Credit and equity investors are at odds over 5G

When it comes to telecommunications companies, everyone’s focus is on the opportunity of 5G infrastructure.

However, the massive capital investment required to implement 5G turns 5G into a massive risk for telecom companies, rather than an opportunity. Despite this, today’s telecom company stands out amongst its peers as the safest credit investment.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

The 5G cellular revolution is coming, and investors are already seeing the dollar signs of faster speeds. Better cellular connection will enable speeds equivalent to home broadband internet but on a cell network.

No one has been more excited about the 5G revolution than the cell providers themselves. Telecommunications companies plan to spend hundreds of billions on both the research & development and the infrastructure needed for 5G.

However, taking a step back we can see this is not an immensely profitable investment for future performance. Telecom companies are not going to be able to charge significantly more for these new 5G services, despite the new services costing many billions to implement.

However, the large provider’s hands are forced by circumstance. The cellular service industry is a mature, slow growth industry, so gaining customers is difficult and requires taking market share from the other major players.

The problem is this creates a race to the bottom, where each major telecom company tries to outspend the others to have the best 5G network, as whoever has the best market will take share.

These two factors make the massive 5G investment almost like maintenance capital expenditure, required just to keep the company going.

Due to this spending, Verizon (VZ) and AT&T (T) shot up to the top of the list of non-bank borrowers earlier this year, and investors have not exactly been thrilled.

Yet, of the three major telecom companies, T-Mobile (TMUS) stands out as a clear credit opportunity. Not only was T-Moblie ahead of the curve on both CapEx and spectrum spending, but it also has the cleanest credit outlook.

Relying on the major Wall Street ratings firms and as-reported financials, investors are led to believe that T-Mobile is a high yield credit.

Here at Valens however, we see things a bit differently.

Our Credit Cash Flow Prime (CCFP) analysis is able to get to the heart of the firm’s true credit risk.

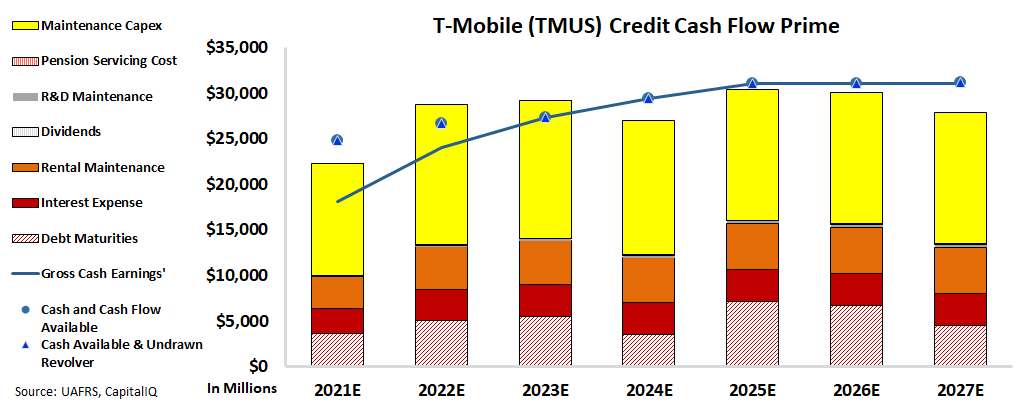

In the chart below, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

Unlike Verizon and AT&T, T-Mobile does not have a dividend commitment, reducing the necessary cash outlays for the company. As a result, T-Mobile’s cash flows and cash on hand just about match and then exceed all obligations, including CapEx and debt maturities in the next few years.

S&P gives the company a BB high yield rating, implying a 10%+ risk of default, which does not make sense given T-Mobile has just enough cash to cover all necessary outlays.

Using the CCFP analysis, Valens rates T-Mobile as an investment grade IG4. This rating corresponds with an expected default rate below 2% within the next five years, a more realistic projection once a holistic understanding of the company’s risk is taken into account.

SUMMARY and T-Mobile US, Inc. Tearsheet

As the Uniform Accounting tearsheet for T-Mobile US, Inc. (TMUS:USA) highlights, the Uniform P/E trades at 43.8x, which is above the global corporate average of 23.7x, but below its own historical average of 29.6x.

High P/Es require high EPS growth to sustain them. That said, in the case of T-Mobile US, Inc., the company has recently shown 85% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, T-Mobile US, Inc.’s Wall Street analyst-driven forecast is a 66% EPS decline in 2021 and 37% EPS growth in 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify T-Mobile US, Inc.’s $144 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 14% annually over the next three years. What Wall Street analysts expect for T-Mobile US, Inc.’s earnings growth is below what the current stock market valuation requires in 2021 but above that requirement in 2022.

Furthermore, the company’s earning power in 2021 is near the long-run corporate average. However, cash flows and cash on hand are in line with its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a low credit and dividend risk.

To conclude, T-Mobile US, Inc.’s Uniform earnings growth is below its peer averages. Also, the company is trading slightly below peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research