This powerful management sentiment indicator gives us reason to be excited about the economic recovery once the pandemic recedes

Every quarter, executive management teams get onto a large conference call and deliver their earnings results to thousands of Wall Street analysts and investors.

It can be tough to decipher when management teams mean what they’re saying versus when they’re trying to downplay certain concerns.

We’ve developed a tool to help us decipher what’s actually going on during quarterly earnings calls. Before the pandemic struck, it was giving bullish signals that may mean corporations could recover faster than investors anticipate once the pandemic recedes.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

Unless you’re an expert interrogator, you probably haven’t been trained to pick up on the subconscious cues we all give off when we’re speaking. But reality is, we are all great lie detectors.

Over the course of a speech, the human voice tends to fluctuate ever so slightly based on how much conviction we’re speaking with.

While some of these fluctuations are detectable, like word choice, speed, and pitch, others tend to go unnoticed to the naked ear—changes like breathiness, or more subtle ‘micro’ changes to pitch and speed.

While these cues are hard to pick up on, they’re also tough to mitigate.

Much to the chagrin of management teams around the world, it’s nearly impossible to train yourself away from all these fluctuations.

These almost microscopic cues can tell you just as much about someone’s speech as the words alone. They can give us information about when a CEO is speaking with conviction versus when he or she appears unsure about their words.

As an investor, this is all valuable information.

At Valens, in addition to the Uniform Accounting that represents the foundation of our analysis, we’ve also developed a tool to help us analyze management conviction on earnings calls.

We call the analysis that comes out of the tool “Earnings Call Forensics.”

Using a framework that we’ve developed for over a decade, we’re able to pick up on subtle cues from earnings calls as a form of “forensic fact checking.”

The framework allows us to point out when management appears to be speaking with confidence, excitement, and conviction, and it also lets us see when management’s cues generate questionable markers.

Generally speaking, we pay more attention to signs of conviction because they only mean one thing—management is confident about that topic.

Conversely, questionable markers don’t directly translate to lies as if it were a truth detector. Instead, questionable markers can mean management wasn’t prepared for a question, they forgot a fact or figure, or they’re fundamentally concerned about the topic they’re speaking on.

In any event, we currently process more than 500 earnings calls per quarter, which gives us a good sample size to apply our learnings for macro analysis, too.

By looking at Earnings Call Forensics in aggregate, we can both see how confident management teams are overall and what, specifically, management teams are confident and concerned about.

For example, if several management teams in the same industry generate questionable markers about their margins, it could be an indicator that the industry is due to face expense pressures in the coming quarters.

On the other hand, widespread confidence markers about growth could be a sign that we should expect high levels of reinvestment.

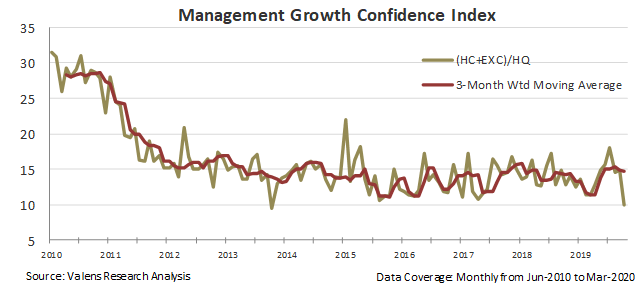

We can assess the overall ratio between confidence and questionable markers to get a sense for how confident management teams are in the current economy.

For the last several years, the ratio has ranged between 1.2 and 1.7 confident markers for every 10 questionable markers, and even as recent as February, that remains towards the higher end of the range.

Midway through 2019, management teams began to generate more questionable markers about global trade and political issues. But even through the first two months of 2020, we saw that trend reverse.

That is incredibly bullish. While the ratio of confidence to questionable markers in March dropped, that’s to be anticipated considering the disruptions in the market. But before the pandemic required us to shut down the economy, management teams were excited to invest.

We also have the ability to break up the analysis by sector, which will be important to monitor over the next few months, specifically for transportation, financials, and energy.

We will be closely monitoring Earnings Call Forensics aggregates as more data comes in. But the confidence management teams showed before the virus struck is a positive signal that management teams might be more likely than normal to be excited to invest as we come out of this virus-induced recession.

All the best, as always

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research