This retail giant might overpay for its next acquisition

QXO (QXO) surprised the market with an unsolicited $5 billion all-cash bid for GMS (GMS), prompting Home Depot (HD) to counter as part of its Pro division expansion.

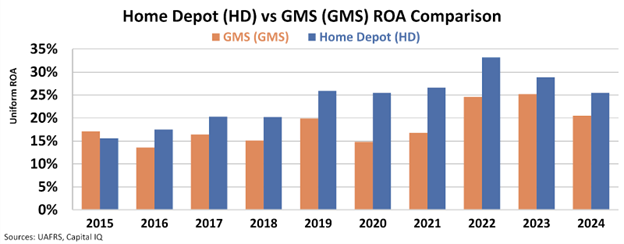

Home Depot has delivered north of 24% ROA since 2019, while GMS has averaged about 20% and is expected to fall toward 10% over the next five years.

Paying a steep premium to outbid QXO could dilute the very profitability that fuels Home Depot’s valuation. Investors will be watching closely to see if another large deal stretches the company’s margins too far.

Investor Essentials Daily:

Thursday News-based Update

Powered by Valens Research

Yesterday, we discussed rumored discussions around Apple’s potential acquisition of Perplexity AI as a means to catch up in the race for advanced search and generative AI.

Today, we’re discussing another potential deal that already has a full-blown bidding contest for GMS (GMS), the U.S. building-products distributor known for drywall, ceilings, steel framing and gypsum.

Last week, QXO (QXO) surprised the market with an unsolicited all-cash proposal valuing GMS at roughly $5 billion, or $95.20 per share including debt.

That move prompted Home Depot (HD) to step in, lodging its own bid. It sees GMS as a strategic fit for its Pro division.

Home Depot has been deliberate about growing its footprint in the professional contractor space.

Earlier this year, it closed on SRS for $18 billion, a deal meant to deepen its reach into complex project segments and edge closer to an estimated $1 trillion total addressable market.

The GMS acquisition would link with that strategy, folding a specialist distributor into Home Depot’s distribution network.

Yet beneath the strategic appeal lies a question of profitability impact.

Since 2019, Home Depot has generated north of 24% Uniform returns on assets ‘’ROA’’ every year.

That consistency has supported its valuation premium and given shareholders confidence in its ability to integrate acquisitions without sacrificing margins.

GMS, by contrast, has averaged around 20% returns over the same period.

While still healthy by industry standards, that gap is significant when applied to a multibillion-dollar purchase.

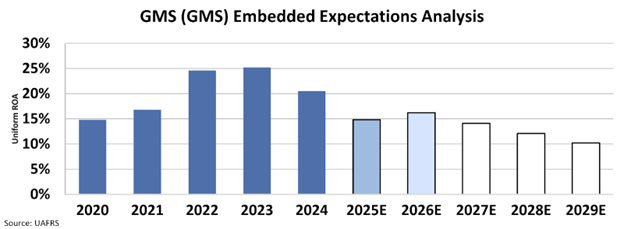

Furthermore, the market also expects GMS’ profitability to drop significantly in the next five years.

We can see what the market thinks through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market predicts that the company’s Uniform ROA will decline to around 10% from 20% last year.

If Home Depot pays a premium far above market value to outbid QXO, it risks diluting the very profitability that has fueled its growth.

QXO has signaled readiness to wage a hostile campaign if its shareholder offer is rebuffed. GMS shares jumped more than 30% on the news, reflecting both the premium price and the competing bids that could drive the final deal higher.

While GMS would fit neatly into Home Depot’s Pro expansion playbook, markets will be watching the size and price of further acquisitions.

After SRS, another large deal could invite scrutiny over whether Home Depot is overreaching in its effort to consolidate a fragmented construction and tools market.

Any misstep could erode the around 25% returns investors have come to expect.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research