This oil major quashed rumors of a possible takeover of its rival

Acquisition is always seen as a possibility especially when a company is facing continuous dips in valuation and skepticism from the market.

This is exactly what happened last week when rumors of a potential takeover of BP (LSE: BP) by Shell (LSE: SHEL) came to light.

Multiple outlets reported last week that Shell held early-stage talks to acquire BP.

In response, Shell quashed those rumors, indicating that it was now bound by UK takeover rules, preventing it from making an offer for its rival in the next six months.

Even though Shell has denied the takeover rumor, investors will be watching closely to see if another takeover deal for BP will materialize.

Investor Essentials Daily:

Wednesday News-based Update

Powered by Valens Research

The oil and gas sector has undergone significant changes in recent years.

Geopolitical tensions and rising environmental concerns have all contributed to volatility in commodity prices and shifts long-term demand trends.

Amidst this volatility, oil majors like BP (LSE:BP) and Shell (LSE:BP) have made strategic moves to adapt to shifting market trends.

Just last week, it was reported that Shell was in early talks to acquire BP, catching the attention of the market.

A potential merger between the two would likely lead to what would be considered as the largest oil deal in decades.

However, Shell dismissed those rumors, issuing a statement declaring that it has no intention of making an offer for BP.

As a result of releasing this statement, Shell can no longer make an offer for BP for the next six months except in certain circumstances, in compliance with UK regulations.

Shell, one of the world’s oil majors, specializes in exploration, production, refining, and marketing of oil and natural gas.

Over the past few years, the company has attempted to streamline its operations by selling its Energy and Chemicals Park in Singapore to the Chandra Asri Group in 2024 and its Nigeria operations to Renaissance in March.

It has also bolstered its liquefied natural gas (LNG) portfolio with its acquisition of Pavilion Energy in April.

Aside from these strategic moves, Shell recently announced another $3.5 billion share buyback program, giving it more money to invest in its operations.

BP is also one of the world’s largest O&G companies. However, the company has been facing market skepticism for the past few years.

This is due in part to a series of corporate mishaps and a less-than-stellar strategic shift to renewables.

BP is attempting to turn things around by divesting from non-core businesses, exploring a potential sale of its lubricant business in Castrol, and scaling back its investments in renewables and ramping up its oil and gas production.

At first glance, the acquisition of BP would turn Shell into a behemoth that can compete against the likes of rivals Exxon Mobil and Chevron.

However, beneath this strategic appeal lies a question of upside.

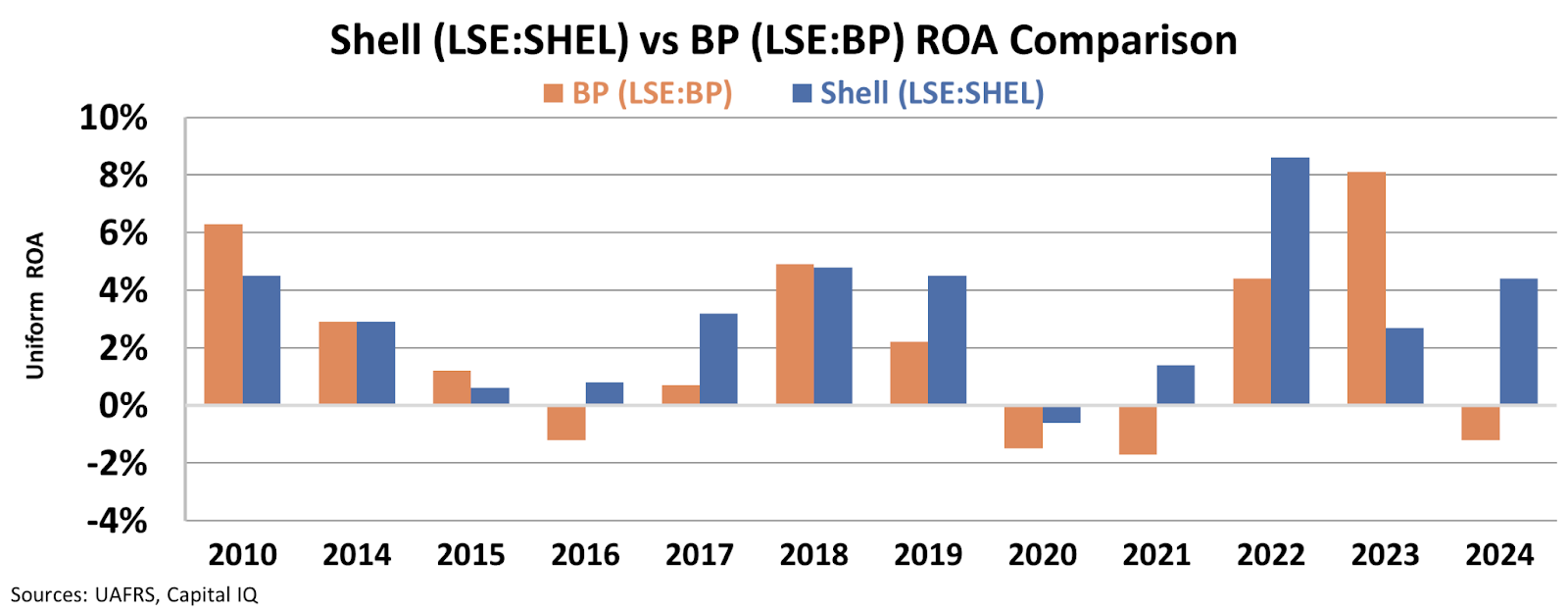

Since 2019 with the exception of 2023, Shell has consistently outperformed BP on a Uniform return on assets “ROA” basis.

Even though Shell has better returns and stands to gain from acquiring its cross-town rival, there are some significant downsides.

It would have to deal with overlapping business units, a larger workforce, and political and legal repercussions that come with a merger of this size. BP also has a debt load of around $27 billion and an additional $38 billion in liabilities.

While a deal for BP could be transformational for Shell, the caveats that come with it are just too big to ignore.

Also, this acquisition could negatively impact a company that’s already on solid footing.

Additionally, Shell might see some potential headwinds.

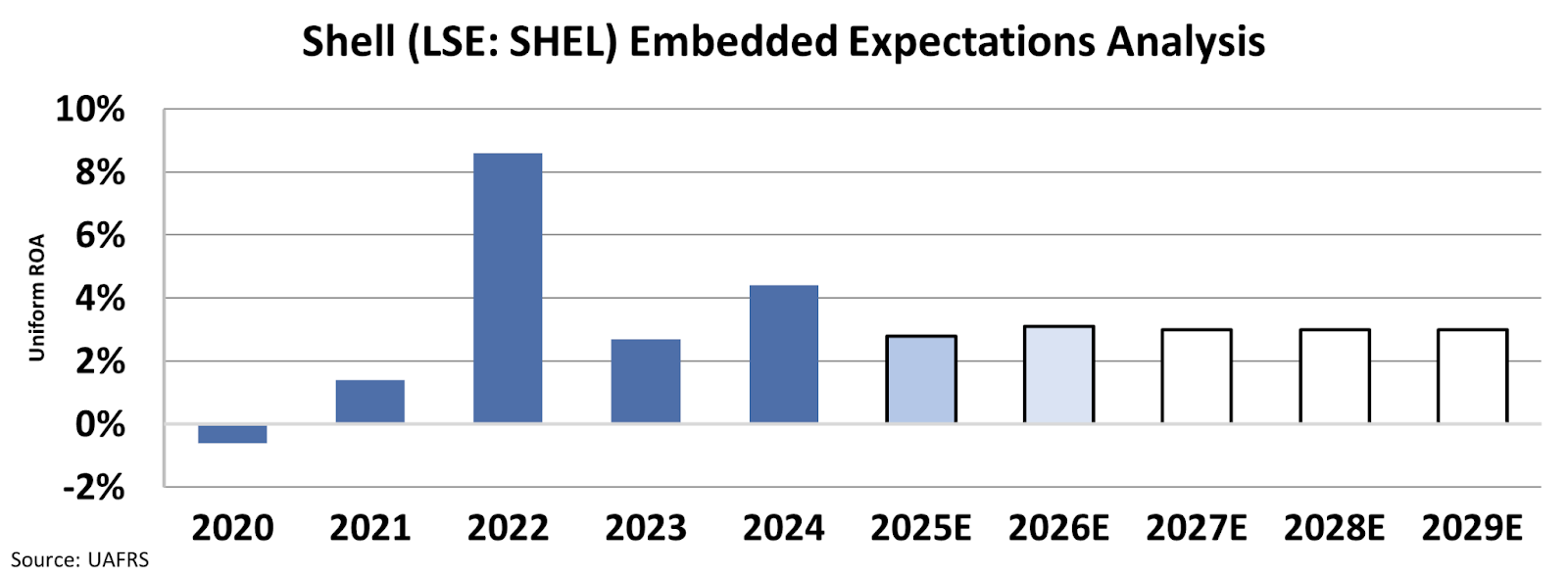

We can see what the market thinks through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the m moarket predicts that Shell’s Uniform ROA will decline to around 3% from 5% last year.

If Shell explores the acquisition of BP once the six-month acquisition ban has lapsed, it risks putting itself in a complicated situation.

Aside from the downsides we mentioned above, the company would likely need to pay a premium to acquire BP.

While this acquisition would be transformational for Shell in terms of oil and gas production and a broader share of the LNG market, it could likely negatively impact the value and returns investors have come to expect from the company.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research