Trouble in private equity means trouble for all

Prior bad decisions are coming to roost for both private equity (“PE”) and big banks right now.

PE firms are eager to continue making deals. However, these firms are facing challenges securing their usual debt capital from large bank loans.

The issue stems from past transactions. Banks still hold debt from prior PE deals on their balance sheets.

Take last year’s Citrix Systems deal for example. Last year, this software company went private in a deal worth $16.5 billion. This was done with help from Elliott Management and Vista Equity Partners.

Banks involved in the process incurred some serious losses. Collectively, Bank of America (BAC), Credit Suisse, and Goldman Sachs (GS) faced losses exceeding $500 million from the debt supporting the Citrix transaction.

Other banks, like Barclays (BCS) and Morgan Stanley (MS), still owe money from when Elon Musk bought Twitter.

As a result, many banks are hesitant to lend further to the sector. Thus, PE firms are exploring alternative financing sources like private capital.

However, these alternatives often come with higher interest rates. Also finding such alternative financing, even at these rates, can be a challenge.

As we’ll talk about today, this is a classic example of what happens in a credit crunch. And this crunch is showing up in a metric we constantly monitor to see where the economy and market are heading.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

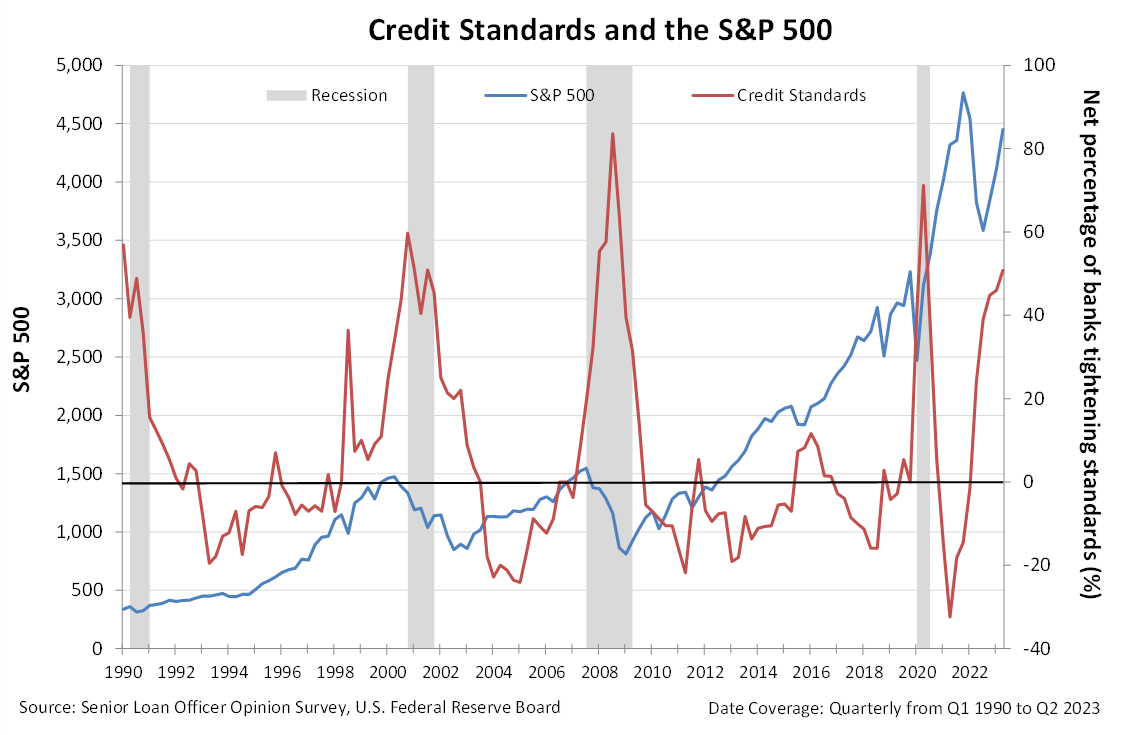

Determining the difficulty companies face in obtaining credit isn’t a challenge. Every quarter, the Fed provides insights into credit tightness via the Senior Loan Officer Opinion Survey or the SLOOS.

The SLOOS is a tool used by the Federal Reserve to gather information about lending practices in the U.S.

Essentially, it’s a quarterly survey sent to senior loan officers at various banks. It asks them about changes in their institutions’ lending standards and the overall demand for loans.

By collecting these insights, the Federal Reserve can gauge the health of the banking sector. This information allows them to make informed decisions related to monetary policy.

The SLOOS provides valuable data on the lending environment. It indicates whether banks are tightening or loosening their credit standards, which can reflect broader economic conditions.

In the most recent SLOOS report, 51% of banks indicated they’ve made their lending standards stricter. Such a level is nearing points historically associated with the onset of a recession.

During the first quarter of 2008, when the U.S. was on the brink of a recession, 32% of banks reported tightening standards. Within a year, that number surpassed 75%. Similarly, 51% of banks were tightening in the early months of 2001, right as the dot-com bubble was bursting.

When the SLOOS indicates a tightening of credit availability, it reflects the financial sector’s growing caution in lending money. This caution is typically triggered by perceived economic risks like high-interest rates and inflation.

And the hesitation of banks to lend to PE firms highlights the growing economic concerns leading to tighter credit conditions.

PE firms traditionally rely on leveraging, or borrowing large sums of money, to fund acquisitions.

Thus, when banks become hesitant to lend to PE firms, it’s a clear sign that they see higher risks in the broader economy.

This reluctance is driven by concerns that, in an economic downturn, PE-backed companies may struggle to generate the returns needed to repay their loans.

When such caution mirrors levels typically observed during recessions, it suggests that banks are bracing for economic headwinds.

In essence, banks tightening their purse strings for PE firms can be viewed as a canary in the coal mine for broader economic concerns.

Credit is the backbone of the market.

Credit availability drives the economy. So, if banks are unwilling to lend, that means we know what comes next. Companies that need to borrow are going to be starved for capital to the point of bankruptcy.

The SLOOS is right around levels where we consistently see recessions kick off, and some plenty of companies are already struggling with refinancing.

Recession risk is rising. That’s why it’s important not to have all your eggs in one basket. If you’re planning on putting any money to work, you’d be best off doing it slowly instead of all at once.

In our Timetable Investor newsletter, we recommend readers allocate their money over a window between three and 24 months. The slower, the worse the near-term outlook.

Today, we recommend a 24-month allocation window, the most bearish we can be.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research