Tracing our broken supply chain back to the source

The global supply chain breakdown is a dominant theme throughout the business world right now. We at Valens hear about it constantly on almost every management earnings call. These shortages extend to the key components of the modern economy.

While it’s easy to blame high demand and gummed up supply chains, there is another cause to these shortages, thanks to a once-in-a-lifetime setup in corporate assets.

Today, we will break down how aging assets across the United States are creating bottlenecks, and what that means for investors

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

Lumber, copper, uranium, steel, sugar… There is another commodity shooting up in price.

While silicon is ubiquitous in the natural world, it requires an energy-intensive processing stage for chips. The vast majority of that processing occurs in China, but the Chinese energy crisis has forced officials to ration their energy usage.

As China clamps down on energy-intensive industries, the silicon supply chain is experiencing historically difficult disruptions. This is causing problems for the hundreds of midstream supply chain players that fulfill specialized tasks necessary for the supply chain to function.

Elkem ASA (ELKO.OL), a Norwegian company that manufactures silicon-based materials for the foundry industry, needed to declare force majeure in September, taking legal protection because it can’t deliver the products it had committed to delivering.

The shortage has caused silicon prices to skyrocket 300%, marking another price shockwave and raising production costs for everything downstream.

Silicon is crucial not only for microchips but various alloys in car engines, a component of cement, and the base material for key adhesives in manufacturing.

The key issue isn’t just the direct effect on industries that depend on silicon. The real issue is broader, highlighting an important feature of the economy.

We recognize the importance because it creates an opportunity. These disruptions may weigh on the economy in the near term. However, they can also be a potential longer-term catalyst for growth that vigilant investors can capitalize on…

Silicon, like many other materials, has seen surging industrial demand in recent years. But in the U.S., corporations have been unwilling to invest the capital expenditure dollars (“capex”) needed to increase capacity materially.

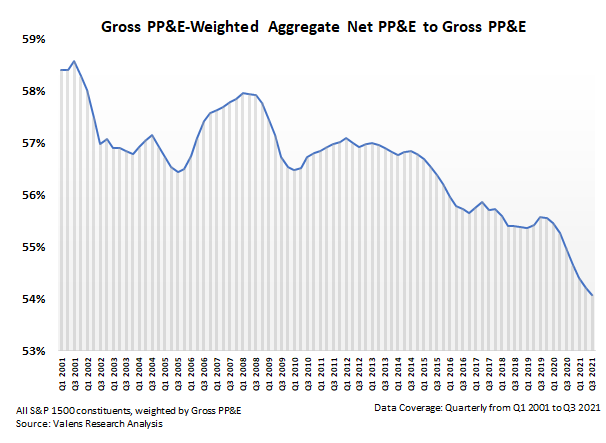

We can see this when we look at Net/Gross PP&E ratios. The chart below shows how old assets are. A lower net/gross PP&E ratio means assets are more heavily depreciated on U.S. corporate balance sheets. This is the accountants’ way of saying that the physical stuff that companies own is older, and right now, it is as old as ever.

This is because U.S. corporations, just like many worldwide, have limited capex investments in the past decade to maximize their cash flows. This is now coming home to roost, creating supply chain issues, where supply can’t ramp up fast enough to meet demand.

The reason is fairly straightforward. As factories and equipment get older, companies think about the looming upcoming replacement cycle. They don’t want to install or repair older equipment, only to replace it sooner rather than later.

Hence, many companies are revamping their entire production systems, replacing new equipment with old equipment, and increasing short-term capacity while they’re at it. It’s a “two birds with one stone” solution. While this is the needed fix, it takes time to implement.

Had equipment been more up to date, it would have been easier for companies to add capacity without these overhauls, potentially alleviating some of the supply chain problems. Now, the painful fix will continue, prompting a huge capex wave over the next few years.

Investors looking for the best names to be exposed to this emerging theme should consider subscribing to our Conviction Long Idea List, where we include multiple names riding this spending trend.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research