This grocery giant is trying to emulate Walmart’s playbook

Supermarket giant Kroger (KR) generates around $150 billion in revenue.

And that scale gives it plenty of bargaining power in the grocery retail space. However, with prices rising, its target customers are now comparing the cost of every item against other players.

To compete, CEO Greg Foran is attempting to leverage Walmart’s (WMT) playbook. However, adopting that strategy is easier said than done.

Investor Essentials Daily:

Wednesday News-based Update

Powered by Valens Research

With gas and housing prices rising, many U.S. consumers are targeting the grocery aisle.

Unfortunately, that’s bad timing for supermarket giant Kroger (KR).

What started as a single shop in Cincinnati has grown into more than 20 regional brands. Nowadays, Kroger generates roughly $150 billion in annual revenue.

That scale used to give it plenty of bargaining power in the grocery retail space. But now, it’s facing a customer who compares the cost of every item against other retailers such as Walmart (WMT), Amazon (AMZN), Costco Wholesale (COST), and private discount chains like Aldi and Trader Joe’s.

Kroger tried to expand by acquiring supermarket chain Albertsons (ACI). But the deal was blocked on antitrust grounds in December 2024.

Without Albertsons’ stores and purchasing power, Kroger can’t match the prices of discount chains. And now it’s facing the consequences of that failed merger.

Kroger’s new CEO, Greg Foran, is moving fast to accommodate tighter consumer budgets. He wants the company to test lower prices on some products then spread those discounts across the store.

Foran ran Air New Zealand for about five years. But U.S. retail investors know him best from his time at Walmart.

Foran led its Chinese operation, then all of Asia, and then its U.S. operation. He helped Walmart cut costs to keep customers in the door. Its U.S. division produced 20 straight quarters of same-store sales growth from 2014 to 2019.

At Kroger, Foran is looking to apply the same strategy. Management wants faster checkout speeds in stores and a better e-commerce experience, alongside lower prices on thousands of products.

The price piece is a risky bet as it puts Kroger up against a master of competitive pricing.

Walmart recently lowered its prices on about 7,200 food items, roughly 20% more products than in 2025.

Walmart can afford to make less profit on things like cereal, meat, and household staples because once shoppers are in the door for groceries, they often leave with other items. This includes apparel, electronics, pharmacy items, or home goods.

The company’s massive scale also makes suppliers more willing to accept lower prices.

Kroger may dominate the grocery market, but Walmart covers the entire retail landscape.

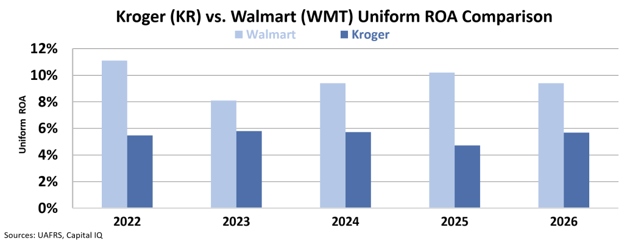

Walmart’s Uniform return on assets (“ROA”) is about 9%, which is modest. But it allows Walmart to stay above its cost of capital after lowering prices.

Kroger’s Uniform ROA sits at nearly 6%, which almost matches its cost of capital. That means the business earns just enough to cover expenses and investor returns.

With a 9% Uniform ROA, Walmart can cut prices, maintain its customer count, and still generate some profit.

Kroger, on the other hand, doesn’t have a cushion. With lower prices, it wouldn’t take much to start losing money on every transaction.

Simply said, Kroger can’t win a war of attrition with Walmart.

Walmart is the largest U.S. company by revenue, and it has a broader profit pool and deeper purchasing power. Plus, its stores offer many more products than Kroger.

Copying that entire business model is beyond Kroger’s reach. That makes its current price-cutting plan dangerous. A short-term reset may help Kroger win back some shoppers. But a long price war would force Kroger to trade margin for traffic.

Investors should watch Kroger’s returns more closely than its sales. Higher revenue doesn’t help if each product brings in less profit.

Kroger is trying to outdo a retailer 15 times its size. That strategy may protect Kroger’s market share in grocery retail, but it leaves little room for shareholder value.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research