This PC manufacturer continues to thrive amid AI-driven shortages

The AI boom has ushered in demand for advanced semiconductor chips and components like storage and memory modules.

White this has benefitted semiconductor firms, this trend has negatively impacted the PC market. With memory prices skyrocketing, the cost of PCs have risen, with shipping expected to go down as a result.

That said, PC manufacturing giant HP (HPQ) has managed to weather these supply shortages, delivering a Uniform ROA of 36% last year.

However, despite its above-average performer status, the company currently trades at a below-average P/E of 6x.

Investor Essentials Daily:

Tuesday News-based Update

Powered by Valens Research

The AI boom has been a boon for multiple firms across the tech industry.

For instance, designers of advanced chips like Nvidia (NVDA) and AMD (AMD) have seen immense growth by engineering the chips needed by AI hyperscalers like Microsoft (MSFT), Amazon (AMZN), Meta (META), and others.

Meanwhile, the rapid infrastructure build-out for AI data centers have benefitted the likes of Seagate (STX) and SK Hynix due to enormous hyperscale demand for storage, DRAM, and HBM chips.

Skyrocketing demand for these components have led to shortages and higher prices, proving beneficial for the suppliers of AI hardware.

That said, this trend has also affected the personal computer (“PC”) market. The PC segment has seen decades of continuing price declines as technology and production advanced rapidly.

However, the AI boom’s insatiable demand for storage and memory modules has bucked that trend. According to industry reports, PC vendors have already announced price adjustments of roughly 15%.

Global PC shipments are likewise forecasted to drop by roughly 11% for 2026.

That said, PC giant HP (HPQ) has managed to weather these component shortages and has even positioned itself to take advantage of AI hardware demand.

HP is one of the world’s largest PC hardware manufacturers, selling laptops, desktops, printers, and other peripherals for both consumer and enterprise customers.

The company uses a “razor-and-blade” model, generating revenue through one-off sales of PC and equipment alongside a recurring revenue stream through the sale of add-on hardware, accessories, and subscription-based ink supply services for its computers and printers.

HP has recently added AI PCs to its product portfolio. These devices are designed specifically for workloads that leverage AI features, with some even capable of running LLMs locally.

Since these are highly specialized hardware, the company is able to command a pricing premium, with AI-ready PCs costing between $200 to $500 more on average.

HP delivered a revenue of $14.4 billion in Q2 2026, with 54% generated by Personal Systems (Commercial) and followed by Printing Supplies and Personal Systems (Consumer) at 19% and 17%, respectively.

The rest of the company’s quarterly revenue was drawn from the consumer and commercial segments of its Printing business unit.

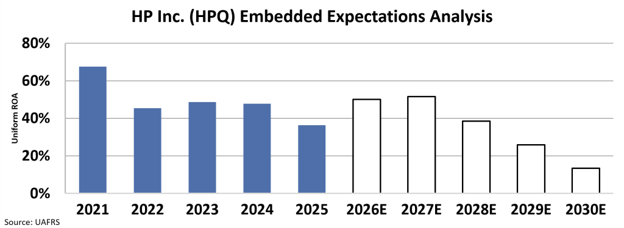

HP has delivered above-average returns as well. Last year, it delivered a Uniform return on assets (“ROA”) of 36% alongside asset growth of 8%.

Despite its strong performance, HP currently trades at a 6x Uniform P/E, well below the 25x corporate average.

At this valuation, investors expect HP’s Uniform ROA to drop steeply to 13% by 2030, well below the returns the company has generated over the past few years.

This valuation signals market concerns about the cyclicality of PC demand. It also shows investors are concerned about cost pressures due to elevated storage and memory module prices.

However, HP’s recurring supplies revenue, continued commercial demand, and AI hardware could support stable returns for years to come and amid AI-driven shortages.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research