This pure-play autonomous vehicle firm has yet to prove its profitability

The autonomous vehicle space has seen rising competition in recent years as companies seek to scale in a market that’s expected to grow to $2.2 trillion by 2030.

Aurora Innovation (AUR), a pure-play self-driving tech provider is attempting to secure a place in the autonomous vehicle space by targeting the trucking industry. The company recently crossed a major milestone last year when it launched its first driverless commercial operations.

By introducing autonomous driving tech in an industry wracked by labor shortages, Aurora has the makings of a potential winner. However, hype has yet to turn into reality for this company.

Investor Essentials Daily:

Friday News-based Update

Powered by Valens Research

The autonomous vehicle (“AV”) space has seen rising competition in recent years as companies race to scale their operations and capabilities in this market which is expected to grow to $2.2 trillion by 2030.

Waymo, Alphabet’s (GOOGL) self-driving unit, along with Tesla (TSLA) and other players, have spent the past few years developing their technology to make the transportation of passengers between destinations possible.

With self-driving tech rapidly improving, ride-hailing giants Uber (UBER) and Lyft (LYFT) have jumped on this innovative trend by partnering with AV manufacturers to power their autonomous driving offerings.

According to reports, over 450,000 commercial AV rides are booked weekly and this number is expected to grow further as self-driving technology continues to improve.

However, the use of AV technology isn’t just limited to passenger transport. Aurora Innovation (AUR) is attempting to bring this technology to the U.S. trucking industry which generates over $800 billion in revenue.

Aurora is a pure-play AV technology provider that went public in 2021 through a merger with a special purpose acquisition company (“SPAC”).

Instead of manufacturing its own AVs, the company designs and sells AV tech that’s meant to be used in freight trucks.

Aurora is setting itself apart in the EV space by targeting trucking—an industry highly vulnerable to labor shortages and brain drain. As of 2025, the driver shortfall is estimated between 60,000 and 80,000.

Since road freight amounts to roughly 70% of all U.S. cargo, insufficient manpower could lead to significant supply chain disruptions if left unaddressed.

The company currently operates in a Transportation-as-a-Service (“TAAS”) model where it provides full driverless freight service to customers. Aurora Driver, the firm’s flagship offering was formally launched under this model.

However, Aurora plans to shift to a Driver-as-a-Service (“DAAS”) model in 2027, where it would provide self-driving tech to fleet owners instead, enabling it to transfer asset ownership to customers.

Aurora has a sizable partnership network spanning original equipment manufacturers (“OEMs”) like Toyota and Volvo, hardware partners such as Aumovio and Nvidia (NVDA), and logistics firms such as FedEx, Schneider, Uber Freight, and others.

The company achieved a crucial milestone in April 2025 when it launched its first driverless commercial freight operations. In Q4 last year, it expanded driverless operation to 10 trucks

2026 will also mark a crucial year for Aurora, as it plans to launch the next iteration of its commercial hardware kits for a new fleet of driverless trucks and close the year out with over 200 driverless trucks in operation without observers. A revenue run-rate of $80 million is also expected.

Aurora’s self-driving tech, DaaS model, and targeting of a niche market (at present, Uber Freight is its only major competitor) in the expanding AV space position it as a high-potential company, bringing significant market interest and lofty expectations.

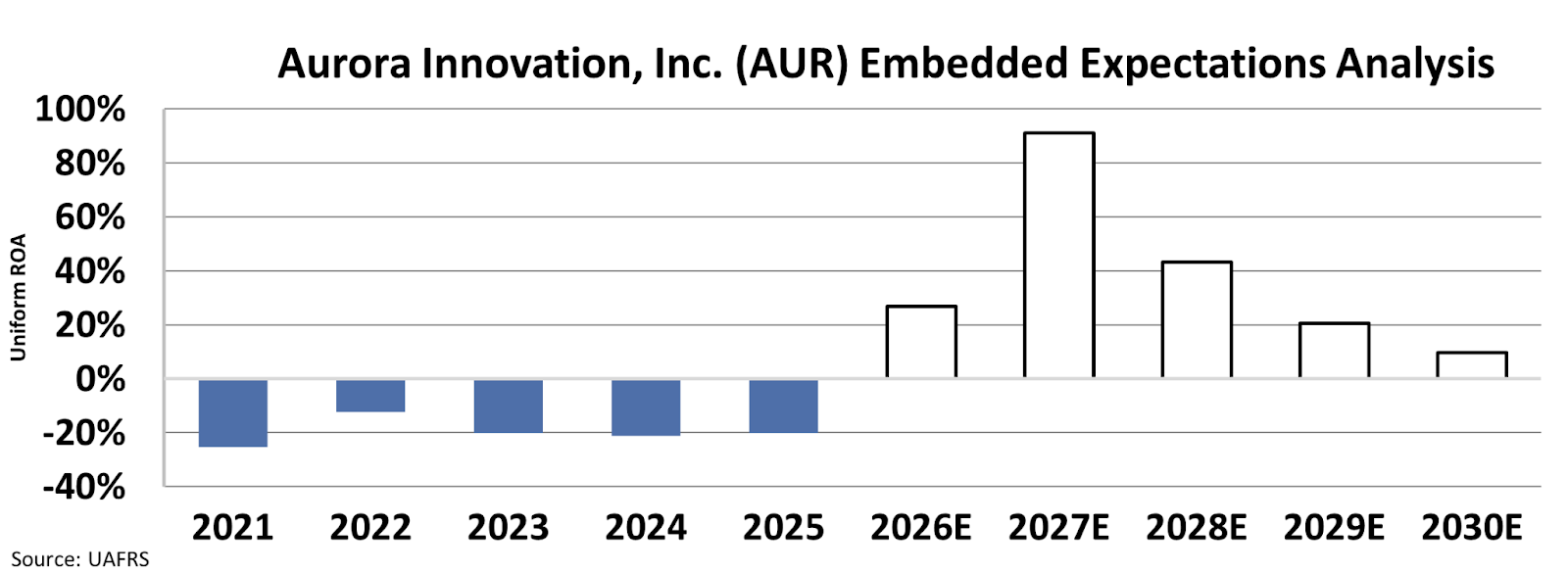

Since going public in 2021, Aurora has delivered negative returns. However, investors are betting that the firm’s Uniform return on assets will climb to 10% by 2030.

Reaching 10% returns after consistently delivering negative returns in an emerging market is a tall order, even for a firm with massive potential on paper.

While there’s no doubt that Aurora’s AV tech and business model hold promise, the stark reality is that it has burned through millions of capital with only a few million in revenue to show for it. The company posted a net loss of $816 million against a revenue of just $3 million last year.

The AV industry is still in its infancy, making it extremely difficult to separate the true winners of the space from the losers.

That’s why until Aurora can demonstrate its ability to generate positive returns, lower losses, and sustain profits, it may be best for investors to stay away from the company.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research