This power-management firm is critical to grid modernization

Demand for grid modernization and added capacity is reaching new highs due to soaring demand for power from both residential and hyperscale data center customers.

For example, PJM Interconnection, the firm responsible for managing the Mid-Atlantic and Midwest’s electric grid has come under severe strain due to high energy demand.

With grid modernization and capacity addition seeing heightened prioritization, Eaton (ETN), one of the biggest power-management companies in the world is positioned to play a key role.

Eaton’s returns have steadily risen over the years due to its growing role in the energy bottleneck. As a result, investors have heightened their expectations for the firm.

Investor Essentials Daily:

Thursday News-based Update

Powered by Valens Research

PJM Interconnection has spent the past decades managing the electric grid in the region it operates in.

In the region managed by PJM Interconnection (the Mid-Atlantic and Midwest), new data centers are piling into a power system already responsible for keeping electricity flowing. It services roughly 67 million people across 13 states.

The strain has become severe enough that regulators have scheduled a July meeting to discuss solutions. Some officials have suggested breaking PJM into smaller pieces that are easier to manage.

It’s no secret that cost pressures are mounting. Wholesale power on PJM’s grid averaged $136.53 per megawatt-hour in the first quarter, up 75% from $77.78 a year earlier.

Congestion costs—fees utilities pay when the grid can’t move power fast enough to meet demand—climbed 300% to $2.02 billion.

Data-center demand included in PJM’s last two capacity auctions (where utilities bid to commit to having a certain amount of power ready during peak demand hours) added $13.8 billion to customer bills.

PJM’s situation highlights the problems with moving power through an aging network.

In short, the grid is past its limits. PJM’s transmission infrastructure has an average age of over 40 years old.

It wasn’t built for today’s high levels of demand. And it’s not alone. 70% of transmission lines and large power transformers nationwide are more than 25 years old.

Furthermore, the grid-modernization bottleneck is causing plenty of problems for the data-center market.

And this setup creates an opportunity for Eaton (ETN).

Eaton is one of the biggest power-management companies in the world. It helps operators manage power coming from the grid.

The company offers tools like uninterruptible power supplies, battery storage, and even microgrids—which provide backup power that works off the grid.

Eaton provides equipment used by utilities and data centers alike. So regardless of whether parts of a grid are being replaced or expanded, the company’s transformers and monitors are needed.

Those might look like simply pieces of equipment, but supply is hard to come by at present, making Eaton a pivotal player in grid modernization.

Last October, Eaton said it had started production at its newly expanded Texas manufacturing facility. The $100 million project more than doubled its U.S. production capacity for voltage regulators and three-phase transformers.

Utilities rely on both of these products to stabilize and expand the grid. And that’s just the tip of the iceberg. Eaton has invested more than $1 billion to support grid expansion since 2023.

Whether PJM fractures or holds together, every operator in every territory still needs Eaton’s gear to keep the lights on.

This business has spent years making sure it’s prepared for a surge in demand, and the markets are catching on.

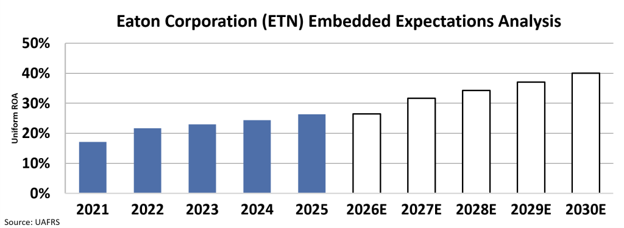

We can see this through Valens’ Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

Eaton’s Uniform return on assets (“ROA”) has risen for five straight years, from 17% in 2021 to 26% in 2025. Investors expect that rise to continue, with Uniform ROA expected to reach 40% by 2030.

Eaton is positioning itself as a key player in solving the energy bottleneck. It’s adding capacity to a market where utility planners and hyperscale data centers are all demanding upgrades.

We’re on the brink of a scramble to connect new power and modernize old infrastructure. And the companies that make essential grid equipment hold the solutions to that problem. This equipment will keep data centers running without bankrupting American households.

Eaton is already preparing for that future. As we mentioned, it has piled more than $1 billion into North American capacity since 2023.

The market expects a lot out of this company today. However it is well positioned to meet, if not exceed these targets in the coming years.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research