

The average company in the US is forecast to have 5% annual Uniform Accounting earnings growth over the next 2 years. Third Point’s holdings are forecast by analysts to slightly eclipse that, growing at 6% a year the next 2 years, on average.

That being said, the companies are not intrinsically undervalued on average, the market is expecting stronger growth than is forecast. The fund is carefully selecting companies it believes it can have a hand in improving, in hopes of realizing robust returns.

On average, the market is pricing these companies to grow earnings by 10% a year. The market is pricing these companies for growth to be 4% higher than analysts are forecasting. Third Point is betting it can help these companies outperform expectations.

Some companies in its portfolio already have high growth expectations, including a few that stand to benefit from near-term coronavirus driven tailwinds, such as health insurance intermediary Centene (CNC) and clinical research support provider IQVIA (IQV).

While the average company is forecast to have 5% Uniform earnings growth the next 2 years by analysts, these firms are forecast to have 18% and 16% growth, respectively. Importantly, the market is significantly more pessimistic too, 1% earnings shrinkage for both names.

That said, there are also names in the portfolio for which the market is paying a higher premium, but which analysts believe will disappoint. In these scenarios, perhaps Third Point sees opportunities to influence management in order to meet, and even exceed, expectations.

An example of a company with this dislocation is Fidelity National Information Services (FIS). The company is forecast by analysts to shrink by 4% a year, well below averages, but the market is expecting the company to deliver 16% growth annually.

Meanwhile, some firms in Third Point’s portfolio are projected to have paltry earnings growth by both analysts and the market. Here, the firm may be in a position to shock both, opening the door up for rapid stock price appreciation.

For instance, the firm’s top holding, Baxter International (BAX) is forecast to have 6% shrinkage over the next 2 years by analysts and immaterial growth going forward by the market. If Third Point can help management procure any meaningful growth, significant upside can be warranted.

Overall, it is clear Third Point is investing in high-quality names that could have surprising growth potential. It believes it can help names with already strong fundamentals shock market expectations and pursue exciting merger opportunities or implement strategic shifts.

If not, maybe Loeb will just write a strongly worded letter to management.

It wouldn’t be clear under GAAP, but unsurprisingly Uniform Accounting shows the real performance and potential of Third Point’s holdings.

SUMMARY and Baxter International Inc. Tearsheet

As Third Point Management’s largest individual stock holding, we’re highlighting Baxter International Inc.’s tearsheet today.

As the Uniform Accounting tearsheet for Baxter International Inc. (BAX:USA) highlights, Baxter’s Uniform P/E trades at 24.5x, which is above corporate average valuations and its historical average levels.

High P/Es require high EPS growth to sustain them. In the case of Baxter, the company has recently shown a 69% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that, in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Baxter’s Wall Street analyst-driven forecast is a 24% Uniform EPS decline in 2020, followed by a 16% Uniform EPS growth in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Baxter’s $84 stock price. These are often referred to as market embedded expectations.

The company can have Uniform earnings shrink by 1% each year over the next three years and still justify current price levels. What Wall Street analysts expect for Baxter’s earnings growth is below what the current stock market valuation requires in 2020 but above that requirement in 2021.

Furthermore, the company’s earning power is 3x the corporate average. Also, cash flows are significantly higher than its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, Baxter’s Uniform earnings growth is in line with peer averages in 2020. However, the company is trading below average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research