This popular diner is going private in a deal valued at over $600 million

2025 has been a rough year for restaurant operators as rising food and labor costs, inflation, and tariffs have squeezed razor-thin margins.

As a result, costs have been passed on to consumers, and while this has kept operators afloat, this has forced price-conscious customers to either look for alternatives or refrain from dining outside altogether.

Denny’s (DENN), a popular diner-style restaurant chain hasn’t been immune to these industry-wide headwinds as it has struggled to attract customers to its locations, leading to multiple store closures.

After years of struggles, the company went private in a deal valued at around $620 million earlier this week.

While there’s no doubt that Denny’s has struggled, its ability to generate returns hasn’t deteriorated nearly as much as the rest of the market seems to believe. Due to this, it’s become a prime target for PE firms eager to acquire public companies ripe for the taking.

Investor Essentials Daily:

Thursday News-based Update

Powered by Valens Research

2025 has been a rough year for restaurant operators as food and labor costs continue to rise. To make things worse, inflation and tariffs have further compressed already-shrinking margins.

As a result, operators have had to pass on costs to consumers, and while this has helped keep them afloat, these price hikes are forcing diners to either look for alternatives or refrain from dining outside altogether.

Denny’s (DENN), a 72-year-old diner-style restaurant chain hasn’t been immune to these industry-wide headwinds. It has struggled to attract cash-strapped customers to dine at its locations, known for operating 24 hours a day.

However, its struggles aren’t new.

Denny’s problems started during the pandemic, as lockdowns forced it to scale back the round-the-clock operations of its diners. And since 2021, around a quarter of its 1,600 locations have not resumed its pre-pandemic store hours. Moreover, the company closed around 180 stores since the beginning of last year as it attempted to control costs and prioritize its most profitable franchises.

Meanwhile revenue has averaged just $457 million over the past three years, below the company’s $567 million average in the three years leading up to the pandemic.

Amid this turbulence, Denny’s stock fell more than 70% from the start of 2021 through the end of October this year.

And as its stock price has declined, Denny’s emerged as a prime target for a private equity (“PE”) takeover. The company still operates one of the largest diner chains in the U.S., with a strong brand value.

Given this brand and asset base, TriArtisan Capital Advisors (owner of TGI Friday’s and P.F. Chang’s) elected to acquire Denny’s for roughly $620 million, which it announced on November 4.

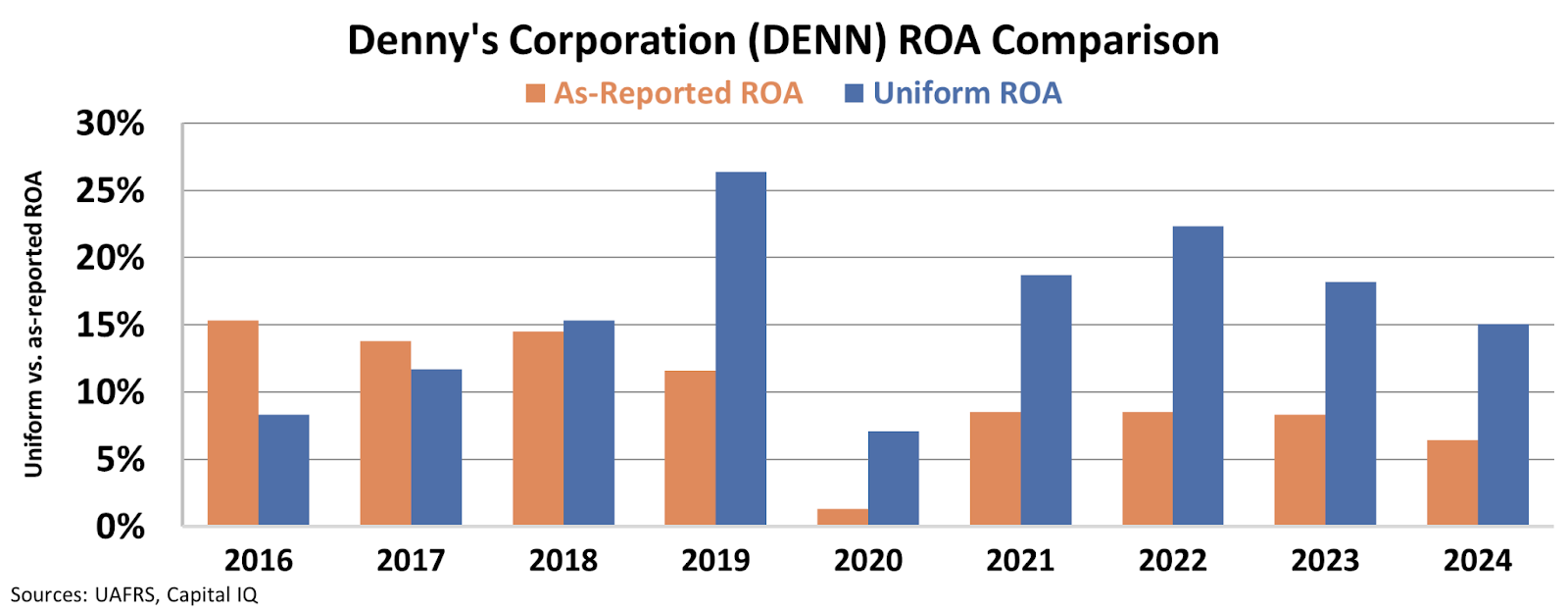

At first, some investors may doubt TriArtisan’s decision to acquire the struggling restaurant chain. Since 2016, the company’s as-reported return on assets (“ROA”) has declined from 15% to just 6% in 2024.

However Uniform Accounting paints a more attractive picture for Denny’s. The company’s Uniform ROA rose dramatically from 8% in 2016 to 26% in 2019. After weathering pandemic struggles in 2020, ROA rebounded to 22% by 2022.

While returns have fallen since 2022, Denny’s was still able to generate 15% returns in 2024, higher than both the 12% corporate average and the company’s pre-2018 profitability.

Despite recent turbulence, Denny’s is still a recognizable brand whose returns are still higher today than it was in the years prior to 2018. The rest of the market underestimated this company’s profitability, giving TriArtisan the opportunity to acquire it at a favorable price.

This same principle applies to individual investors. Uniform Accounting can reveal undervalued companies that the rest of the market is overly pessimistic toward, presenting opportunities for investors to capitalize.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research