This indicator has reached all-time highs and provides businesses with much needed support

Historically, credit is the catalyst for economic cycles, both good and bad. A recession, outside of the current one, historically is caused by a lack of credit leading to credit, and therefore productivity destruction. As such, investors must pay attention to the credit markets, especially during times of uncertainty.

This credit market signal is a great proxy for corporate credit growth trends. It can help investors understand if credit is available or not. And right now, it is pointing to credit being very available.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

Credit is the lifeblood of the economy. It is necessary for companies to be able to accelerate investments when opportunity presents itself.

Another important aspect of credit is the freedom it gives companies to refinance or borrow. Without access to credit, companies need to make tough decisions on asset allocation, and can seize up and default, destroying productive capacity. This could lead to an economic contraction.

The adverse effects a lack of credit can have on the economy is why it is necessary to follow commercial and industrial (C&I) loan growth trends. It allows investors to understand the direction of bank’s borrowing trends, as opposed to corporations borrowing in the market by issuing bonds.

Like the economy as a whole, C&I loans tend to improve for long periods and decline for short, but dramatic bouts. Loan growth is usually in line with economic growth because it is fueling that growth.

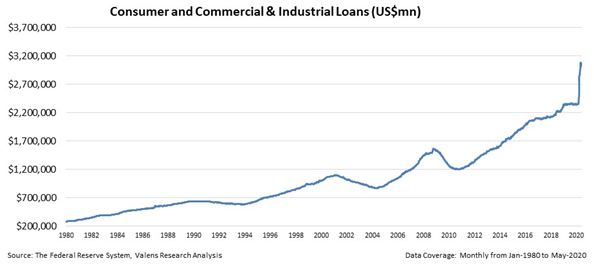

The chart below shows C&I loans from 1980 to the end of 2019. It reached short-term peaks in 1990, 2001, and 2008. All these years line up with economic troubles.

In the early 1990s, the economy entered a recession as inflation rose due to continual increases in the Federal Funds rate. This, coupled with the 1990 oil price shock, sent the economy into a short recession.

The early 2000s also saw a recession due to the technology bubble in the stock market and in telecom debt driven spending, and then the 9/11 terrorist attacks. Finally, 2008 saw one of the worst recessions in American history due to the mortgage crisis and the popping of the housing bubble.

In the current environment, the commercial and industrial loan chart is continuing to rise to new highs. Borrowers were able to access a massive influx of money made available since the pandemic struck, as central banks and governments everywhere understood the importance of flooding the economy with liquidity to prevent a credit crunch. It has increased by nearly 25% in only a matter of months.

When the coronavirus began, the fear was companies would not have enough cash to survive. Companies undergoing a demand shock would default due to their lack of cash. Economists and investors alike feared consumers would hoard savings and many businesses would see huge losses in revenue.

This has happened to some extent, but businesses will be able to survive the short-term loss in revenue as companies have secured easy access to credit.

As the chart above shows, credit has been relatively easy to find. PPP, Main Street lending, and bank lending commitments under revolvers and relationship lending have been able to keep companies afloat.

Companies have borrowed significantly, and importantly for the economy, firms have the ability to borrow aggressively to survive. It’s why there hasn’t been broader waves of defaults so far.

This may have negative effects for companies three to five years from now, when these businesses need to refinance. But it is also a necessary step for companies to survive right now.

As long as companies can borrow enough to not default, firms should be able to make it past this short-term drop in demand. Then the hope is cash flows begin to increase and companies can refocus their borrowing on growing and managing refinancing.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research