This streaming giant has been overlooked by investors relying on as-reported financials

Streaming services are no longer just an add-on to the American viewing experience—it is now the primary entertainment option for most, if not all, of Americans.

A decade ago, the average household only had one streaming subscription. Now, that number has ballooned to more than four.

With streaming services achieving universal adoption, companies are raising prices in a race towards profitability.

And in this race, none have succeeded more than Netflix (NFLX), the current market leader which enjoys both a massive subscriber base and pricing power.

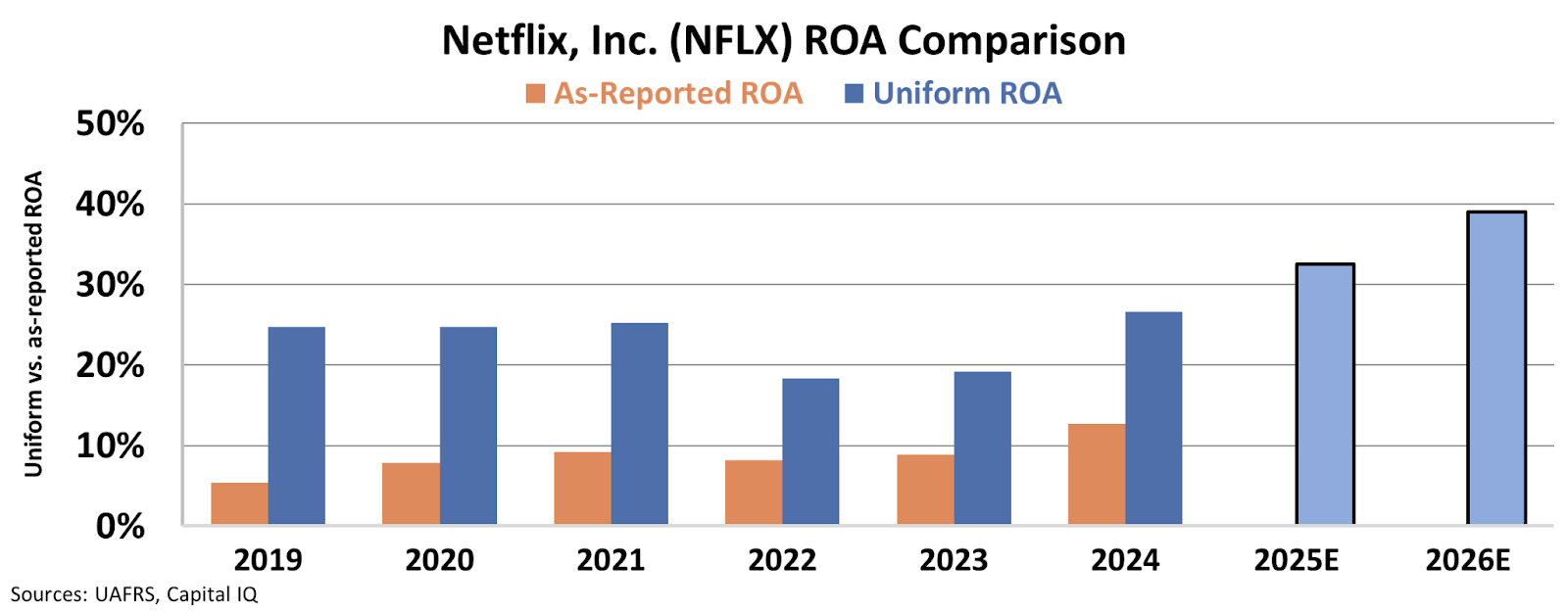

Yet despite averaging returns of 20%+ from 2019 to 2024, investors relying on as-reported financials have missed just how profitable this company is.

Investor Essentials Daily:

Friday News-based Update

Powered by Valens Research

Streaming services are no longer just an addition to an existing legacy cable subscription—it is now the primary entertainment option for millions of consumers.

Ten years ago, the average household subscribed to only one streaming service. Fast forward to now, that number has gone up to over four, as a glut of options have flooded the market. Back then, Netflix (NFLX) was the primary provider customers flocked to.

But now, media conglomerates such as Paramount Skydance (PSKY), Disney (DIS), and Warner Bros. Discovery (WBD) are competing against Netflix and trying to chip away at its dominance.

With streaming services becoming more ubiquitous, companies are raising prices in a race towards profitability.

For instance, HBO Max’s prices are up 23% since 2019. Meanwhile, Disney-owned Hulu and Disney+ prices are up 58% and 172%, respectively. Netflix, the current leader in streaming, has raised its prices 38% since 2019.

While Netflix’s rivals are attempting to close the gap (Paramount Skydance for example, is trying to acquire Warner Bros. Discovery), none of them have come close to doing so, especially in terms of higher pricing power and chasing profitability.

Price hikes tend to lead to subscription cancellations, but Netflix has managed to retain customers, with cancellation rates averaging at only 2% since May 2023.

Analysts say the company has done this through a combination of offering least expensive subscription tiers, ranging from $7.99 to $17.99, alongside a premium option at $24.99, which also happens to be the most expensive out of all streaming services.

At present, Netflix has the most subscribers in the U.S., with over 67 million. Hulu, Disney+, Paramount+, and HBO Max are trailing by a wide margin, at 39 million, 36.5 million, 34.5 million, and 23.8 million subscribers, respectively.

The combination of a massive subscriber base and pricing power has yielded above-average returns for the company. However, investors, especially those who rely on as-reported numbers, haven’t seen just how profitable it is.

Uniform accounting shows that the company is far more profitable than the rest of the market realizes.

From 2019 to 2024, the average Uniform return on assets (“ROA”) of Netflix have averaged over 20% levels. Wall Street analysts even expect that ROA (represented in light blue bars) will rise to 39% in the next two years.

However, if as-reported numbers were to be followed, the streaming giant’s average returns would only be at 8%, far lower than what Uniform accounting reveals.

Despite being a market-leading giant, as-reported numbers hide just how profitable Netflix is. Investors relying on as-reported financials can still overlook the company because of this distortion.

Uniform accounting reveals how profitable and undervalued Netflix truly is, and how much upside investors relying on faulty financials have missed.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research