This popular credit marker consistently gives investors the wrong signals

To understand the equity markets, investors must have a solid grasp of what is occurring in the credit markets. Many investors turn to credit default swaps (CDS) as a solid indicator of credit health in the market.

When the credit markets displayed scary signals in March 2020, investors were seemingly left with no choice but to panic. In reality, these individuals were looking at the wrong data. Their panic was unwarranted.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

GameStop (GME) has been a sensation the last few weeks. It was the biggest headline, but it was not the only stock in focus over the last two weeks. AMC Entertainment’s (AMC) stock also participated in a big way.

AMC Entertainment’s stock rocketed over 200% the last week of January as the company announced it was successfully able to raise over $900 million. This new debt issuance is serving the firm as a cash cushion.

Before it got the placement, there were real conversations about the company going bankrupt. Now, those issues are entirely off the table in the near-term, and that is what caused the stock to take off.

This surge is an example that shows how equity and credit markets are trading ‘wide open’ at the moment. As companies are able to refinance and borrow money to reduce the risk of default, the picture for a company can change overnight. This was the catalyst for the AMC Entertainment short squeeze.

To understand the equity markets, investors must have a solid grasp of what is occurring in the credit markets.

Historically, the catalyst for a recession has been the lack of credit. When companies or individuals can no longer finance their debt, they are forced into bankruptcy.

When waves of bankruptcies happen, the bankrupt have to focus on cleaning up their balance sheets as opposed to growing, and so demand declines, leading to a spiral of declining economic activity.

One part of understanding the credit risk comes from the Credit Default Swap (CDS) markets.

The potential risk of a default wave this past March was confirmed to be low by Valens’ data through the entire crash. However, individuals were panicked at the onset of the pandemic as some credit markets were flashing scary signals.

In 2008, CDS were bought and sold as insurance on underlying bonds. One part of the recession came when mortgage bonds failed, and AIG, who sold this insurance, now was on the hook. Paying attention to CDS is a good indicator of credit health.

A higher CDS, like a higher insurance premium, signals the borrower has a higher credit risk and is a bigger risk to default. A lower CDS means the opposite.

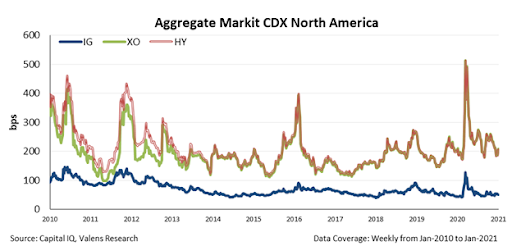

Markit CDX is a popular index tracking credit default swap baskets.

Markit saw its high yield index rise to levels in March people have not seen since the Great Recession. With these scary signals, people panicked that companies would be going under.

However, this spike in default risk was only a mirage from the wrong data.

What the people who panicked did not capture was how these indices are incomplete. They only represent a small subset of the market. The Markit CDX only covers 100 entities that do not all have high yield credit ratings.

This data is taken from a universe of hundreds of thousands of credits and thousands of companies with liquidly traded debt.

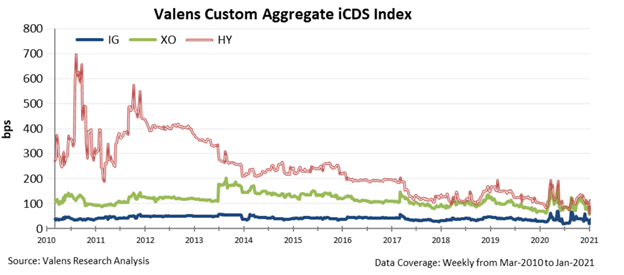

Part of the reason we at Valens told credit investors to hold tight on their investments was because we had better data. We used our own aggregate CDS indices.

We gather this data from a universe of hundreds of thousands of credits and thousands of companies with liquidly traded debt.

Through our CDS indices, we are able to analyze and base our decisions on real data.

Additionally, the indices we use are much more complete in the signals they offer. They attempt to capture all U.S. companies with liquidly traded CDS.

Our indices showed that while the CDS spiked wider in March, they never reached previous levels seen in 2010 and 2013. Furthermore, these levels were far from the ones witnessed in the real panic times of 2008.

As you can see in the below chart, the tick up in March was much less severe than the ones represented in Markit CDX.

Since Valens could identify this discrepancy in the market, we knew a full-blown recession was unlikely, especially after the government injected its stimulus.

With the wrong data, it is no wonder investors panicked.

Right now, the same data shows we are at historically low levels of credit risk.

With a low cost to borrow, companies can refinance their debt. This means that the risk of default for these firms is low. Just one example is a distressed firm like AMC easily accessing the credit market to refinance.

Under these market conditions, the market is currently secure from any long-term tremors. As much as the headlines try to tell investors otherwise, the next Great Recession isn’t looming around the corner.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research